Short-Term vs. Long-Term Capital Gains Taxes: What Every U.S. Investor Needs to Know in 2026

When you sell an investment for a profit, the IRS doesn't just ask how much you made — it asks how long you held it. That single question can be the difference between paying 37% and paying 0% on the exact same profit.

This is the short-term vs. long-term capital gains distinction, and it is one of the most powerful — and most underused — tools in personal finance. This guide breaks it all down with the latest 2026 IRS numbers, real-world examples, and actionable strategies to keep more of what you earn.

For a full overview of how capital gains tax works from the ground up, start with our guide: Capital Gains Tax Explained.

The Core Difference: One Rule, Massive Impact

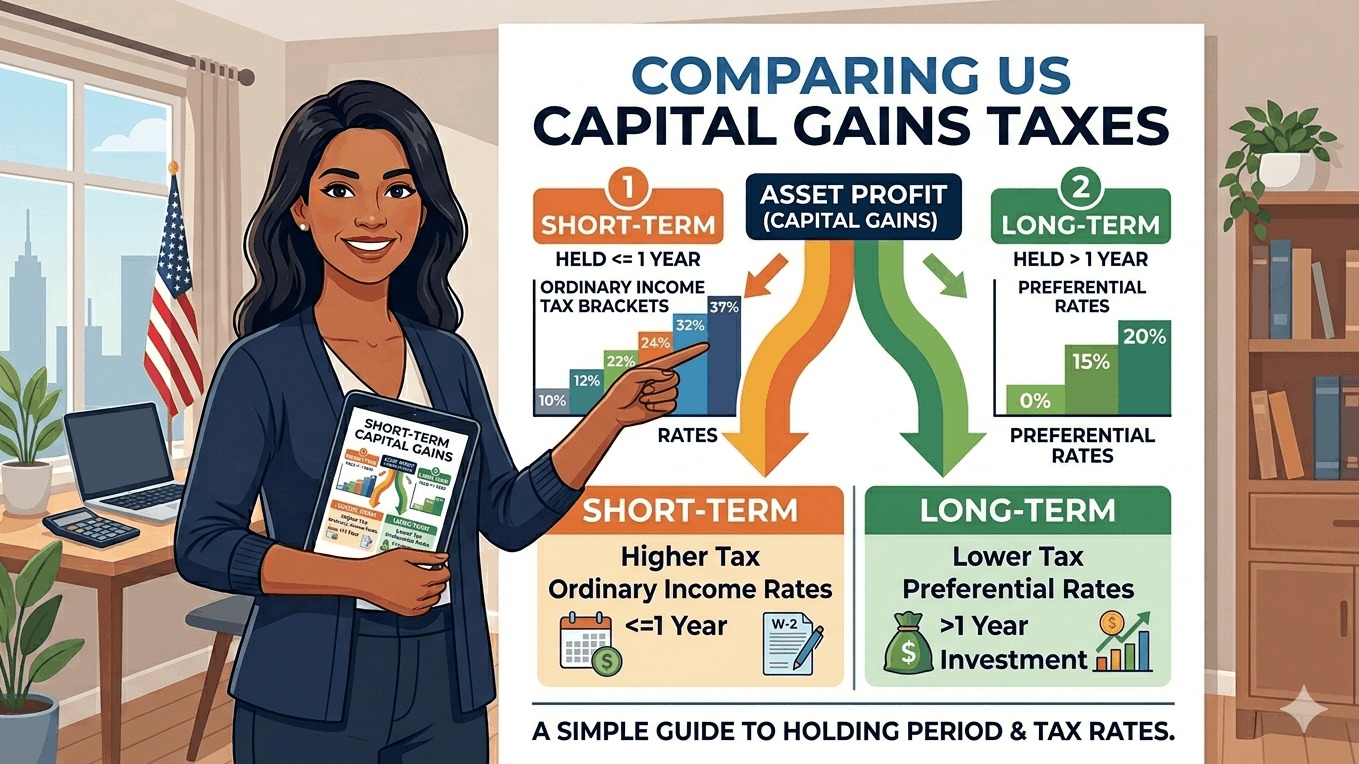

The IRS divides all capital gains into two categories based entirely on your holding period — the time between when you bought and when you sold the asset:

| Type | Holding Period | 2026 Tax Treatment |

|---|---|---|

| Short-Term Capital Gain | 365 days or less | Taxed as ordinary income — same as wages (10%–37%) |

| Long-Term Capital Gain | 366 days or more | Taxed at preferential rates of 0%, 15%, or 20% |

There is no gray area. Sell on day 365 and you owe short-term rates. Wait until day 366 and you qualify for long-term rates. That one-day difference can mean thousands of dollars in tax savings.

2026 Short-Term Capital Gains Tax Rates

Short-term gains get no preferential treatment — they are taxed at the same rates as your wages, salary, and other ordinary income. Unlike the long-term capital gains tax rate, there is no 0% rate or 20% ceiling for short-term capital gains taxes.

2026 Short-Term Rates (Single Filers) — Same as Ordinary Income Brackets:

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 – $12,400 |

| 12% | $12,401 – $50,250 |

| 22% | $50,251 – $105,700 |

| 24% | $105,701 – $201,900 |

| 32% | $201,901 – $256,100 |

| 35% | $256,101 – $640,600 |

| 37% | Over $640,600 |

A trader who flips stocks in days or weeks is taxed exactly like a salaried employee — at their full marginal income bracket. There is no cap and no discount.

Side-by-Side Rate Comparison: 2026

This table shows exactly how stark the difference is between the two tax treatments at the same income levels:

| Your Taxable Income (Single) | Short-Term Rate | Long-Term Rate | Potential Savings |

|---|---|---|---|

| Up to $49,450 | 10%–12% | 0% | Up to 12% |

| $49,451 – $105,700 | 22% | 15% | 7% |

| $105,701 – $543,350 | 24%–35% | 15% | 9%–20% |

| Over $543,350 | 37% | 20% | 17% |

The gap is widest in the middle income ranges, where the difference between short-term and long-term rates can be as large as 20 percentage points.

How Holding Period Is Counted: The Exact Rule

The IRS is precise about how holding periods are measured. The rules matter more than most investors realize:

- Start date: The day after you acquire the asset (the acquisition date itself does not count)

- End date: The day you sell the asset (this date counts)

- Threshold: You must hold the asset for more than one year — meaning at least 366 days — to qualify for long-term rates

Example: You buy a stock on March 25, 2026. To qualify for long-term treatment, you must sell no earlier than March 26, 2027. Selling on March 25, 2027 — exactly one year later — would still be short-term.

Special cases to know:

- Inherited assets: Property inherited from a deceased person automatically qualifies for long-term treatment, regardless of how long the heir actually holds it

- Gifted assets: The recipient generally inherits the original owner's holding period

- Wash-sale rule: If you sell a security at a loss and repurchase a substantially identical one within 30 days before or after the sale, the loss is disallowed — the holding period resets

Real-World Example: The Cost of Selling Too Early

Meet Sarah, a single filer with $75,000 in taxable income in 2026. She bought stock for $10,000 and later sold it for $25,000 — a $15,000 profit.

Scenario A — Sold after 10 months (Short-Term): Her $15,000 gain is added to ordinary income and taxed at her marginal rate of 22%.

- Tax on $15,000 gain: $3,300

Scenario B — Sold after 14 months (Long-Term): Her taxable income of $75,000 places her in the 15% long-term capital gains bracket.

- Tax on $15,000 gain: $2,250

Sarah saves $1,050 simply by waiting four more months.

Now scale this up. On a $150,000 gain, the same patience saves $10,500. On a $500,000 gain, it saves $35,000 or more — just from timing.

The 0% Rate: A Powerful Planning Opportunity in 2026

For 2026, single filers can earn up to $49,450 in taxable income — or $98,900 for married couples filing jointly — and still pay 0% for long-term capital gains. This opens up a significant tax planning opportunity many Americans overlook.

Who benefits most from the 0% rate:

- Retirees living on savings with modest income

- Early-career investors in lower income brackets

- Part-time workers or freelancers in lower-earning years

- Anyone whose taxable income drops below the threshold in a given year (due to deductions, retirement contributions, etc.)

Strategy — "Gain harvesting": If your taxable income is below $49,450 (single) or $98,900 (married), you can sell appreciated long-term investments, lock in gains, and owe zero federal capital gains tax. You can then immediately repurchase the same assets at the new higher cost basis — effectively resetting your basis tax-free. This is the mirror image of tax-loss harvesting and is completely legal.

Remember: taxable income is calculated after the standard deduction. In 2026, the standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. This means a single filer with gross income of around $65,550 or less could still fall within the 0% long-term capital gains zone.

Asset-by-Asset Breakdown: How Different Investments Are Taxed in 2026

Not all assets follow the standard 0%/15%/20% long-term schedule. Here is how specific asset types are treated:

| Asset Type | Short-Term Rate | Long-Term Rate |

|---|---|---|

| Stocks & ETFs | Ordinary income (up to 37%) | 0%, 15%, or 20% |

| Mutual funds | Ordinary income (up to 37%) | 0%, 15%, or 20% |

| Cryptocurrency | Ordinary income (up to 37%) | 0%, 15%, or 20% |

| Real estate (investment) | Ordinary income (up to 37%) | 0%, 15%, or 20% |

| Collectibles (art, coins, gold) | Ordinary income (up to 37%) | Max 28% |

| Small business stock (Sec. 1202) | Ordinary income (up to 37%) | Max 28% |

| Real estate depreciation recapture | Ordinary income (up to 37%) | Max 25% |

Cryptocurrency note for 2026: The IRS treats crypto as property, so the same short-term/long-term rules apply to every sale, trade, or exchange. Starting in 2026, crypto brokers are required to report transactions directly to the IRS via Form 1099-DA, making accurate record-keeping essential for all crypto investors.

The Net Investment Income Tax (NIIT): The Extra 3.8%

High-income earners face an additional 3.8% Net Investment Income Tax on top of their capital gains rate. This surcharge applies to:

- Single filers with modified AGI over $200,000

- Married filing jointly with modified AGI over $250,000

This threshold has not been adjusted for inflation since it was introduced, meaning more taxpayers are gradually pulled in each year. For top earners, the NIIT effectively pushes the maximum long-term capital gains rate to 23.8% (20% + 3.8%).

How Losses Offset Gains: Short-Term vs. Long-Term Rules

Capital losses must first be matched against gains of the same type — then they can cross over:

Step 1 — Same-type netting:

- Short-term losses offset short-term gains first

- Long-term losses offset long-term gains first

Step 2 — Cross-type netting:

- If one category still has a net loss after Step 1, it offsets the other category's net gain

Step 3 — Ordinary income offset:

- If total capital losses exceed total capital gains, up to $3,000 per year can be deducted against ordinary income ($1,500 if married filing separately)

- Remaining losses carry forward indefinitely to future tax years

Why the type distinction matters for losses: A net short-term loss offsets short-term gains (which would have been taxed at high ordinary rates) — so matching short-term losses against short-term gains gives you the most valuable deduction. Planning the timing of your loss realizations can significantly affect how much tax you save.

6 Strategies to Minimize Your Capital Gains Tax in 2026

1. Always hold for at least 366 days The most straightforward strategy. Converting a short-term gain into a long-term one can cut your tax rate by 7–20+ percentage points depending on your income.

2. Harvest gains at the 0% rate If your taxable income is below $49,450 (single) or $98,900 (married), realize long-term gains now — you owe nothing federally. Then repurchase at the higher cost basis to reduce future gains.

3. Use tax-loss harvesting to offset gains Sell underperforming investments to generate capital losses that cancel out gains. Even if you repurchase similar (not identical) investments immediately, the loss still counts. Watch the 30-day wash-sale window.

4. Invest through tax-advantaged accounts Inside a 401(k), IRA, Roth IRA, HSA, or 529, capital gains are either deferred or completely tax-free. Your highest-growth investments belong in these accounts. Investment earnings within these accounts aren't taxed until you take distributions in retirement, and in the case of a Roth IRA, the investment earnings aren't taxed at all, provided you follow the Roth IRA rules.

5. Time your sales across tax years If you are close to the end of the year and near a threshold, consider whether pushing a sale into January keeps you in a lower bracket. This is especially powerful when straddling the 0%/15% line.

6. Gift appreciated shares instead of cash Rather than selling appreciated stock (and paying tax), gift the shares directly to a family member in a lower bracket or to a charity. The charity pays no capital gains tax. Family members in the 0% bracket can sell and owe nothing federally.

Common Mistakes Investors Make With Capital Gains in 2026

Selling too early out of anxiety. Market dips sometimes push investors to sell before the one-year mark. Holding through short-term volatility often saves thousands in taxes — in addition to potential investment upside.

Ignoring the holding period on reinvested dividends. Each dividend reinvestment creates a new lot with its own holding period. Selling shares that include recently reinvested dividends may trigger short-term rates on that portion.

Forgetting crypto is taxable. Every crypto trade — including swapping one coin for another — is a taxable event. With Form 1099-DA now in effect, the IRS has direct visibility into these transactions.

Not accounting for the NIIT. Investors near the $200,000/$250,000 MAGI threshold can sometimes restructure income to stay below it — eliminating the extra 3.8% surcharge.

Not using losses strategically. Many investors let capital losses expire without using them to offset gains. Proactive tax-loss harvesting throughout the year — not just in December — is a year-round discipline.

Final Thoughts

The distinction between short-term and long-term capital gains is one of the clearest examples in the entire U.S. tax code where timing — not strategy, not complexity — determines your outcome. Waiting 366 days instead of 365 can legally slash your tax bill by up to 20 percentage points. Staying within the 0% long-term bracket means paying nothing at all on your investment profits.

In 2026, with the 0% rate threshold for married couples at $98,900 and the standard deduction at $32,200, more American investors than ever have room to realize long-term gains tax-free. The question is whether you plan for it — or leave it on the table.

For a complete breakdown of all capital gains rules, special rates, home sale exclusions, and crypto guidance, read our full reference guide: Capital Gains Tax Explained.