Retirement planning in the U.S. can feel overwhelming, especially when you’re constantly hearing different numbers—$1 million, $2 million, or even more. The truth is, there’s no single “perfect” number. What matters more is whether you’re on track for your age and lifestyle goals.

This guide breaks down how much you should aim to save at each stage of life, using simple benchmarks, real-world examples, and practical tips you can actually apply.

Why Age-Based Benchmarks Matter

Instead of focusing on a huge final number, it’s much easier (and more realistic) to track your progress over time. Financial experts often recommend saving a multiple of your annual salary by certain ages.

These benchmarks act like checkpoints. If you’re slightly behind, you can adjust early. If you’re ahead, you gain flexibility—maybe even the option to retire early.

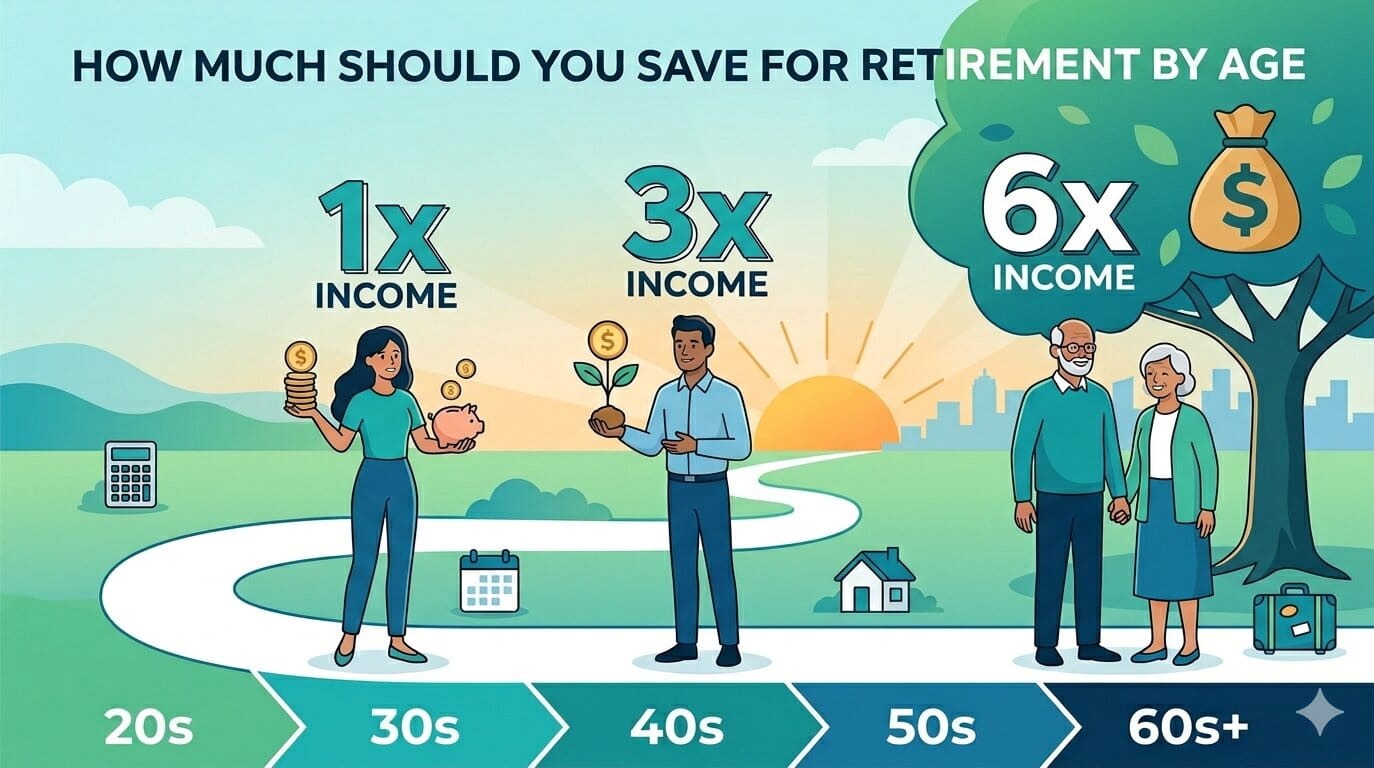

Retirement Savings Benchmarks by Age

Here’s a simple table to guide you:

| Age | Savings Goal (Multiple of Salary) | What It Means |

|---|---|---|

| 30 | 1x salary | You’ve started building momentum |

| 40 | 3x salary | Serious growth phase begins |

| 50 | 6x salary | Peak earning & saving years |

| 60 | 8–10x salary | Near retirement readiness |

| 67 | 10–12x salary | Comfortable retirement target |

These are general U.S.-based guidelines and assume you plan to retire around 65–67.

In Your 20s: Build the Habit, Not Perfection

Your 20s are less about hitting big numbers and more about building consistency.

If you’re earning $50,000, even saving $300–$500 per month can put you ahead of most people. The real advantage here is time. Thanks to compounding, money invested early grows significantly more than money invested later.

Example:

Alex starts investing $400/month at 25. By 65, assuming a 7% return, that grows to over $1 million. If Alex waits until 35, the total drops drastically—even if contributions increase.

Practical tips:

- Start with a 401(k), especially if your employer offers a match

- Open a Roth IRA (see how contributions work here: https://statush.com/retirement-planning/how-roth-ira-contributions-work )

- Automate savings so you don’t rely on discipline

At this stage, consistency beats perfection every time.

In Your 30s: Acceleration Phase

By your 30s, life gets more expensive—housing, family, responsibilities—but this is also when your income typically grows.

The goal: reach 1x your salary by 30 and 2–3x by 40.

Example:

Sarah earns $80,000 at 35. Ideally, she should have $80,000–$160,000 saved. If she’s behind, increasing contributions now can still make a big difference.

This is also the decade where missed opportunities start to matter more.

Practical tips:

- Increase your savings rate to 15–20% of income

- Invest in diversified portfolios (learn more: https://statush.com/retirement-planning/retirement-investment-portfolio-allocation )

- Avoid lifestyle inflation—raises shouldn’t fully go to spending

If you’re slightly behind, don’t panic. Adjusting in your 30s is still very effective.

In Your 40s: Serious Wealth Building

Your 40s are your prime earning years, and this is where retirement planning becomes real.

The target: 3x salary by 40, 5–6x by 50.

Example:

John earns $120,000 at 45 but only has $200,000 saved. Ideally, he should be closer to $360,000+. He’s behind—but not hopelessly.

At this stage, small changes won’t cut it. You need focused action.

Practical tips:

- Max out retirement accounts (401(k), IRA)

- Reduce high-interest debt aggressively

- Consider additional income streams (see: https://statush.com/retirement-planning/how-to-create-passive-income-for-retirement )

This decade often determines whether retirement will be comfortable or stressful.

In Your 50s: Catch-Up and Optimization

Your 50s are your final major opportunity to boost savings before retirement.

The goal: 6x salary by 50, 8–10x by 60.

The good news? U.S. retirement accounts allow catch-up contributions, meaning you can invest more than younger savers.

Example:

Lisa, age 55, earns $100,000 but has $350,000 saved. She’s behind the ideal $600,000 target. However, by maximizing contributions and delaying retirement slightly, she can still recover.

Practical tips:

- Take full advantage of catch-up contributions

- Shift investments gradually to reduce risk

- Learn withdrawal strategies early (https://statush.com/retirement-planning/best-withdrawal-strategy-for-retirement-accounts )

This stage is about efficiency, not just accumulation.

In Your 60s: Transition to Retirement

Now the focus shifts from saving to turning savings into income.

The target: 8–12x salary by retirement age (65–67).

But here’s something important—your total savings number matters less than how much income it can generate.

This is where concepts like the safe withdrawal rate come into play (learn more: https://statush.com/retirement-planning/safe-withdrawal-rate-explained ).

Example:

If you have $1 million saved, a 4% withdrawal rate gives you about $40,000/year—plus Social Security.

Practical tips:

- Plan when to take Social Security (https://statush.com/retirement-planning/when-should-you-start-social-security )

- Create a structured income plan

- Reduce exposure to market volatility

This stage is less about growth and more about stability.

What If You’re Behind?

Let’s be honest—many people are.

The key is not to compare yourself to ideal benchmarks but to improve your trajectory.

Here are realistic ways to catch up:

- Increase savings rate (even 5% more helps significantly)

- Delay retirement by a few years

- Reduce major expenses (housing, debt)

- Build additional income streams

You can also explore alternative strategies like the FIRE approach (https://statush.com/retirement-planning/what-is-the-fire-movement ), which focuses on aggressive saving and early retirement.

Factors That Change Your Target

Not everyone needs the same retirement savings. Your number depends on:

- Lifestyle expectations (modest vs luxury)

- Location (cost of living varies widely across the U.S.)

- Health and longevity

- Additional income sources (Social Security, pensions, rental income)

For example, someone planning to retire in a low-cost state may need far less than someone staying in a high-cost city.

A Simple Way to Estimate Your Goal

A quick rule of thumb:

- Multiply your desired annual retirement income by 25

So if you want $60,000/year in retirement:

- $60,000 × 25 = $1.5 million

This aligns with the 4% withdrawal rule and gives you a practical target.

Final Thoughts

Retirement savings isn’t about hitting a perfect number—it’s about staying on track over time.

If you’re in your 20s, focus on starting.

If you’re in your 30s or 40s, focus on scaling.

If you’re in your 50s or 60s, focus on optimizing.

The earlier you take it seriously, the easier it becomes. But even if you’re starting late, smart adjustments can still lead to a comfortable retirement.

And if you want a deeper dive into planning strategies, start here: https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age