A Roth conversion is one of the most powerful—and often misunderstood—strategies in retirement planning.

At its core, it’s simple:

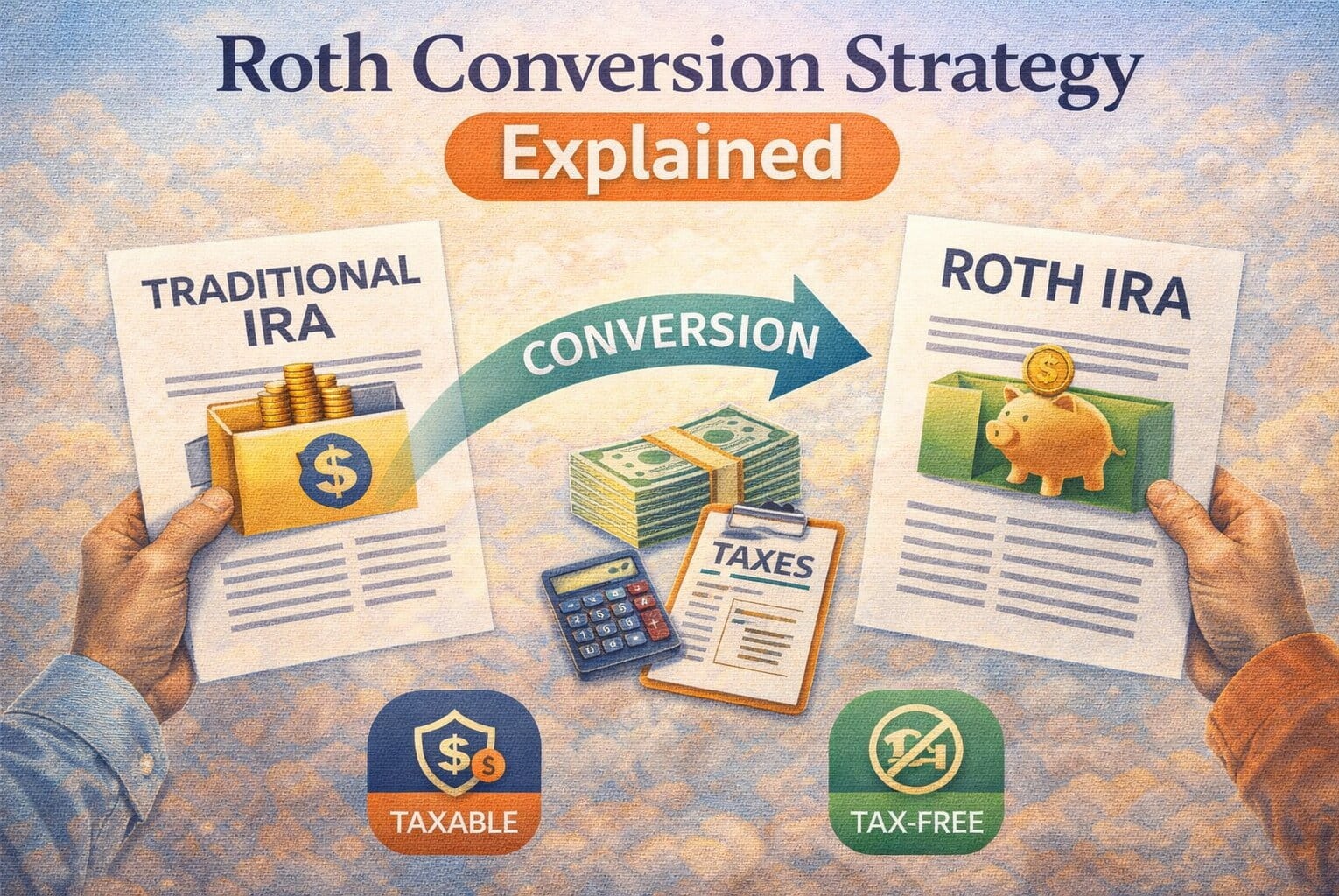

You move money from a tax-deferred account (like a Traditional IRA) into a Roth IRA—and pay taxes now instead of later.

But the real value comes from when and how you do it. Done correctly, a Roth conversion can reduce lifetime taxes, increase flexibility, and create tax-free income in retirement.

Let’s break it down step by step.

What Is a Roth Conversion?

A Roth conversion is the process of transferring funds from:

- Traditional IRA → Roth IRA

- 401(k) → Roth IRA (via rollover)

When you convert:

- You pay income tax on the amount converted

- Future growth becomes tax-free

Why Consider a Roth Conversion?

The main goal is to pay taxes at a lower rate now to avoid higher taxes later.

Benefits include:

- Tax-free withdrawals in retirement

- No Required Minimum Distributions (RMDs)

- Greater flexibility in income planning

Simple Example

Case Study:

- You convert $50,000 from a Traditional IRA

- You’re in the 22% tax bracket

Taxes owed:

- ~$11,000

But later:

- That $50,000 grows to $150,000

- You withdraw it tax-free

That’s the long-term advantage.

When Does a Roth Conversion Make Sense?

Timing is everything.

A Roth conversion works best when:

1. You’re in a Lower Tax Bracket Today

Example:

- Early retirement years before Social Security starts

- Temporary drop in income

2. You Expect Higher Taxes Later

This could happen if:

- Tax rates increase

- Your retirement income is high

3. You Want Tax-Free Income in Retirement

Having a Roth account gives you flexibility:

- Withdraw without increasing taxable income

- Control your tax bracket

Roth Conversion vs Regular Contributions

| Feature | Roth Contribution | Roth Conversion |

|---|---|---|

| Source of Funds | New income | Existing retirement funds |

| Taxes Paid | Already paid | Paid at conversion |

| Income Limits | Yes | No |

| Purpose | Ongoing saving | Tax strategy |

Both are useful—but conversions are more strategic.

To understand contributions:

https://statush.com/retirement-planning/how-roth-ira-contributions-work

Step-by-Step Roth Conversion Process

- Choose how much to convert

- Transfer funds to a Roth IRA

- Pay taxes on the converted amount

- Invest the funds for growth

That’s it—but the strategy lies in how much and when.

Real-World Strategy Example

Case Study:

- Age: 60

- Retired but not yet claiming Social Security

- Low taxable income

Strategy:

- Convert $40,000/year from Traditional IRA

- Stay within a lower tax bracket

Over 5–7 years:

- Significant portion moved to Roth

- Future taxes reduced

Partial Conversions: The Smart Approach

Instead of converting everything at once, many people use partial conversions.

Why?

- Avoid jumping into a higher tax bracket

- Spread tax impact over multiple years

Example:

- Convert $30,000/year instead of $150,000 at once

This keeps taxes manageable.

Tax Impact of Roth Conversions

The biggest downside is immediate taxation.

Important considerations:

- Conversion amount is added to your income

- Can push you into a higher tax bracket

- May affect Medicare premiums

To manage taxes effectively:

https://statush.com/retirement-planning/how-to-reduce-taxes-in-retirement

Roth Conversion and RMDs

Traditional IRAs require Required Minimum Distributions (RMDs).

Roth IRAs:

- Do NOT require RMDs

This makes Roth conversions useful for:

- Reducing future mandatory withdrawals

- Controlling taxable income

To understand withdrawal rules:

https://statush.com/retirement-planning/traditional-ira-withdrawal-rules-explained

How Roth Conversion Fits Into Your Retirement Plan

A Roth conversion is not a standalone strategy—it works best when combined with:

- Withdrawal planning

- Tax strategy

- Income planning

Example:

- Use Traditional IRA for early withdrawals

- Use Roth IRA later for tax-free income

To build a full strategy:

https://statush.com/retirement-planning/retirement-income-planning-strategies

Common Mistakes to Avoid

- Converting too much at once

- Ignoring tax brackets

- Not planning for tax payments

- Converting without a long-term strategy

For more pitfalls:

https://statush.com/retirement-planning/retirement-mistakes-to-avoid

When Roth Conversion May Not Be Ideal

It may not make sense if:

- You’re already in a high tax bracket

- You need the money soon

- You can’t afford the tax bill

Timing and planning are critical.

How It Helps Long-Term

A well-executed Roth conversion can:

- Reduce lifetime taxes

- Provide tax-free income

- Increase financial flexibility

- Simplify estate planning

Final Thoughts

A Roth conversion is a powerful tool—but only when used strategically.

It’s not about avoiding taxes—it’s about choosing when to pay them.

Paying taxes at the right time can save you significantly over the long run and give you more control over your retirement income.

If used correctly, a Roth conversion can turn a tax-deferred future into a tax-free one—and that’s a major advantage in retirement planning.

To align this strategy with your overall savings goals, start here:

https://statush.com/retirement-planning/how-much-should-you-save-for-retirement-by-age