When filing taxes in the United States, one of the most important decisions you’ll make is choosing between the standard deduction vs itemized deduction.

This choice directly impacts your taxable income, which determines how much tax you owe.

The good news? Understanding this concept is easier than it sounds—and choosing the right option can save you thousands of dollars.

What Is a Tax Deduction?

A tax deduction reduces your taxable income, meaning you pay tax on a lower amount.

The Internal Revenue Service (IRS) allows taxpayers to choose between:

- A fixed deduction (standard deduction)

- A list of actual expenses (itemized deductions)

Related: What Is Taxable Income

What Is the Standard Deduction?

The standard deduction is a fixed amount you can subtract from your income, no questions asked.

Key Features:

- Simple and quick

- No need to track expenses

- Used by most taxpayers

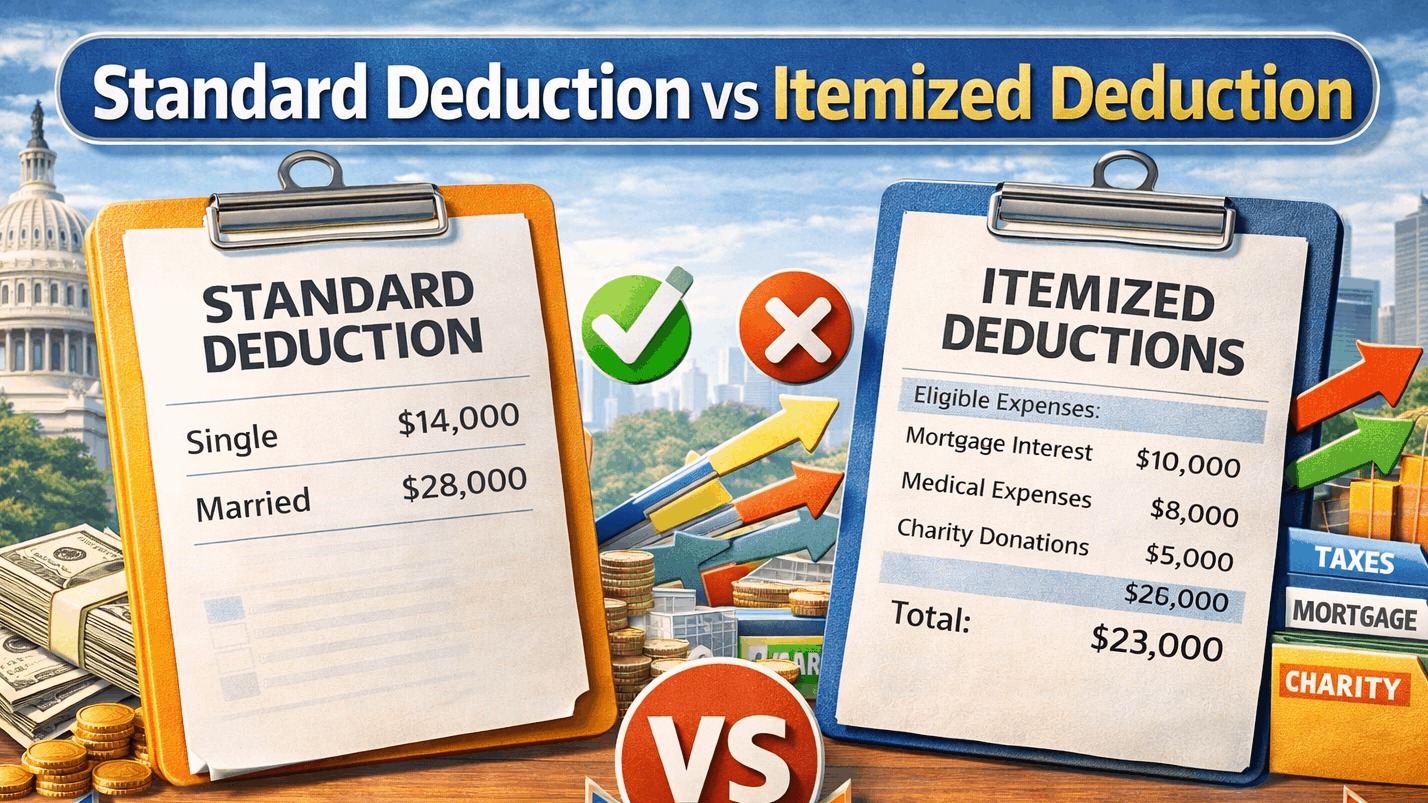

Example (Approximate Values for 2026):

- Single: ~$14,000

- Married Filing Jointly: ~$28,000

These amounts may change slightly each year due to inflation.

What Is Itemized Deduction?

The itemized deduction allows you to deduct specific eligible expenses instead of taking the standard amount.

Common Itemized Deductions:

- Mortgage interest

- Medical expenses

- State and local taxes (SALT)

- Charitable donations

Related: How Income Taxes Work in the USA

Standard Deduction vs Itemized Deduction: Key Differences

| Feature | Standard Deduction | Itemized Deduction |

|---|---|---|

| Type | Fixed amount | Based on expenses |

| Complexity | Very simple | Requires documentation |

| Popularity | Used by most taxpayers | Used less frequently |

| Flexibility | No customization | Highly customizable |

| Best For | Salaried individuals | Homeowners, high spenders |

How to Choose Between Standard and Itemized Deduction

The rule is simple:

Choose the option that gives you the larger deduction

Use Standard Deduction If:

- You don’t have many deductible expenses

- You want a simple filing process

- Your expenses are lower than the standard deduction

Use Itemized Deduction If:

- Your expenses exceed the standard deduction

- You own a home

- You made large charitable donations

Real-Life Example

Scenario 1: Standard Deduction Wins

- Income: $60,000

- Itemized expenses: $8,000

- Standard deduction: $14,000

Choose standard deduction (higher amount)

Scenario 2: Itemized Deduction Wins

- Income: $80,000

- Itemized expenses:

- Mortgage interest: $12,000

- Taxes: $8,000

- Donations: $5,000

- Total: $25,000

Choose itemized deduction (higher than standard)

How Deductions Impact Your Taxes

Deductions reduce your taxable income, not your total income.

Example:

- Income: $70,000

- Deduction: $14,000

- Taxable Income: $56,000

You only pay tax on $56,000.

Related: Federal vs State Taxes Explained

When Itemizing Makes Sense

Itemizing is beneficial if you:

- Own a house (high mortgage interest)

- Pay high state taxes

- Donate regularly to charity

- Have significant medical expenses

Related: How to Manage Investment Risk

Common Mistakes to Avoid

- Choosing itemized without calculating properly

- Forgetting eligible deductions

- Not keeping proper documentation

- Assuming itemizing is always better

Why This Decision Matters

Choosing between standard deduction vs itemized deduction can:

- Reduce your taxable income

- Lower your tax bill

- Improve your financial planning

Even a small difference can result in significant savings.

Final Thoughts

So, standard deduction vs itemized deduction—what’s better?

There’s no one-size-fits-all answer.

- Standard deduction = simple and fast

- Itemized deduction = detailed but potentially more beneficial

The best choice is always the one that gives you the maximum tax savings.