A Roth IRA is one of the most powerful retirement tools available in the U.S.—but only if you truly understand how contributions work.

At a glance, it seems simple: you contribute money, it grows, and you withdraw it tax-free. But the real advantage lies in the details—contribution limits, rules, timing, and strategies.

Let’s break it all down in a way that’s easy to follow and actually useful.

What Is a Roth IRA?

A Roth IRA (Individual Retirement Account) allows you to invest after-tax income, meaning you don’t get a tax break today—but your money grows tax-free, and withdrawals in retirement are also tax-free.

This makes it very different from traditional retirement accounts.

If you want a broader comparison of retirement accounts, check:

https://statush.com/retirement-planning/best-retirement-accounts-usa

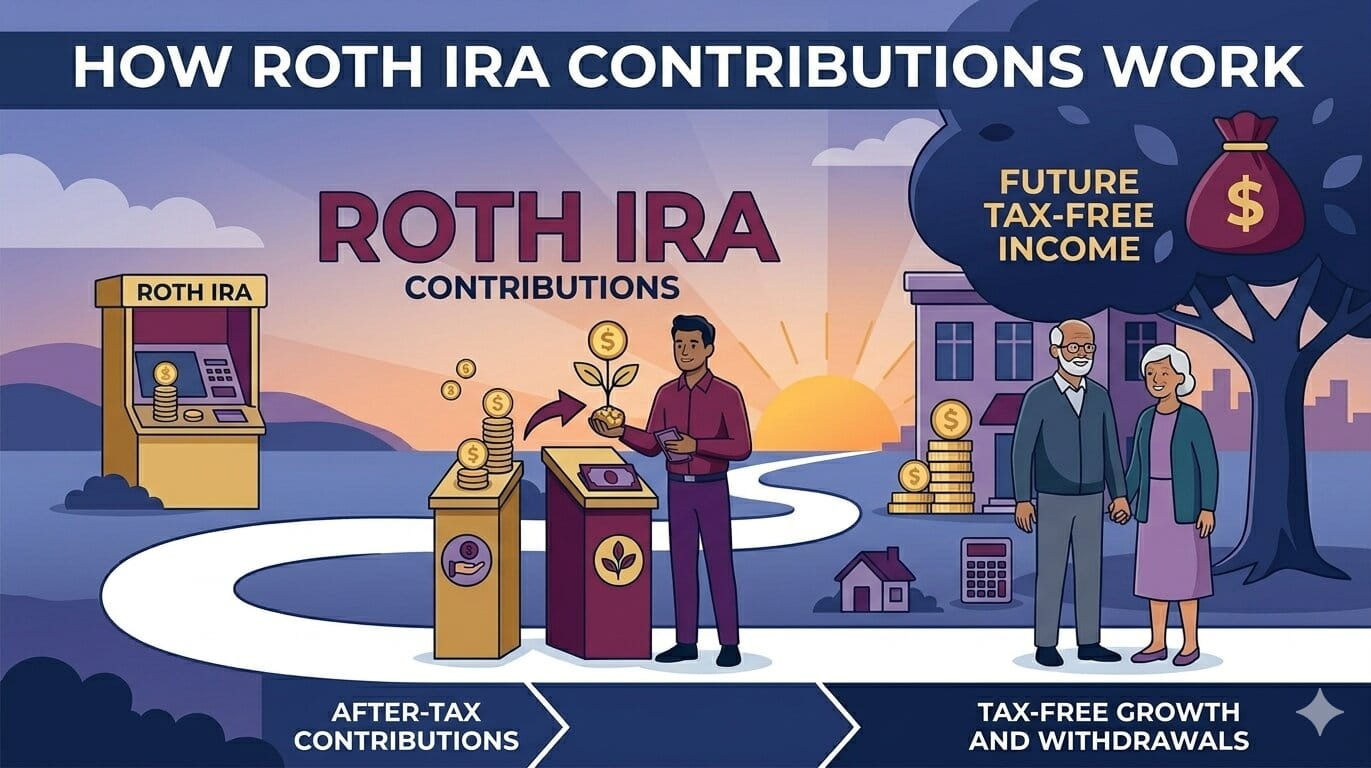

How Roth IRA Contributions Work (Simple Explanation)

Here’s the core idea:

- You contribute money you've already paid taxes on

- Your investments grow tax-free

- You can withdraw contributions anytime (without penalty)

- Earnings become tax-free after age 59½ (with conditions)

Let’s simplify this further with a table:

| Feature | Roth IRA Rule |

|---|---|

| Contribution Type | After-tax income |

| Annual Limit | Set by IRS (varies yearly) |

| Tax on Growth | None |

| Withdrawal of Contributions | Anytime, tax-free |

| Withdrawal of Earnings | Tax-free after 59½ |

| Required Minimum Distributions | None |

This combination is what makes Roth IRAs so attractive.

Contribution Limits (And What They Mean)

Each year, the IRS sets a maximum amount you can contribute.

For most people:

- Around $6,500–$7,000 annually (plus extra if age 50+)

But here’s the important part—your income affects eligibility.

If you earn above certain thresholds, your contribution limit may be reduced or eliminated.

Example:

Jessica earns $85,000 and contributes the full amount annually. But if her income rises significantly, she may need to adjust or use a backdoor strategy.

Real-World Example of Roth IRA Growth

Let’s make this practical.

Case Study:

- Age: 25

- Monthly contribution: $500

- Annual return: 7%

By age 65, this grows to over $1 million.

Now here’s the key advantage:

All of that can be withdrawn tax-free.

Compare that to a traditional account, where taxes could reduce your usable income significantly.

Contribution Timing Matters More Than You Think

When you contribute is almost as important as how much you contribute.

Two people investing the same total amount can end up with very different results depending on timing.

Example:

- Person A invests $6,500/year starting at 25

- Person B invests $6,500/year starting at 35

Even though both invest for decades, Person A ends up with significantly more due to compounding.

This is why starting early is one of the biggest advantages you can have.

Can You Withdraw Contributions Anytime?

Yes—and this is one of the most flexible features of a Roth IRA.

You can withdraw your original contributions at any time:

- No tax

- No penalty

However, earnings follow stricter rules.

Example:

If you contributed $30,000 over time and your account is now worth $50,000:

- You can withdraw $30,000 anytime

- The extra $20,000 (earnings) has restrictions

This flexibility makes Roth IRAs useful even beyond retirement.

Roth IRA vs Traditional IRA

Let’s compare quickly:

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax Benefit Now | No | Yes |

| Tax-Free Withdrawals | Yes | No |

| Required Withdrawals | No | Yes |

| Best For | Long-term growth | Immediate tax savings |

If you want to understand Traditional IRA rules in depth:

https://statush.com/retirement-planning/traditional-ira-withdrawal-rules-explained

Who Should Use a Roth IRA?

A Roth IRA is especially useful if:

- You’re early in your career

- You expect higher income in the future

- You want tax-free retirement income

- You value flexibility in withdrawals

Example:

A 28-year-old software engineer earning $70,000 benefits more from a Roth IRA than someone nearing retirement with a high income.

How Roth IRA Fits Into Your Retirement Plan

The best strategy isn’t choosing between Roth and traditional—it’s using both.

A balanced approach gives you:

- Tax savings now (traditional accounts)

- Tax-free income later (Roth accounts)

This concept is called tax diversification, and it’s critical for long-term planning.

To see how this fits into your overall savings targets:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age

Common Mistakes to Avoid

Even though Roth IRAs are simple, people still make avoidable mistakes:

- Not contributing early enough

- Leaving money uninvested (sitting as cash)

- Exceeding income limits without realizing

- Withdrawing earnings too early

For a broader list of pitfalls:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

Advanced Strategy: Backdoor Roth IRA

If your income is too high for direct contributions, you can still access a Roth IRA using a backdoor strategy.

This involves:

- Contributing to a Traditional IRA

- Converting it to a Roth IRA

It’s a common approach for high earners, but it requires careful execution to avoid tax complications.

Practical Tips for Maximizing Your Roth IRA

Here are some actionable tips:

- Automate monthly contributions

- Invest in low-cost index funds

- Increase contributions yearly

- Start as early as possible

- Avoid unnecessary withdrawals

Consistency matters more than timing the market.

Final Thoughts

A Roth IRA is simple in concept but powerful in impact.

You pay taxes today—but gain complete freedom later. No required withdrawals, no tax on growth, and flexibility when you need it.

For many Americans, it’s one of the best long-term wealth-building tools available.

If you use it early, consistently, and strategically, it can completely transform your retirement outlook.

And if you want to go deeper into building a full retirement income strategy, start here:

https://statush.com/retirement-planning/retirement-income-planning-strategies