If you want to pay less in taxes, the key is simple: reduce your taxable income.

Many people assume taxes are fixed, but in reality, there are several legal strategies that can significantly lower how much of your income is taxed. Whether you’re a salaried employee, business owner, or investor, small adjustments can lead to meaningful savings.

In this guide, we’ll break down practical ways to reduce your taxable income in the United States—with real examples and easy-to-understand explanations.

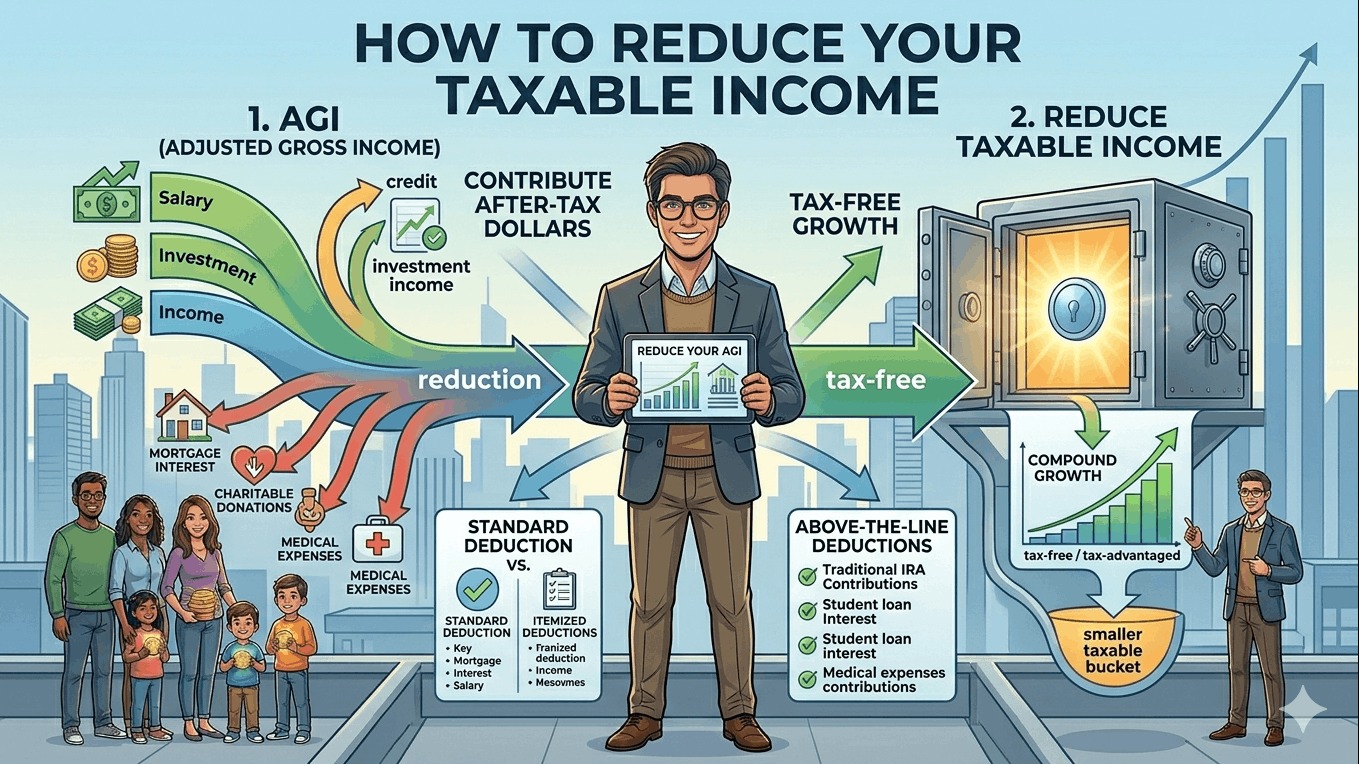

What Is Taxable Income? (Simple Explanation)

Taxable income is the portion of your earnings that the government actually taxes after deductions and adjustments.

Basic formula:

- Total income

- Minus deductions

- Minus adjustments

= Taxable income

Example:

- Salary: $100,000

- Deductions: $20,000

- Taxable income: $80,000

Learn more:

What Is Taxable Income

https://statush.com/finance-statistics/what-is-taxable-income

1. Contribute to Retirement Accounts

One of the easiest and most effective ways to reduce taxable income is through retirement contributions.

How it works:

- Contributions to traditional 401(k) or IRA are tax-deductible

- Your taxable income decreases immediately

Real-world example:

- Income: $90,000

- 401(k) contribution: $15,000

- New taxable income: $75,000

Related:

Tax Advantages of a 401(k)

https://statush.com/finance-statistics/tax-advantages-of-a-401k

Practical tip:

Always contribute at least enough to get employer matching—it’s both tax savings and free money.

2. Use Health Savings Accounts (HSA)

An HSA is one of the most tax-efficient tools available.

Benefits:

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals for medical expenses are tax-free

Example:

If you contribute $3,500 to an HSA:

- Your taxable income drops by $3,500

My take:

HSAs are often overlooked, but they offer one of the best tax advantages available.

3. Take Advantage of Tax Deductions

Deductions directly reduce your taxable income.

Common deductions:

- Mortgage interest

- Student loan interest

- Medical expenses (above limits)

- State and local taxes (SALT)

Learn more:

Standard Deduction vs Itemized Deduction

https://statush.com/finance-statistics/standard-deduction-vs-itemized-deduction

Practical tip:

If your deductions exceed the standard deduction, itemizing can save more money.

4. Claim Tax Credits (Indirect Impact)

While credits don’t reduce taxable income directly, they reduce your total tax bill—which is just as valuable.

Examples:

- Child Tax Credit

- Education credits

- Earned Income Tax Credit

Related:

Tax Credits vs Tax Deductions

https://statush.com/finance-statistics/tax-credits-vs-tax-deductions

5. Deduct Business Expenses

If you have a side hustle or business, you can deduct legitimate expenses.

Examples:

- Home office

- Equipment

- Software

- Travel expenses

Real-world example:

- Side income: $20,000

- Expenses: $5,000

- Taxable income: $15,000

Learn more:

Tax Write-Offs for Side Hustles

https://statush.com/finance-statistics/tax-write-offs-for-side-hustles

6. Use Flexible Spending Accounts (FSA)

An FSA allows you to use pre-tax money for medical or dependent care expenses.

Benefit:

- Contributions reduce taxable income

- Covers everyday healthcare costs

Example:

If you contribute $2,000 to an FSA:

- Your taxable income drops by $2,000

7. Invest in Tax-Efficient Accounts

Where you invest matters just as much as what you invest in.

Tax-efficient options:

- 401(k)

- IRA

- Roth accounts (for future tax savings)

Related:

Tax Benefits of Retirement Accounts

https://statush.com/finance-statistics/tax-benefits-of-retirement-accounts

8. Harvest Investment Losses

Tax-loss harvesting helps offset gains and reduce taxable income.

Example:

- Capital gain: $10,000

- Capital loss: $4,000

- Taxable gain: $6,000

Learn more:

Tax Strategies for Investors

https://statush.com/finance-statistics/tax-strategies-for-investors

Practical tip:

Review your portfolio before year-end to take advantage of this strategy.

9. Time Your Income and Expenses

Timing can play a big role in reducing taxes.

Strategies:

- Delay income to next year

- Accelerate deductions into current year

Example:

If you expect higher income next year, deferring income can reduce your current taxable income.

10. Contribute to Charitable Donations

Charitable giving can lower taxable income if you itemize deductions.

Example:

- Donate $5,000

- Taxable income reduces by $5,000

Practical tip:

“Bunch” donations into one year to maximize deductions.

11. Use Education-Related Tax Benefits

Education expenses can provide deductions or credits.

Examples:

- Tuition deductions

- Education tax credits

Learn more:

Education Tax Credits Explained

https://statush.com/finance-statistics/education-tax-credits-explained

12. Optimize Filing Status

Your filing status affects your tax brackets and deductions.

Options:

- Single

- Married filing jointly

- Married filing separately

- Head of household

Choosing the right status can lower taxable income and taxes owed.

Common Mistakes to Avoid

Even smart taxpayers miss opportunities:

- Not contributing to retirement accounts

- Ignoring HSAs or FSAs

- Taking standard deduction when itemizing is better

- Missing eligible credits

Avoiding these can make a noticeable difference.

Final Thoughts

Reducing your taxable income is one of the most effective ways to keep more of your money. The best part is that most strategies are simple and completely legal—you just need to use them consistently.

In my opinion, the most powerful strategies are:

- Retirement contributions

- Tax-advantaged accounts (HSA, 401(k))

- Smart use of deductions

Simple plan to follow:

- Maximize tax-advantaged contributions

- Track deductions and expenses

- Plan ahead instead of waiting until tax season

Continue Learning

- Tax Planning Strategies for High Earners

https://statush.com/finance-statistics/tax-planning-strategies-for-high-earners - Tax Optimization Strategies

https://statush.com/finance-statistics/tax-optimization-strategies - Long-Term Tax Planning Guide

https://statush.com/finance-statistics/long-term-tax-planning-guide