Saving for retirement is only half the job. The real challenge begins when you need to turn your savings into income—without running out of money or paying unnecessary taxes.

That’s where a smart withdrawal strategy comes in.

The order, timing, and amount you withdraw can significantly impact:

- How long your money lasts

- How much tax you pay

- Your overall financial stability

Let’s break down the best withdrawal strategies in a clear, practical way.

Why Withdrawal Strategy Matters

Without a plan, you could:

- Pay higher taxes than necessary

- Deplete your savings too quickly

- Miss opportunities to optimize income

A good strategy helps you:

Maximize income while minimizing taxes and risk

Types of Retirement Accounts (Quick Overview)

Before choosing a strategy, understand how different accounts are taxed:

| Account Type | Tax Treatment |

|---|---|

| Traditional IRA / 401(k) | Taxed as income |

| Roth IRA | Tax-free withdrawals |

| Taxable Accounts | Capital gains tax |

Each account plays a different role in your withdrawal plan.

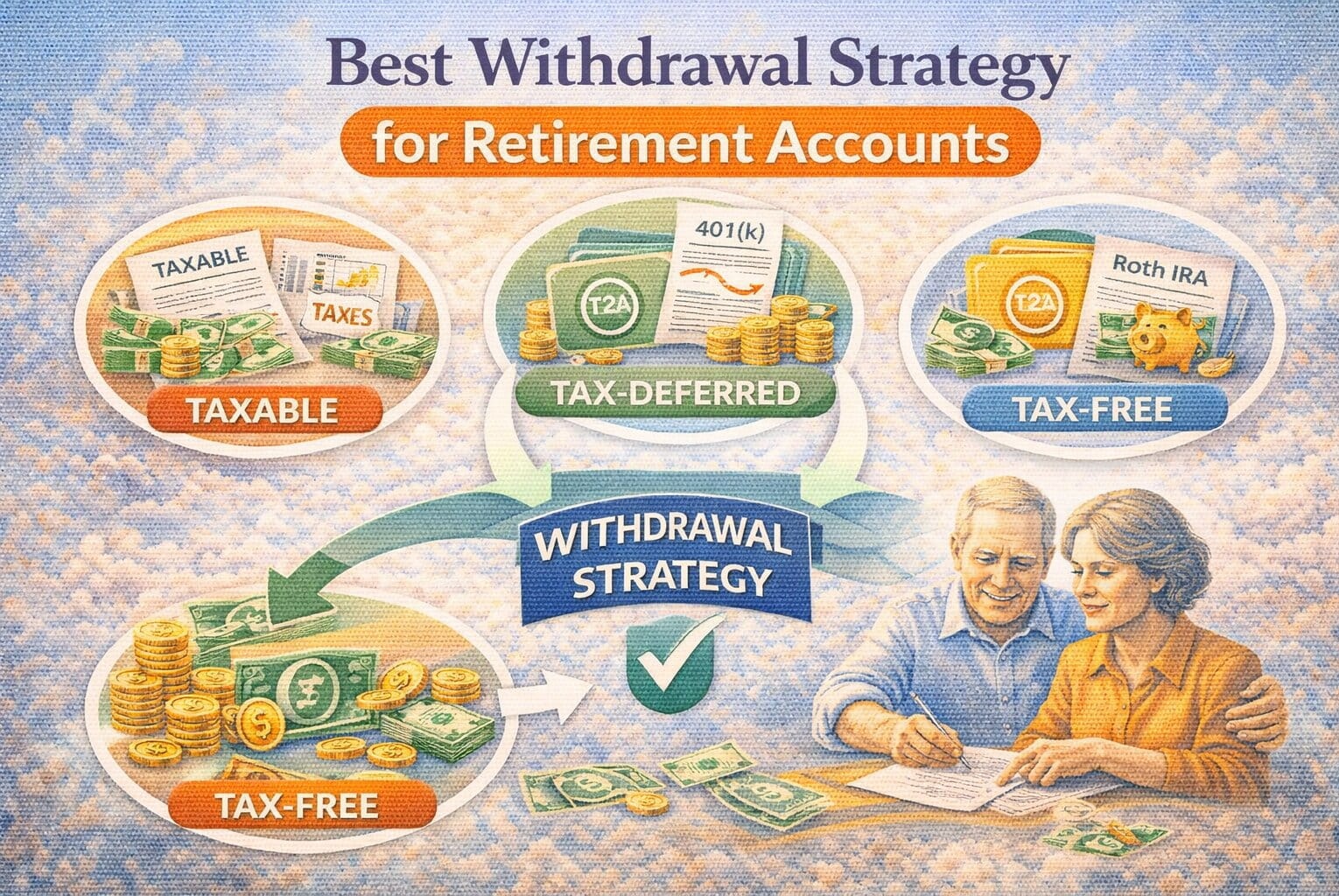

The Standard Withdrawal Order

A commonly recommended strategy is:

1. Taxable Accounts First

2. Tax-Deferred Accounts (IRA, 401k)

3. Roth Accounts Last

Why this works:

- Taxable accounts → lower tax rates (capital gains)

- Tax-deferred → taxed as income

- Roth → grows tax-free, best used later

Example of Withdrawal Order

Case Study:

- Total retirement income needed: $60,000

Strategy:

- $20,000 from taxable investments

- $25,000 from Traditional IRA

- $15,000 from Roth IRA

Result:

- Balanced tax impact

- Lower overall tax burden

Strategy 1: Follow the 4% Rule

The 4% rule provides a baseline for how much to withdraw.

- Withdraw 4% annually

- Adjust for inflation

Example:

- $1 million portfolio → $40,000/year

To understand this rule:

https://statush.com/retirement-planning/safe-withdrawal-rate-explained

Strategy 2: Use a Flexible Withdrawal Approach

Instead of fixed withdrawals, adjust based on market conditions.

Example:

- Strong market → withdraw slightly more

- Weak market → withdraw less

This helps preserve your portfolio during downturns.

Strategy 3: Tax Bracket Management

Your goal is to stay within a lower tax bracket.

Example:

- Withdraw just enough from IRA to stay in the 12% or 22% bracket

- Use Roth funds to avoid pushing into higher brackets

To reduce taxes:

https://statush.com/retirement-planning/how-to-reduce-taxes-in-retirement

Strategy 4: Plan Around Required Minimum Distributions (RMDs)

Traditional retirement accounts require withdrawals starting in your 70s.

These can:

- Increase taxable income

- Push you into higher tax brackets

Solution:

- Withdraw gradually before RMD age

- Consider Roth conversions

To understand RMDs:

https://statush.com/retirement-planning/traditional-ira-withdrawal-rules-explained

Strategy 5: Coordinate with Social Security

The timing of Social Security affects your withdrawal strategy.

Example:

- Delay Social Security

- Use savings early

This can:

- Increase future benefits

- Reduce early taxable income

To plan timing:

https://statush.com/retirement-planning/when-should-you-start-social-security

Strategy 6: Combine Income Sources

A strong withdrawal plan includes multiple income streams:

- Social Security

- Investment withdrawals

- Passive income

Example:

- Social Security → $25,000

- Withdrawals → $30,000

- Dividends → $10,000

Total: $65,000

To explore income strategies:

https://statush.com/retirement-planning/retirement-income-planning-strategies

Strategy 7: Use Roth Accounts Strategically

Roth accounts provide tax-free income.

Best use:

- During high-tax years

- To avoid moving into higher tax brackets

To understand Roth strategies:

https://statush.com/retirement-planning/roth-conversion-strategy-explained

Real-World Example

Case Study:

- Portfolio: $1.2 million

- Income need: $70,000

Strategy:

- $25,000 Social Security

- $30,000 IRA withdrawals

- $15,000 Roth withdrawals

Result:

- Balanced taxes

- Stable income

Common Mistakes to Avoid

- Withdrawing too much early

- Ignoring tax implications

- Not diversifying income sources

- Taking large lump sums unnecessarily

For more pitfalls:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

How It Fits Into Your Retirement Plan

Your withdrawal strategy connects:

- Savings

- Investments

- Taxes

- Income

Without a plan, even large savings can be inefficiently used.

To align with your savings goals:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age

Practical Tips

- Plan withdrawals annually

- Use a mix of account types

- Adjust based on market performance

- Keep flexibility in your strategy

- Review regularly

Final Thoughts

The best withdrawal strategy isn’t just about how much you take—it’s about when, where, and how you take it.

A well-planned approach helps:

- Reduce taxes

- Extend your savings

- Maintain a stable income

Retirement isn’t just about having money—it’s about using it wisely.

And with the right withdrawal strategy, you can turn your savings into a reliable income that lasts for decades.