Retirement isn’t about having a large savings balance—it’s about turning that savings into reliable, ongoing income.

Without a paycheck, your financial stability depends on how well you can convert your assets into a steady income stream that lasts for decades.

The goal is simple:

Create consistent income while protecting your savings from running out.

Let’s break down how to build a retirement income stream step by step.

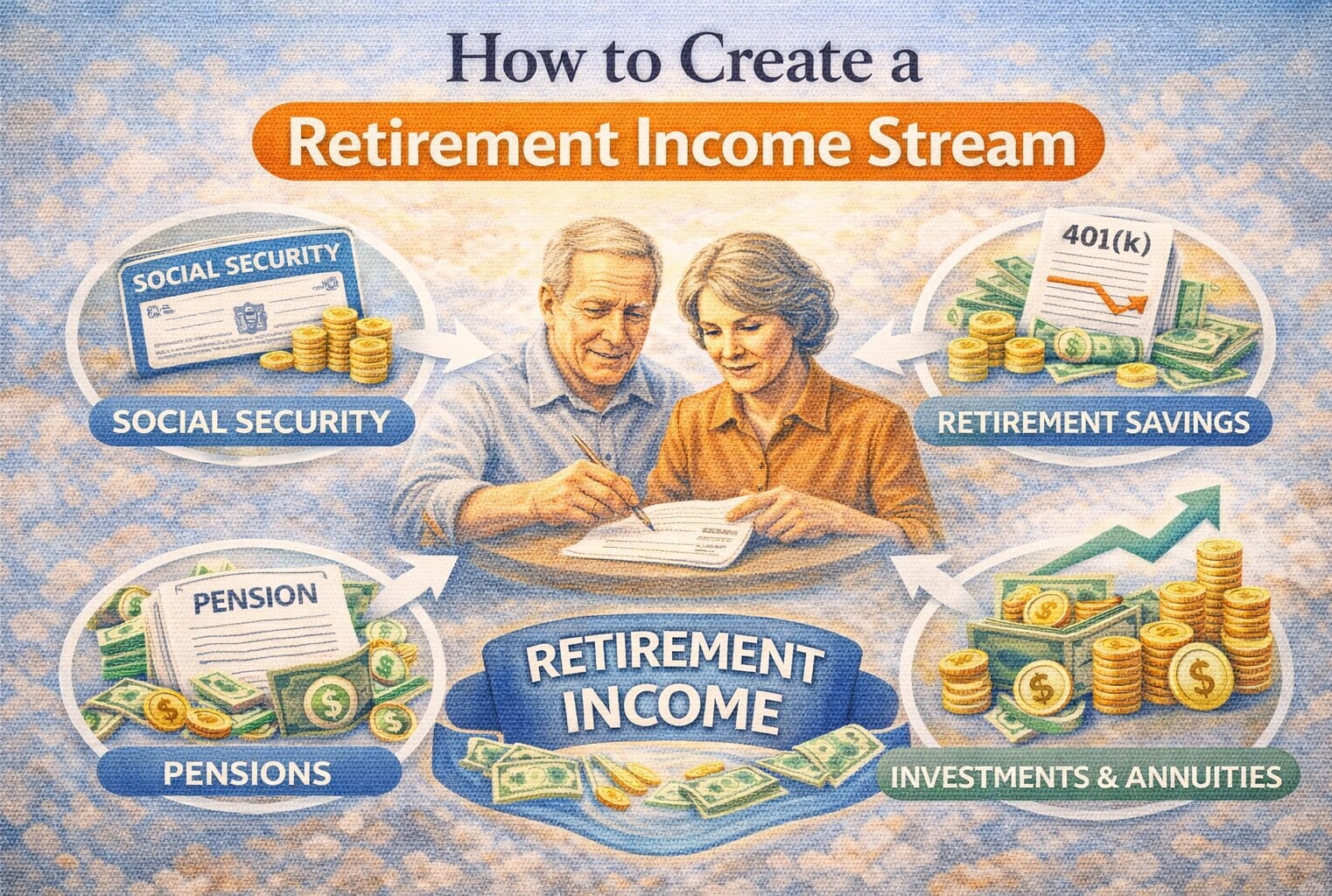

What Is a Retirement Income Stream?

A retirement income stream is the combination of all sources that provide you with regular income after you stop working.

These sources typically include:

- Social Security

- Retirement account withdrawals

- Investments

- Passive income

The key is combining them in a way that is stable, tax-efficient, and sustainable.

Step 1: Estimate Your Income Needs

Before creating income, you need to know how much you’ll need.

A common approach:

- Replace 70%–80% of your pre-retirement income

Example:

- Pre-retirement income: $80,000

- Retirement need: ~$60,000/year

For detailed budgeting:

https://statush.com/retirement-planning/retirement-budget-planning-guide

Step 2: Identify Your Income Sources

Most retirees rely on multiple income streams.

Here’s a simple breakdown:

| Income Source | Stability | Flexibility |

|---|---|---|

| Social Security | High | Low |

| Retirement Accounts | Medium | High |

| Passive Income | Medium | Medium |

| Investments | Variable | High |

Diversifying your income sources reduces risk.

Step 3: Use the Safe Withdrawal Rule

Your savings need to generate income sustainably.

A common guideline:

- Withdraw around 4% annually

Example:

- $1 million portfolio → $40,000/year

To understand this rule:

https://statush.com/retirement-planning/safe-withdrawal-rate-explained

Step 4: Build Passive Income Streams

Passive income reduces reliance on withdrawals.

Examples include:

- Dividend stocks

- Rental income

- Bonds

Example:

- Passive income: $20,000/year

- Remaining need: $40,000

To explore options:

https://statush.com/retirement-planning/how-to-create-passive-income-for-retirement

Step 5: Plan Your Withdrawal Strategy

How you withdraw money matters.

General approach:

- Taxable accounts

- Tax-deferred accounts (IRA, 401k)

- Roth accounts

This helps minimize taxes.

To learn more:

https://statush.com/retirement-planning/best-withdrawal-strategy-for-retirement-accounts

Step 6: Time Your Social Security Benefits

Social Security provides a stable income base.

- Claim early → lower income

- Delay → higher income

Example:

- $2,000/month at 67

- ~$2,480/month at 70

To plan timing:

https://statush.com/retirement-planning/when-should-you-start-social-security

Step 7: Balance Growth and Income

Your portfolio should support both:

| Goal | Investment Type |

|---|---|

| Income | Bonds, dividends |

| Growth | Stocks |

| Stability | Cash |

This ensures your income grows over time while remaining stable.

Real-World Example

Case Study:

- Total savings: $1 million

- Income goal: $60,000/year

Income plan:

- Social Security → $25,000

- Dividends → $15,000

- Withdrawals → $20,000

This balanced approach:

- Reduces withdrawal pressure

- Provides stable income

Step 8: Adjust for Inflation

Your income needs will increase over time.

Example:

- $60,000 today → ~$90,000+ in 20 years

To manage inflation:

https://statush.com/retirement-planning/how-inflation-impacts-retirement-planning

Step 9: Protect Against Market Risk

Market downturns can impact your income.

Strategies:

- Maintain a cash reserve

- Use a diversified portfolio

- Adjust withdrawals during downturns

To protect your savings:

https://statush.com/retirement-planning/how-to-protect-retirement-savings-from-market-crashes

Step 10: Optimize Taxes

Taxes can reduce your income significantly.

Strategies:

- Use tax-efficient withdrawal order

- Combine taxable and tax-free income

- Consider Roth conversions

To reduce taxes:

https://statush.com/retirement-planning/how-to-reduce-taxes-in-retirement

Common Mistakes to Avoid

- Relying on a single income source

- Withdrawing too much early

- Ignoring taxes

- Not adjusting for inflation

For more insights:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

How It Fits Into Your Retirement Plan

Your income stream connects everything:

- Savings

- Investments

- Budget

- Lifestyle

Without a structured income plan, even large savings can be mismanaged.

To align your savings goals:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age

Final Thoughts

Creating a retirement income stream is about turning your savings into a reliable paycheck for life.

The best strategies combine:

- Stability (Social Security, bonds)

- Growth (stocks)

- Flexibility (Roth accounts, withdrawals)

With the right plan, you can enjoy retirement with confidence—knowing your income is steady, sustainable, and built to last.