A Traditional IRA is one of the most popular retirement accounts in the U.S.—mainly because it offers tax benefits upfront. But when it comes time to withdraw your money, the rules can get a bit tricky.

Understanding how withdrawals work isn’t just important—it can save you thousands of dollars in taxes and penalties.

Let’s break it down step by step, in plain English, with real-world examples and practical strategies.

What Is a Traditional IRA?

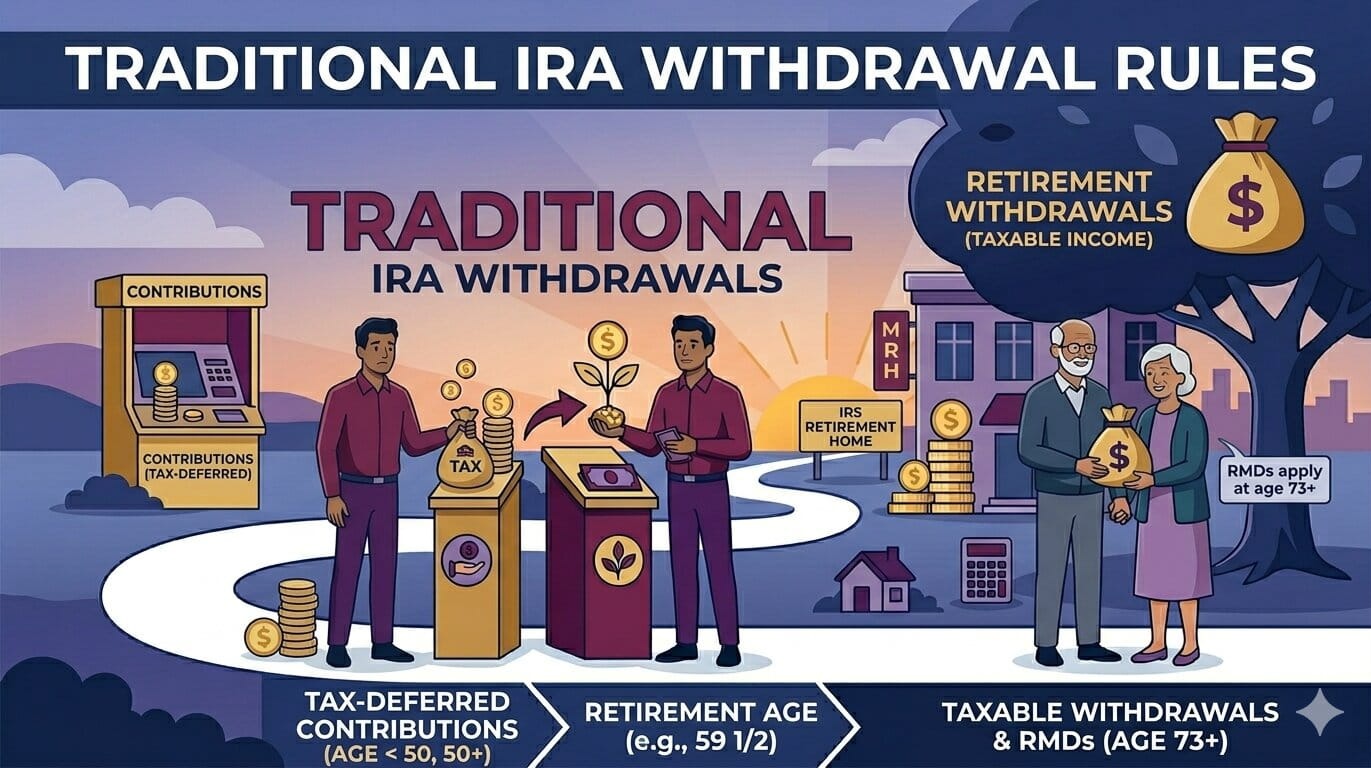

A Traditional IRA (Individual Retirement Account) allows you to contribute pre-tax income, meaning you may get a tax deduction today. Your investments then grow tax-deferred until retirement.

But here’s the trade-off:

When you withdraw the money later, it’s taxed as ordinary income.

If you want to compare this with other retirement accounts, start here:

https://statush.com/retirement-planning/best-retirement-accounts-usa

How Traditional IRA Withdrawals Work (Simple Overview)

At a basic level:

- Contributions may be tax-deductible

- Growth is tax-deferred

- Withdrawals are taxed as income

- Early withdrawals can trigger penalties

Here’s a quick table to simplify things:

| Rule Type | What It Means |

|---|---|

| Tax on Contributions | Usually deductible |

| Tax on Withdrawals | Fully taxable |

| Early Withdrawal Penalty | 10% before age 59½ |

| Required Minimum Distributions (RMDs) | Mandatory after certain age |

| Withdrawal Flexibility | Limited before retirement |

The Age 59½ Rule: The Most Important Threshold

The IRS sets age 59½ as the key milestone.

- Before 59½ → withdrawals may face a 10% penalty + income tax

- After 59½ → no penalty, but still taxed as income

Example:

Mike withdraws $20,000 at age 50.

- Pays income tax

- Pays additional 10% penalty ($2,000)

That’s a costly mistake if it’s avoidable.

Early Withdrawals: When Are They Allowed?

While early withdrawals are generally discouraged, there are some exceptions where you can avoid the 10% penalty (but still pay taxes):

- First-time home purchase (up to $10,000)

- Qualified education expenses

- Certain medical expenses

- Disability

Example:

Sarah withdraws $10,000 at age 35 to buy her first home. She avoids the penalty—but still pays income tax.

Even with exceptions, early withdrawals should be a last resort.

Required Minimum Distributions (RMDs)

Unlike Roth IRAs, Traditional IRAs require you to start withdrawing money at a certain age.

This is called a Required Minimum Distribution (RMD).

- Typically begins around age 73 (based on current IRS rules)

- You must withdraw a minimum amount each year

- Failure to do so can result in heavy penalties

Example:

John turns 73 and has $500,000 in his IRA. The IRS requires him to withdraw a specific percentage annually—even if he doesn’t need the money.

This ensures the government eventually collects taxes.

How Withdrawals Are Taxed

Every dollar you withdraw from a Traditional IRA is taxed as ordinary income.

That means your tax rate depends on:

- Your total income that year

- Your tax bracket

Example:

If you withdraw $50,000 in a year where your total income puts you in the 22% tax bracket:

- You could owe around $11,000 in federal taxes

This is why planning withdrawals strategically matters.

Real-World Withdrawal Strategy Example

Let’s look at a realistic scenario:

Case Study:

- Linda, age 65

- $800,000 in Traditional IRA

- Needs $40,000/year

Instead of withdrawing randomly, she:

- Combines IRA withdrawals with Social Security

- Keeps herself in a lower tax bracket

- Avoids large lump-sum withdrawals

This strategy helps her reduce lifetime taxes.

To go deeper into income planning:

https://statush.com/retirement-planning/retirement-income-planning-strategies

Traditional IRA vs Roth IRA (Withdrawal Perspective)

Here’s where things get interesting:

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Taxes on Withdrawal | Yes | No |

| Early Withdrawal Flexibility | Limited | More flexible |

| Required Distributions | Yes | No |

| Best Use Case | Tax savings now | Tax-free income later |

If you want to understand Roth IRA contributions and benefits:

https://statush.com/retirement-planning/how-roth-ira-contributions-work

Why Withdrawal Timing Is Critical

One of the biggest mistakes people make is withdrawing too much too quickly.

Large withdrawals can:

- Push you into a higher tax bracket

- Increase Medicare premiums

- Reduce long-term savings

Example:

Taking out $100,000 in one year instead of spreading it over several years could significantly increase your tax bill.

Strategies to Reduce Taxes on Withdrawals

Smart planning can make a huge difference.

Here are a few effective strategies:

- Spread withdrawals over multiple years

- Withdraw during lower-income years

- Combine with Roth accounts for flexibility

- Consider Roth conversions (learn more: https://statush.com/retirement-planning/roth-conversion-strategy-explained )

The goal is to control how much tax you pay—not just when you withdraw.

What Happens If You Miss an RMD?

Missing a Required Minimum Distribution is one of the most expensive mistakes.

The IRS penalty can be significant (historically up to 50%, though rules may evolve).

Example:

If your RMD is $20,000 and you don’t withdraw it, you could face a large penalty on that amount.

This is why tracking RMDs is essential once you reach the required age.

Common Mistakes to Avoid

Here are some of the most common errors:

- Withdrawing too early without a clear plan

- Ignoring tax implications

- Missing RMD deadlines

- Taking large lump sums unnecessarily

For more pitfalls, read:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

How Traditional IRA Fits Into Your Retirement Plan

A Traditional IRA works best when combined with other accounts.

For example:

- Use Traditional IRA for tax savings now

- Use Roth IRA for tax-free withdrawals later

This balance gives you flexibility in retirement.

To understand how much you should be saving overall:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age

Final Thoughts

Traditional IRA withdrawal rules aren’t complicated—but they do require attention.

The key points to remember:

- Withdrawals are taxable

- Early withdrawals can be costly

- RMDs are mandatory

- Timing affects how much tax you pay

If you plan ahead, you can minimize taxes, avoid penalties, and make your savings last longer.

And ultimately, that’s what retirement planning is all about—turning decades of savings into reliable, efficient income.