How Dividend Taxes Work in the USA: A Complete 2026 Guide

You buy a stock, it pays you a dividend, and you feel like you're getting free money. Then tax season arrives. Suddenly, that quarterly payment starts to feel a lot less free.

Dividend taxes catch many investors off guard — not because they're complicated, but because most people don't realize that the IRS treats two types of dividends in drastically different ways. On the exact same $50,000 in dividends, one type could cost you $0 in federal taxes. The other could cost you over $18,500. The difference comes down to a single word: qualified.

This guide explains exactly how dividend taxes work in 2026, what determines whether your dividends are qualified or ordinary, and how to keep more of what your investments earn.

What Is a Dividend?

A dividend is a payment a corporation or fund makes to its shareholders, typically out of its profits. Most dividends are paid in cash on a quarterly schedule, but some are paid as additional shares of stock or other property.

You can receive dividends from:

- Individual stocks (domestic and some foreign)

- Mutual funds and ETFs

- Real Estate Investment Trusts (REITs)

- Money market funds

- Master Limited Partnerships (MLPs)

The IRS considers dividends to be income in the year they are received — even if you automatically reinvest them. This is one of the most important facts new investors learn the hard way: a dividend reinvestment plan (DRIP) does not defer or eliminate the tax. You owe tax on reinvested dividends in the year they are paid, just as if you had received the cash.

To understand how dividends fit into your overall taxable income picture, see our guide: What Is Taxable Income.

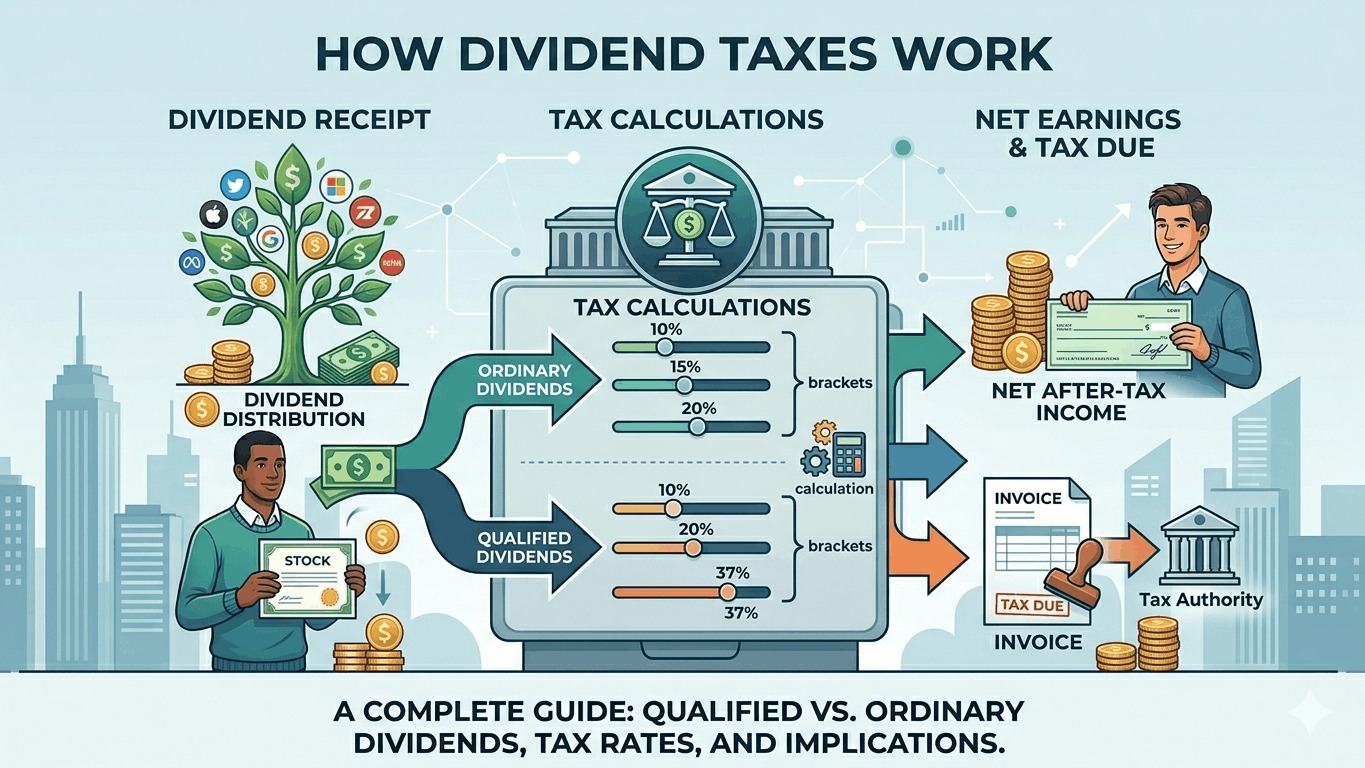

The Two Types of Dividends: Qualified vs. Ordinary

This is the most important distinction in dividend taxation. Everything else flows from it.

| Qualified Dividends | Ordinary (Non-Qualified) Dividends | |

|---|---|---|

| 2026 Federal Tax Rate | 0%, 15%, or 20% | 10% to 37% (ordinary income rates) |

| Maximum effective rate | 23.8% (including NIIT) | 40.8% (including NIIT) |

| Tax treatment | Same as long-term capital gains | Same as wages and salary |

| Who benefits most | Long-term buy-and-hold investors | Nobody — this is the less favorable treatment |

The gap is enormous. On $50,000 in dividends, a taxpayer in the 24% ordinary income bracket pays $12,000 on ordinary dividends — but only $7,500 at the 15% qualified rate. That is a $4,500 annual difference from the same investment dollar amount.

2026 Ordinary Dividend Tax Rates

Ordinary (non-qualified) dividends are taxed at the same rates as your wages and other ordinary income — your regular federal income tax brackets.

2026 Ordinary Income Tax Rates (Single Filers):

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 – $12,400 |

| 12% | $12,401 – $50,250 |

| 22% | $50,251 – $105,700 |

| 24% | $105,701 – $201,900 |

| 32% | $201,901 – $256,100 |

| 35% | $256,101 – $640,600 |

| 37% | Over $640,600 |

There is no preferential rate, no 0% option, and no 20% ceiling for ordinary dividends. They stack on top of your other income and are taxed at your full marginal rate. For a complete breakdown of how these brackets are applied layer by layer, read our guide: How Tax Brackets Work.

What Makes a Dividend "Qualified"? The Two Requirements

For a dividend to receive the lower qualified rate, it must pass both of the following tests:

Test 1 — Source Requirement

The dividend must be paid by:

- A U.S. corporation, OR

- A qualified foreign corporation whose stock is listed on a major U.S. stock exchange (e.g., NYSE, NASDAQ)

Automatically disqualified sources (always ordinary dividends):

- Real Estate Investment Trusts (REITs)

- Master Limited Partnerships (MLPs)

- Money market funds

- Employee stock option plans

- Dividends paid by tax-exempt organizations

- High-income ETFs using options strategies (e.g., JEPI, JEPQ)

Test 2 — Holding Period Requirement

You must have held the stock for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date.

What is the ex-dividend date? It is the cutoff date a company sets to determine which shareholders are eligible for the next dividend payment. If you buy before this date and meet the holding period, your dividend is qualified. If you buy just before the date and sell right after collecting the dividend, it is not.

Simplified rule for most investors: If you've owned a regular U.S. company stock for at least two months before the dividend was paid, it will almost always be qualified. Active traders who buy and sell quickly around dividend dates are most at risk of losing qualification.

The dividend payer is required to report which of your dividends are qualified on Form 1099-DIV — Box 1b shows qualified dividends, Box 1a shows total ordinary dividends. The amount in Box 1a minus Box 1b equals your non-qualified ordinary dividends.

Real-World Example: The Tax Cost of Ordinary vs. Qualified

Meet Robert and Lisa, a married couple filing jointly with $180,000 in taxable income in 2026. They receive $30,000 in dividends from their investment portfolio.

Scenario A — All Ordinary Dividends: Their income falls in the 22% bracket. Ordinary dividends are taxed at their marginal rate.

- Tax on $30,000 in dividends: $6,600 (22%)

Scenario B — All Qualified Dividends: Their taxable income of $180,000 places them in the 15% qualified dividend bracket.

- Tax on $30,000 in dividends: $4,500 (15%)

They save $2,100 per year simply by ensuring their dividends qualify — without changing the amount they invest or the stocks they choose.

For a high-income couple in the 37% bracket collecting $100,000 in dividends, the difference between ordinary and qualified treatment is $17,000 per year.

The Net Investment Income Tax (NIIT): The Hidden 3.8% Surcharge

High-income investors face an additional 3.8% Net Investment Income Tax on dividend income. This applies to:

- Single filers with Modified AGI over $200,000

- Married filing jointly with Modified AGI over $250,000

This threshold has not been adjusted for inflation since it was introduced in 2013 — meaning it pulls in more taxpayers every year as incomes rise.

The NIIT applies to the lesser of your net investment income or the amount your MAGI exceeds the threshold. It affects both qualified and ordinary dividends.

Combined maximum 2026 rates including NIIT:

- Qualified dividends: 20% + 3.8% = 23.8%

- Ordinary dividends: 37% + 3.8% = 40.8%

The $17,000 difference per $100,000 in dividends widens to over $17,000 at the highest income levels — making the qualified vs. ordinary distinction even more critical for high earners.

Special Dividend Types: How Different Investments Are Taxed

Not all dividends fit neatly into the qualified/ordinary framework. Here is how specific investment types are treated in 2026:

| Investment Type | Dividend Treatment in 2026 |

|---|---|

| U.S. stocks (held 60+ days) | Qualified — taxed at 0%, 15%, or 20% |

| U.S. stocks (held < 60 days) | Ordinary — taxed at income rates |

| REITs | Ordinary — always taxed at income rates (up to 37%) |

| MLPs (Master Limited Partnerships) | Ordinary — taxed at income rates |

| Money market funds | Ordinary — taxed at income rates |

| International ETFs | Usually qualified if listed on U.S. exchange |

| Options-based income ETFs (JEPI, JEPQ) | Ordinary — taxed at income rates |

| Mutual fund capital gain distributions | Always long-term — taxed at capital gains rates |

| Return of capital distributions | Not taxable now — reduces your cost basis |

REITs are a common trap. Many investors buy REITs specifically for their high dividend yields, not realizing every dollar of that income is taxed at ordinary rates — up to 37% federally. Holding REITs inside a tax-advantaged account (like an IRA) is the standard workaround.

5 Strategies to Reduce Dividend Taxes in 2026

1. Maximize the 0% qualified dividend rate If your taxable income is below $49,450 (single) or $98,900 (married filing jointly), your qualified dividends are completely tax-free federally. Strategies like maximizing retirement contributions, claiming the full standard deduction, and timing income carefully can keep you in this bracket. The 2026 standard deduction is $16,100 for single filers and $32,200 for married couples — use it. For more on deduction strategies, read: Standard Deduction vs Itemized Deduction.

2. Hold REIT and MLP income in a traditional IRA Since REIT and MLP distributions are always taxed as ordinary income, shielding them in a traditional IRA or 401(k) eliminates the current-year tax hit. Let that high-yield income compound tax-deferred.

3. Own qualified dividend stocks in your taxable account Qualified dividend stocks from established U.S. companies work best in a taxable brokerage account — you benefit from the lower 0%/15%/20% rate, which you'd lose inside a traditional IRA.

4. Use your Roth IRA for the highest-yield investments Dividends inside a Roth IRA are completely tax-free, including all reinvested growth. A high-yield dividend stock compounding tax-free over 20–30 years is one of the most powerful legal tax advantages available to individual investors.

5. Don't sell stocks just before the ex-dividend date If you're close to meeting the 60-day holding period requirement and the ex-dividend date is approaching, wait the extra days before selling. Losing qualified status on a large dividend can cost far more than any short-term market timing benefit.

How Dividends Interact With Your Income Tax Bracket

Dividends add to your total taxable income — and that interaction is more nuanced than most investors realize.

Qualified dividends do not push your wages into a higher bracket. They are placed "on top" of your ordinary income and taxed at their own rates. However, they do count toward your total income for purposes of determining which qualified dividend rate bracket you fall into — and whether you cross the NIIT threshold.

Understanding how all income layers — wages, dividends, capital gains, self-employment income — stack together and affect each other is covered in detail in our guide: How Income Taxes Work in the USA.

Dividends vs. Capital Gains: Key Differences

Investors often confuse dividend income with capital gains, since both are investment-related. They are fundamentally different:

| Dividends | Capital Gains | |

|---|---|---|

| What it is | Payment from a company to shareholders | Profit from selling an asset |

| When taxed | When received (including reinvested) | When the asset is sold |

| Qualified rate | Based on 60-day holding period rule | Based on 366-day holding period rule |

| Tax form | Form 1099-DIV | Schedule D / Form 8949 |

| Can be 0% federally? | Yes — for qualified dividends within income limits | Yes — for long-term gains within income limits |

Both qualified dividends and long-term capital gains share the same 0%/15%/20% rate structure in 2026. To understand how capital gains are taxed and how they interact with dividend income, read: Capital Gains Tax Explained and Short-Term vs Long-Term Capital Gains Taxes.

State Taxes on Dividends

Federal dividend taxes are only part of the picture. Most states also tax dividend income — but rules vary widely:

- No income tax states: Texas, Florida, Nevada, Washington, Alaska, Wyoming, South Dakota — no state dividend tax

- States taxing dividends as ordinary income: California (up to 13.3%), New York (up to 10.9%), New Jersey (up to 10.75%) — no preferential qualified rate at the state level

- Some states conform to federal qualified treatment: A small number of states recognize the qualified/ordinary distinction and apply lower rates accordingly

For a full breakdown of how federal and state taxes interact, see: Federal vs State Taxes Explained.

Final Thoughts

Dividend taxes are not a fixed cost — they are a variable that smart investors actively manage. The difference between qualified and ordinary treatment, the power of the 0% bracket, and the importance of account placement can together save tens of thousands of dollars over a lifetime of investing.

In 2026, with the qualified dividend 0% threshold at $98,900 for married couples and the standard deduction at $32,200, the opportunity to earn dividend income completely tax-free is within reach for more Americans than most people realize. The question is whether you build your portfolio and plan your income with that in mind.

For a complete picture of how your total income — wages, dividends, capital gains, and deductions — all come together on your return, start with our comprehensive guide: How Income Taxes Work in the USA.