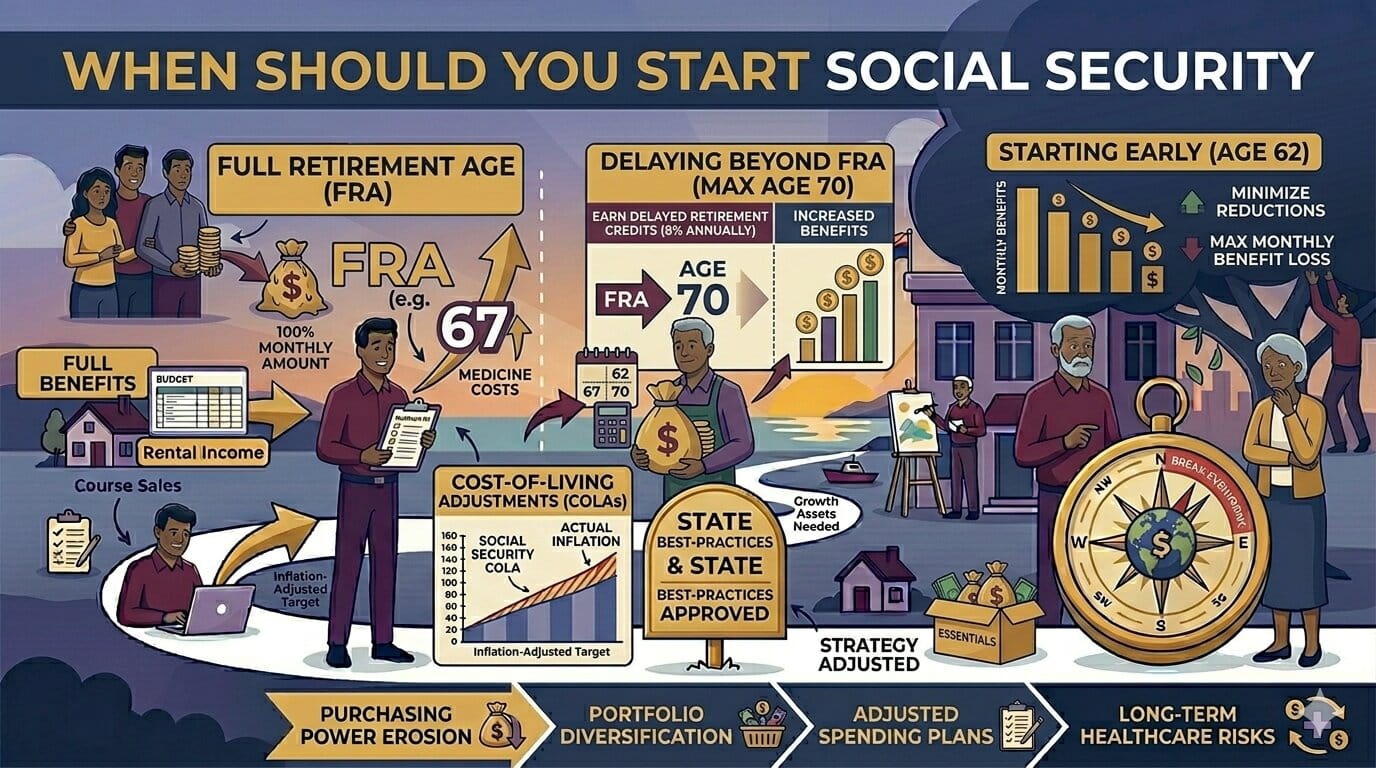

Deciding when to start Social Security is one of the most important—and often confusing—decisions in retirement planning.

You can claim benefits as early as 62, wait until full retirement age (around 67), or delay until 70. Each option has a significant impact on your monthly income and total lifetime benefits.

The right choice isn’t the same for everyone. It depends on your health, financial situation, and long-term goals.

Let’s break it down clearly so you can make an informed decision.

Why Timing Matters

The age you claim Social Security directly affects how much you receive each month.

- Claim early → smaller monthly payments

- Claim later → larger monthly payments

But there’s a trade-off:

Do you want money sooner, or more money later?

Social Security Claiming Ages Explained

Here’s a simple breakdown:

| Age | What Happens |

|---|---|

| 62 | Earliest eligibility, reduced benefits |

| 67 | Full retirement age (FRA), full benefits |

| 70 | Maximum benefits (delayed credits) |

How Much Difference Does It Make?

Let’s look at a practical example:

| Claiming Age | Monthly Benefit |

|---|---|

| 62 | $1,400 |

| 67 | $2,000 |

| 70 | $2,480 |

That’s a huge difference over time.

- Claim early → less per month, longer payout

- Delay → more per month, shorter payout

Option 1: Claiming at Age 62

This is the earliest you can start receiving benefits.

Pros:

- Immediate income

- Useful if you need money early

- More total payments (over time)

Cons:

- Permanent reduction (~25–30%)

- Lower lifetime income if you live longer

Best for:

- Those with shorter life expectancy

- People who need income immediately

Option 2: Claiming at Full Retirement Age (67)

This is considered the standard option.

Pros:

- Full benefit amount

- Balanced approach

- No early reduction

Cons:

- You wait longer to receive income

Best for:

- People with average life expectancy

- Those who want a middle-ground strategy

Option 3: Delaying Until Age 70

Delaying increases your benefit significantly.

- Benefits grow ~8% per year after FRA

Pros:

- Highest monthly income

- Better protection against inflation

- Strong long-term strategy

Cons:

- Delayed income

- Requires other income sources in early retirement

Best for:

- People in good health

- Those expecting longer lifespans

Break-Even Point: When Delaying Pays Off

There’s a point where delaying benefits becomes more profitable.

Example:

- Claim early → more payments initially

- Claim later → higher payments over time

Typically, the break-even age is around:

- 78–82 years old

If you live beyond that, delaying often results in more total income.

Real-World Example

Case Study:

- Maria, age 62

- Benefit at 62: $1,500/month

- Benefit at 70: $2,600/month

If she lives into her 80s:

- Delaying could result in significantly higher total income

Factors That Affect Your Decision

1. Health and Life Expectancy

- Shorter lifespan → claim earlier

- Longer lifespan → delay benefits

2. Financial Situation

- Need income now → claim early

- Have other income → delay

3. Work Status

If you’re still working:

- Benefits may be reduced if claimed early

4. Spousal Benefits

Married couples can optimize benefits by coordinating claiming strategies.

Social Security and Taxes

Your benefits may be taxable depending on your income.

Example:

- Higher income → up to 85% of benefits taxable

Planning withdrawals carefully can reduce taxes.

To learn more:

https://statush.com/retirement-planning/how-to-reduce-taxes-in-retirement

How Social Security Fits Into Your Retirement Plan

Social Security should be part of a larger income strategy.

Example:

- Expenses: $60,000/year

- Social Security: $25,000

- Remaining need: $35,000

This reduces reliance on your savings.

To build a full plan:

https://statush.com/retirement-planning/retirement-income-planning-strategies

Common Mistakes to Avoid

- Claiming too early without a plan

- Ignoring long-term impact

- Not considering spouse benefits

- Overlooking tax implications

For more insights:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

Practical Strategies

- Delay if you can afford to

- Use other income sources early

- Consider your health and family history

- Coordinate with your spouse

- Plan for taxes

How It Connects to Your Savings Goals

The timing of Social Security affects how much you need to save.

- Early claim → need more savings

- Delayed claim → less pressure on savings

To align your savings strategy:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age

Final Thoughts

There’s no universal “best age” to start Social Security.

The right choice depends on your personal situation—your health, finances, and long-term goals.

But one thing is clear:

- Claiming early gives you income sooner

- Delaying gives you more income later

The key is finding the balance that works for your life.

With the right strategy, Social Security can become a powerful foundation for a secure and comfortable retirement.