Retirement accounts are the single most powerful legal tax shelter available to ordinary Americans. Unlike complex strategies reserved for the wealthy, these accounts are available to almost anyone with earned income — and the tax benefits are extraordinary.

Contributing $24,500 to a 401(k) in 2026 doesn't just grow your retirement savings. It reduces your taxable income by $24,500 right now — potentially saving you $5,390 to $9,065 in federal taxes this year alone, depending on your bracket. Add a spousal contribution, an IRA, and an HSA, and a married couple can shelter over $75,000 from taxes in a single year.

This guide breaks down every major retirement account available in 2026, what each one saves you in taxes, and how to stack them for maximum benefit.

Why Retirement Accounts Are the Foundation of Tax Planning

Before diving into specific accounts, it helps to understand the three tax advantages these accounts can offer — individually or in combination:

| Tax Benefit | What It Means |

|---|---|

| Tax deduction on contributions | Money you contribute reduces your taxable income today |

| Tax-deferred growth | Investments grow without being taxed each year |

| Tax-free withdrawals | Money comes out in retirement completely free of tax |

Most accounts offer two of these three. The HSA — which we'll cover below — offers all three, making it the rarest and most valuable account type in the entire tax code.

To understand how reducing taxable income through retirement contributions interacts with your overall tax situation, see our guide: What Is Taxable Income.

2026 Retirement Account Contribution Limits at a Glance

(Per IRS Notice 2025-67 — effective January 1, 2026)

| Account Type | 2026 Limit | Age 50+ Catch-Up | Age 60–63 Super Catch-Up |

|---|---|---|---|

| 401(k) / 403(b) / 457 / TSP | $24,500 | +$8,000 (total $32,500) | +$11,250 (total $35,750) |

| Traditional IRA / Roth IRA | $7,500 | +$1,100 (total $8,600) | N/A |

| SIMPLE IRA | $17,000 | +$4,000 (total $21,000) | +$5,250 |

| SEP IRA | $72,000 | N/A | N/A |

| HSA (self-only) | $4,400 | +$1,000 at age 55+ | N/A |

| HSA (family) | $8,750 | +$1,000 at age 55+ | N/A |

A married couple, both over 50, each contributing to a 401(k) and an IRA, can shelter a combined $82,200 from federal income taxes in 2026 — before even counting employer matches or HSA contributions.

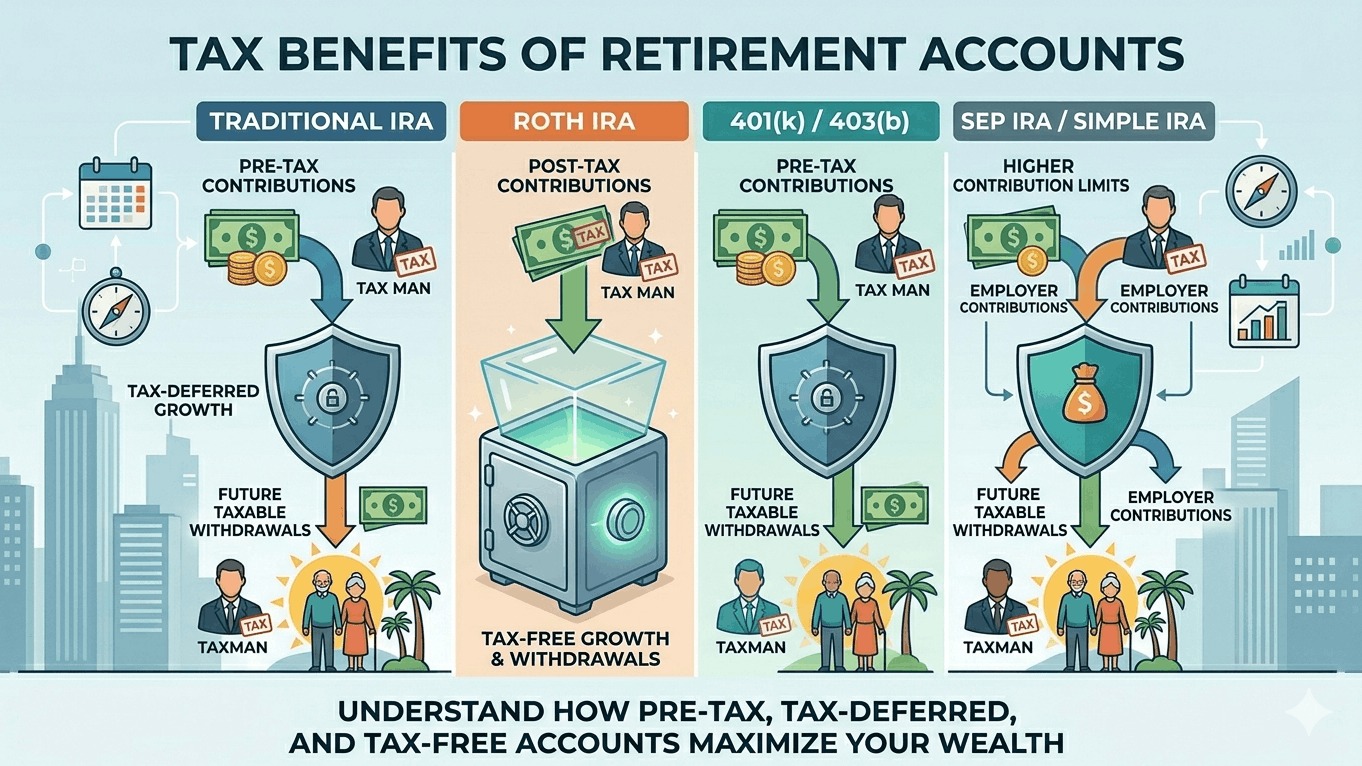

The 401(k): America's Most Common Retirement Tax Break

The 401(k) is the workhorse of American retirement savings. If your employer offers one, it is almost always the first account you should maximize.

How the Tax Benefit Works

Traditional 401(k) contributions are made pre-tax, meaning they are deducted from your paycheck before income tax is calculated. Your taxable income drops dollar-for-dollar.

Example: You earn $90,000 and contribute $24,500 to your 401(k) in 2026.

- Taxable income falls from $90,000 to $65,500

- At the 22% marginal bracket, your federal tax savings: $5,390

- Your actual out-of-pocket cost for a $24,500 contribution is only $19,110

Inside the account, all investments — dividends, capital gains, interest — grow completely tax-deferred. You pay no tax until you withdraw in retirement.

2026 401(k) Key Numbers

- Employee contribution limit: $24,500 (up from $23,500 in 2025)

- Age 50+ catch-up: Additional $8,000 (total $32,500)

- Ages 60–63 "super catch-up": Additional $11,250 (total $35,750) — introduced by SECURE 2.0

- Total limit including employer contributions: $70,000

New in 2026 — Mandatory Roth catch-ups: Under SECURE 2.0, employees who earned more than $150,000 in FICA wages from their employer in 2025 must make their 2026 catch-up contributions as Roth (after-tax) contributions rather than pre-tax. This applies to catch-up amounts above the standard $24,500 deferral limit.

Employer Match: The Best Return in Investing

Many employers match a percentage of your 401(k) contributions — typically 50%–100% of the first 3%–6% of your salary. This is an immediate 50%–100% return on your contribution before investment growth begins. Always contribute at least enough to capture the full employer match. Leaving a match on the table is leaving free money — and a free tax deduction — behind.

The Roth 401(k) Option

Many employers now offer a Roth 401(k) alongside the traditional option. Contributions are made after-tax — no deduction now — but all future growth and withdrawals are completely tax-free. The same $24,500 contribution limit applies to both, and you can split contributions between traditional and Roth 401(k) in any proportion.

Understanding which bracket you're in today — and whether you expect a higher or lower rate in retirement — determines which option is more valuable. See our full guide: How Tax Brackets Work.

Traditional IRA: A Deduction Anyone Can Access

An Individual Retirement Account (IRA) is available to anyone with earned income, regardless of whether their employer offers a retirement plan.

2026 Traditional IRA Key Numbers

- Contribution limit: $7,500 (up from $7,000 in 2025)

- Age 50+ catch-up: Additional $1,100 (total $8,600)

- Tax benefit: Contributions may be fully deductible, reducing taxable income now

Deductibility Phase-Out Rules for 2026

The deduction for traditional IRA contributions is subject to income limits if you or your spouse is covered by a workplace retirement plan:

Covered by a workplace plan — Single filers:

- Full deduction: MAGI up to $81,000

- Partial deduction: $81,001 – $91,000

- No deduction: Over $91,000

Covered by a workplace plan — Married filing jointly:

- Full deduction: MAGI up to $136,000 (for the covered spouse)

- Partial deduction: $136,001 – $156,000

- No deduction: Over $156,000

Not covered, but spouse is covered — Married filing jointly:

- Full deduction: MAGI up to $242,000

- Partial deduction: $242,001 – $252,000

- No deduction: Over $252,000

If neither you nor your spouse is covered by a workplace plan, your traditional IRA contributions are always fully deductible regardless of income.

Tax-Deferred Growth

Whether or not your contribution is deductible, all growth inside a traditional IRA is tax-deferred. Dividends, capital gains, and interest accumulate without annual taxation — a major advantage over taxable brokerage accounts where these are taxed each year. Compare how dividends and capital gains in taxable accounts are taxed in our guides: Capital Gains Tax Explained and Short-Term vs Long-Term Capital Gains Taxes.

Withdrawals

Traditional IRA withdrawals in retirement are taxed as ordinary income at whatever bracket you fall into at that time. Withdrawals before age 59½ generally trigger a 10% early withdrawal penalty on top of income tax, with limited exceptions (first home purchase, disability, substantially equal periodic payments, etc.).

Required Minimum Distributions (RMDs) begin at age 73, meaning you must start withdrawing a portion each year whether you need the money or not.

Roth IRA: Tax-Free Growth Forever

The Roth IRA is the mirror image of the traditional IRA. You contribute after-tax dollars today, receive no deduction — and everything that grows inside the account comes out completely tax-free in retirement.

2026 Roth IRA Key Numbers

- Contribution limit: $7,500 (same as traditional IRA — total is shared)

- Age 50+ catch-up: Additional $1,100 (total $8,600)

- Tax benefit: No deduction now, but all qualified withdrawals are tax-free

2026 Roth IRA Income Limits

Unlike the traditional IRA, the Roth IRA has hard income limits that restrict who can contribute directly:

| Filing Status | Full Contribution | Partial Contribution | No Contribution |

|---|---|---|---|

| Single / Head of Household | MAGI up to $153,000 | $153,001 – $168,000 | Over $168,000 |

| Married Filing Jointly | MAGI up to $242,000 | $242,001 – $252,000 | Over $252,000 |

| Married Filing Separately | $0 | $0 – $10,000 | Over $10,000 |

Backdoor Roth IRA: High earners above these limits can still access the Roth IRA through a legal strategy — contributing to a non-deductible traditional IRA and then converting it to a Roth. This "backdoor" method remains fully legal in 2026.

Why the Roth IRA is So Powerful

- No RMDs: Unlike traditional IRAs and 401(k)s, Roth IRAs have no required minimum distributions during the account owner's lifetime. Your money can compound indefinitely.

- Tax-free inheritance: Roth IRAs can be passed to heirs, who also benefit from tax-free growth (subject to 10-year withdrawal rules for most non-spouse beneficiaries)

- Flexible withdrawals: Contributions (not earnings) can be withdrawn at any time without penalty — making the Roth IRA also function as a flexible emergency backup fund

A Roth IRA is particularly valuable for younger investors who expect to be in a higher tax bracket in retirement than they are today, and for anyone who wants to hold high-growth, high-dividend investments tax-free over decades.

HSA: The Only Triple Tax-Advantaged Account in the U.S. Tax Code

The Health Savings Account (HSA) is the most tax-efficient account available to any American — and the most underused. It offers a benefit no other account can match: all three tax advantages at once.

- Contributions are tax-deductible (or pre-tax if made through payroll)

- Investments grow tax-deferred inside the account

- Withdrawals are tax-free when used for qualified medical expenses

This triple tax benefit means every dollar you contribute to an HSA is worth more than a dollar contributed to any other account type.

2026 HSA Key Numbers

- Self-only coverage: $4,400 (up from $4,300 in 2025)

- Family coverage: $8,750 (up from $8,550 in 2025)

- Age 55+ catch-up: Additional $1,000 (per eligible person)

- Eligibility: Must be enrolled in a qualifying High-Deductible Health Plan (HDHP)

New for 2026: The One Big Beautiful Bill Act expanded HSA eligibility — Bronze and Catastrophic health plans from ACA Marketplaces are now HSA-compatible, opening access to millions more Americans who previously couldn't contribute.

The HSA as a Retirement Account

Most people treat their HSA as a healthcare spending account. The real strategy is to treat it as a stealth retirement account:

- Pay out-of-pocket medical expenses with cash today (save the receipts)

- Let the HSA balance grow invested in index funds for decades

- After age 65, withdraw for any purpose — medical expenses are tax-free, non-medical withdrawals are taxed as ordinary income (same as a traditional IRA)

- Or: Reimburse yourself decades later for those old medical receipts — completely tax-free, no time limit on reimbursement

A couple both aged 55 or older can contribute $9,750 in 2026 (each in their own HSA) — all triple-tax-advantaged.

SEP IRA: The Self-Employed Power Move

For self-employed individuals, freelancers, and small business owners, the SEP IRA (Simplified Employee Pension) offers one of the largest contribution limits of any retirement account.

2026 SEP IRA Key Numbers

- Maximum contribution: $72,000 (up from $70,000 in 2025)

- Contribution rate: Up to 25% of compensation (for employees) or approximately 20% of net self-employment income

- Tax benefit: Contributions are fully tax-deductible as a business expense

A self-employed consultant earning $360,000 in net income can contribute $72,000 to a SEP IRA in 2026 — deducting every dollar from both income tax and self-employment tax. The SEP IRA requires almost no administrative overhead, making it ideal for solo operators.

SIMPLE IRA: Small Business's 401(k) Alternative

For small businesses with 100 or fewer employees, the SIMPLE IRA (Savings Incentive Match Plan for Employees) provides a cost-effective retirement plan option without the administrative complexity of a full 401(k).

2026 SIMPLE IRA Key Numbers

- Employee contribution limit: $17,000 (up from $16,500 in 2025)

- Age 50+ catch-up: Additional $4,000 (total $21,000)

- Ages 60–63 super catch-up: Additional $5,250 (total $22,250)

- Employer requirement: Employers must either match up to 3% of compensation or contribute 2% flat for all eligible employees

The Saver's Credit: Extra Tax Relief for Lower-Income Earners

On top of all the deductions and tax-free growth above, lower- and moderate-income workers who contribute to a retirement account qualify for the Saver's Credit — a direct dollar-for-dollar reduction in tax owed (not just a deduction).

2026 Saver's Credit Income Limits

| Filing Status | Full Credit Threshold | Phase-Out Ends |

|---|---|---|

| Married Filing Jointly | Up to $80,500 | — |

| Head of Household | Up to $60,375 | — |

| Single / Married Filing Separately | Up to $40,250 | — |

The credit is worth up to $1,000 per person ($2,000 for married couples) — on top of any tax deduction from the contribution itself. That means a qualifying couple could reduce their tax bill by $2,000 in credits while also deducting up to $49,000 in contributions. This is one of the most generous combined incentives in the tax code for working families.

How Retirement Contributions Reduce Your Taxable Income: A Real Example

Meet Kevin and Maria, married filing jointly, earning a combined $160,000 in 2026.

Without any retirement contributions:

- Standard deduction: −$32,200

- Taxable income: $127,800

- Estimated federal tax (at 22% marginal rate): ~$18,179

With maximum retirement contributions:

- Kevin's 401(k): −$24,500

- Maria's 401(k): −$24,500

- Kevin's IRA: −$7,500

- Maria's IRA: −$7,500

- HSA (family): −$8,750

- Standard deduction: −$32,200

- Taxable income: $55,050

- Estimated federal tax (at 12% marginal rate): ~$5,350

Total federal tax savings: $12,829 — just from using accounts they already have access to. They also dropped from the 22% bracket to the 12% bracket entirely.

To see how these income layers interact with your overall federal tax calculation, read: How Income Taxes Work in the USA.

Account Placement Strategy: Which Investments Go Where

Not all investments belong in all accounts. Strategic placement maximizes after-tax returns across your entire portfolio.

| Investment Type | Best Account | Why |

|---|---|---|

| High-growth stocks | Roth IRA / Roth 401(k) | All gains come out tax-free |

| REITs / high-yield bonds | Traditional IRA / 401(k) | Shield ordinary-income-producing assets from current tax |

| Qualified dividend stocks | Taxable brokerage | Already taxed at favorable 0%/15%/20% rate — no benefit to sheltering |

| Index funds (low turnover) | Taxable brokerage | Minimal annual tax drag, long-term capital gains rates apply |

| Medical expense investments | HSA | Triple tax benefit — best possible treatment |

Traditional vs. Roth: How to Choose

The fundamental question in retirement account planning is whether to pay taxes now (Roth) or later (traditional/pre-tax). The answer depends on your tax situation:

Choose Traditional (Pre-Tax) if:

- You are in a higher tax bracket today than you expect to be in retirement

- You need the current-year deduction to manage your tax bill

- You are approaching retirement and want to reduce income now

Choose Roth if:

- You are in a lower bracket today and expect higher income in retirement

- You are young and expect decades of tax-free compounding

- You want to avoid RMDs and preserve flexibility

- Your income is near a key threshold (like the 0% capital gains bracket or NIIT threshold) — reducing current taxable income may not save much, making the Roth's future tax-free value more compelling

For most people in the 22% bracket or below, the Roth is mathematically favored. For those in the 32% bracket and above, the traditional pre-tax deduction typically wins.

To understand how deductions and tax brackets interact with this decision, see: Standard Deduction vs Itemized Deduction and How Tax Brackets Work.

State Tax Considerations

Federal tax benefits are only half the picture. Most states also follow federal rules for retirement account deductions, but there are important exceptions:

- Most states: Mirror the federal deduction for traditional 401(k) and IRA contributions, providing a state income tax deduction as well

- Pennsylvania and New Jersey: Do not allow a deduction for traditional IRA or 401(k) contributions — but also do not tax qualified retirement distributions, effectively creating a different kind of tax deferral

- No income tax states (Texas, Florida, Nevada, etc.): No state income tax, so the only benefit is federal

For more on how federal and state tax systems interact, see: Federal vs State Taxes Explained.

2026 Complete Retirement Account Reference Table

| Account | 2026 Limit | Catch-Up (50+) | Tax on Contributions | Tax on Growth | Tax on Withdrawal |

|---|---|---|---|---|---|

| Traditional 401(k) | $24,500 | +$8,000 | Pre-tax (deductible) | Tax-deferred | Ordinary income |

| Roth 401(k) | $24,500 | +$8,000* | After-tax | Tax-free | Tax-free |

| Traditional IRA | $7,500 | +$1,100 | Pre-tax (if eligible) | Tax-deferred | Ordinary income |

| Roth IRA | $7,500 | +$1,100 | After-tax | Tax-free | Tax-free |

| SEP IRA | $72,000 | N/A | Pre-tax (deductible) | Tax-deferred | Ordinary income |

| SIMPLE IRA | $17,000 | +$4,000 | Pre-tax (deductible) | Tax-deferred | Ordinary income |

| HSA | $4,400 / $8,750 | +$1,000 (age 55+) | Pre-tax (deductible) | Tax-deferred | Tax-free (medical) |

*High-income earners (>$150,000 FICA wages) must make 401(k) catch-up contributions as Roth starting in 2026.

Final Thoughts

Retirement accounts are not just about saving for the future — they are one of the most effective ways to legally reduce what you pay in taxes right now. The combination of upfront deductions, tax-deferred or tax-free compounding, and strategic account placement can save the average American household tens of thousands of dollars over a working career.

In 2026, with 401(k) limits at $24,500, IRA limits at $7,500, and HSA limits at $8,750, the total shelter available to a working American is higher than it has ever been. The question is not whether to use these accounts — it is which combination to use and in what order.

For a complete picture of how all of these savings feed into your overall income tax calculation, start with our comprehensive guide: How Income Taxes Work in the USA.