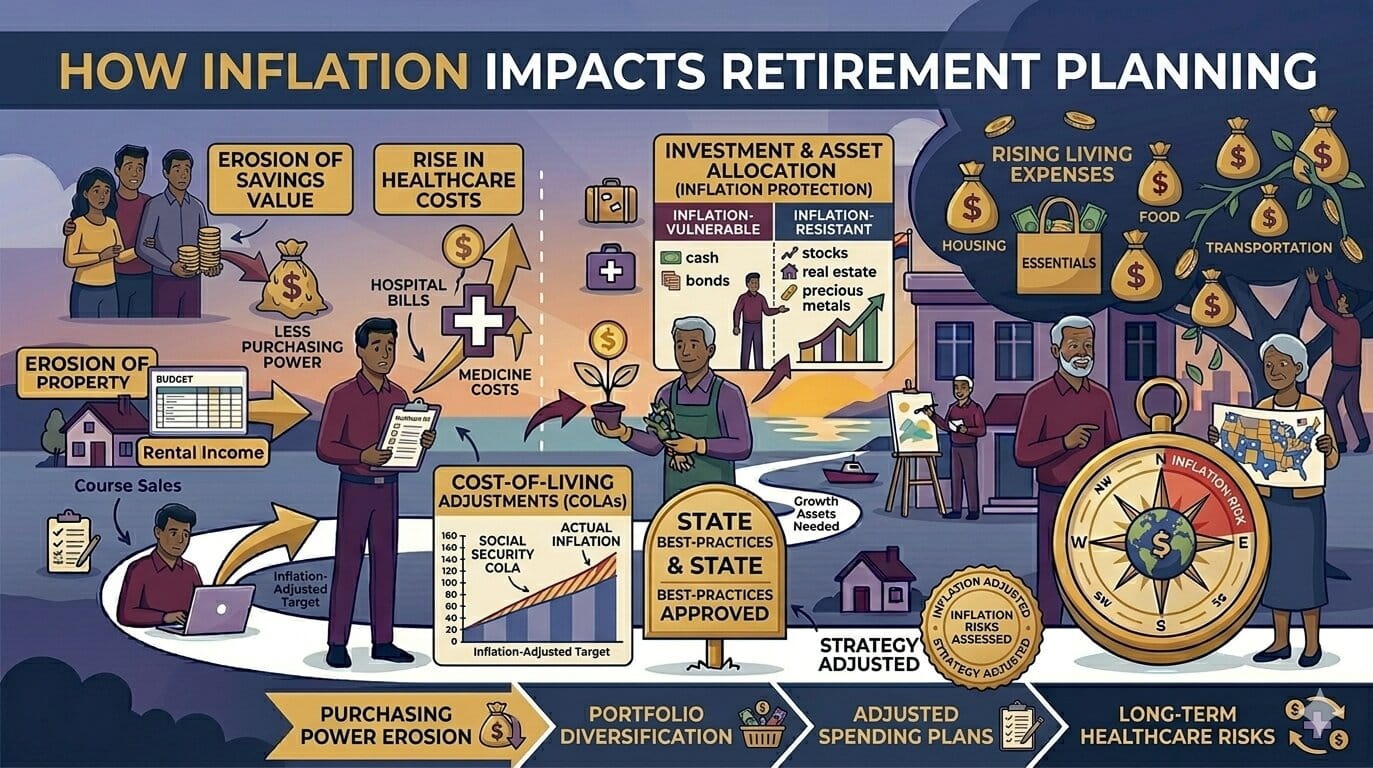

Inflation is one of the most underestimated risks in retirement planning. It doesn’t happen suddenly—but over time, it quietly reduces your purchasing power.

What costs $50,000 today might cost significantly more in the future. And if your income doesn’t keep up, your lifestyle can slowly decline.

That’s why understanding inflation—and planning for it—is essential for a secure retirement.

What Is Inflation?

Inflation is the gradual increase in prices over time.

As inflation rises:

- The value of money decreases

- Your expenses increase

- Your savings buy less

Simple example:

- Today: $100 buys groceries for a week

- In 20 years: That same basket might cost $180+

Why Inflation Matters in Retirement

Inflation is especially important in retirement because:

- You’re living on a fixed or semi-fixed income

- Your savings must last decades

- Costs (especially healthcare) tend to rise

Unlike your working years, you can’t easily increase your income to keep up.

How Inflation Affects Your Savings

Let’s look at a simple scenario:

| Year | Annual Expenses (3% Inflation) |

|---|---|

| Today | $50,000 |

| 10 Years | ~$67,000 |

| 20 Years | ~$90,000 |

| 30 Years | ~$121,000 |

This shows how significantly costs can increase over time.

Real-World Example

Case Study:

- Retiree needs $60,000/year today

- Inflation rate: 3%

After 25 years:

- Required income → ~$125,000/year

If their income doesn’t grow, they’ll struggle to maintain their lifestyle.

Inflation vs Fixed Income

One of the biggest risks is relying only on fixed income sources.

Examples:

- Pensions

- Bonds with fixed interest

- Fixed annuities

These may not keep up with inflation.

Example:

A $40,000 fixed income today may feel insufficient in 20 years.

How Inflation Impacts Different Retirement Assets

| Asset Type | Inflation Impact |

|---|---|

| Cash | Loses value over time |

| Bonds | Limited protection |

| Stocks | Potential growth above inflation |

| Real Estate | Often keeps pace with inflation |

This is why diversification is critical.

Common Mistakes to Avoid

- Keeping too much cash

- Ignoring inflation in long-term planning

- Relying only on fixed income

- Not adjusting spending over time

For more insights:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

How Inflation Affects Retirement Goals

Inflation increases the amount you need to save.

Example:

- Goal today: $1 million

- Future equivalent: $1.5–$2 million (depending on inflation)

This is why planning early is critical.

To align your savings goals:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age

Practical Tips

- Include growth investments in your portfolio

- Adjust your budget annually

- Plan for rising healthcare costs

- Build multiple income streams

- Avoid over-reliance on fixed income

Final Thoughts

Inflation may be slow, but its impact is powerful.

It quietly reduces your purchasing power and can significantly affect your retirement lifestyle if ignored.

The key is not to avoid inflation—but to plan for it.

With the right mix of growth, income, and flexibility, you can protect your savings and maintain your lifestyle for decades.

And when inflation is accounted for in your strategy, your retirement plan becomes far more resilient—and realistic.