One of the biggest questions in retirement planning is simple—but critical:

How much can you safely withdraw from your savings each year without running out of money?

This is where the safe withdrawal rate comes in. It’s the foundation of retirement income planning and a key concept behind strategies like FIRE and early retirement.

Let’s break it down in a clear, practical way so you can actually use it.

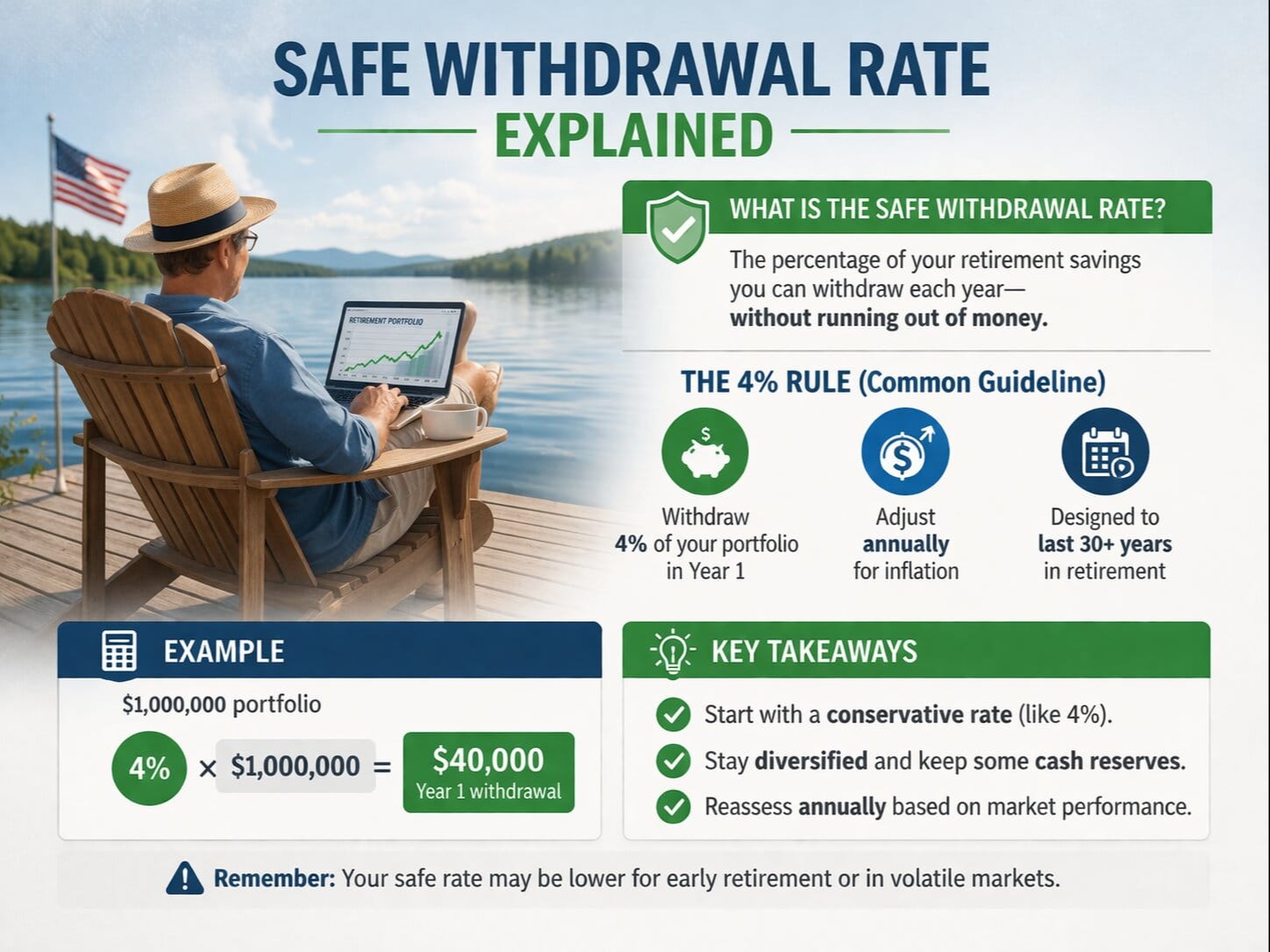

What Is the Safe Withdrawal Rate?

The safe withdrawal rate is the percentage of your retirement savings you can withdraw annually while still making your money last for decades.

The most commonly used rule is:

- 4% per year

This is often called the 4% rule.

How the 4% Rule Works

The idea is simple:

- Withdraw 4% of your portfolio in the first year of retirement

- Adjust that amount for inflation each year

Example:

- Retirement savings: $1,000,000

- First-year withdrawal: $40,000 (4%)

In future years, you increase that amount slightly to keep up with inflation.

Simple Table for Understanding

| Portfolio Size | 4% Withdrawal | Monthly Income |

|---|---|---|

| $500,000 | $20,000/year | ~$1,667 |

| $1,000,000 | $40,000/year | ~$3,333 |

| $1,500,000 | $60,000/year | ~$5,000 |

| $2,000,000 | $80,000/year | ~$6,667 |

This gives you a quick way to estimate how much income your savings can generate.

Where Did the 4% Rule Come From?

The rule is based on historical market research (like the Trinity Study), which analyzed how long portfolios lasted under different withdrawal rates.

It found that withdrawing around 4% annually gave a high probability that your money would last 30 years or more.

Real-World Example

Let’s make this practical.

Case Study:

- Robert retires at 65

- Has $800,000 saved

- Uses a 4% withdrawal rate

First-year income:

- $32,000

Combined with Social Security, this may be enough to cover his expenses.

To understand Social Security timing:

https://statush.com/retirement-planning/when-should-you-start-social-security

Why the Safe Withdrawal Rate Matters

Without a strategy, it’s easy to:

- Withdraw too much and run out of money

- Withdraw too little and limit your lifestyle unnecessarily

The safe withdrawal rate provides a balanced approach.

Factors That Affect Your Withdrawal Rate

The 4% rule is a guideline—not a guarantee.

Several factors can influence your ideal rate:

1. Retirement Length

- Retiring at 65 → 30-year timeline

- Retiring at 45 → 40–50 years

Early retirees often need a lower withdrawal rate (3–3.5%).

2. Market Performance

If markets perform poorly early in retirement, your portfolio can be impacted significantly.

This is called sequence of returns risk.

3. Inflation

Inflation reduces purchasing power over time.

To understand its impact:

https://statush.com/retirement-planning/how-inflation-impacts-retirement-planning

4. Investment Allocation

Your mix of stocks and bonds affects both growth and stability.

For guidance:

https://statush.com/retirement-planning/retirement-investment-portfolio-allocation

3%, 4%, or 5%: Which Should You Use?

Here’s a general guideline:

| Withdrawal Rate | Risk Level | Best For |

|---|---|---|

| 3% | Very Safe | Early retirement, long timelines |

| 4% | Balanced | Traditional retirement |

| 5% | Higher Risk | Shorter retirement or flexible spending |

Example:

- Early retiree at 45 → safer with 3–3.5%

- Retiree at 65 → 4% is often reasonable

Safe Withdrawal Rate and FIRE

The safe withdrawal rate is central to FIRE strategies.

Example:

- Annual expenses: $50,000

- Required savings: $50,000 × 25 = $1.25 million

This calculation directly uses the 4% rule.

To learn more:

https://statush.com/retirement-planning/what-is-the-fire-movement

Common Mistakes to Avoid

Even with a solid rule, mistakes can happen:

- Ignoring inflation

- Withdrawing too aggressively early

- Not adjusting for market conditions

- Keeping too much money in low-growth assets

For more insights:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

Flexible Withdrawal Strategy

Many experts now recommend a more flexible approach instead of strictly sticking to 4%.

Example:

- Withdraw less during market downturns

- Withdraw more during strong market years

This helps your portfolio last longer.

How It Fits Into Your Retirement Plan

The safe withdrawal rate is just one part of a bigger plan.

You also need:

- Tax-efficient withdrawals

- Social Security planning

- Multiple income sources

To build a complete strategy:

https://statush.com/retirement-planning/retirement-income-planning-strategies

What If You Want More Income?

If your withdrawal amount feels too low, you have options:

- Increase your savings before retirement

- Reduce expenses

- Build passive income streams

Explore ideas here:

https://statush.com/retirement-planning/how-to-create-passive-income-for-retirement

Practical Tips

- Start with a 4% baseline

- Adjust based on your retirement age

- Review annually

- Keep a diversified portfolio

- Plan for flexibility

Consistency and adaptability are key.

Final Thoughts

The safe withdrawal rate isn’t about perfection—it’s about sustainability.

It gives you a simple, reliable framework to turn your savings into income without running out of money.

For most people, the 4% rule is a solid starting point. But the best approach is one that adapts to your situation, timeline, and goals.

And if you want to connect this strategy with your overall savings targets, start here:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age