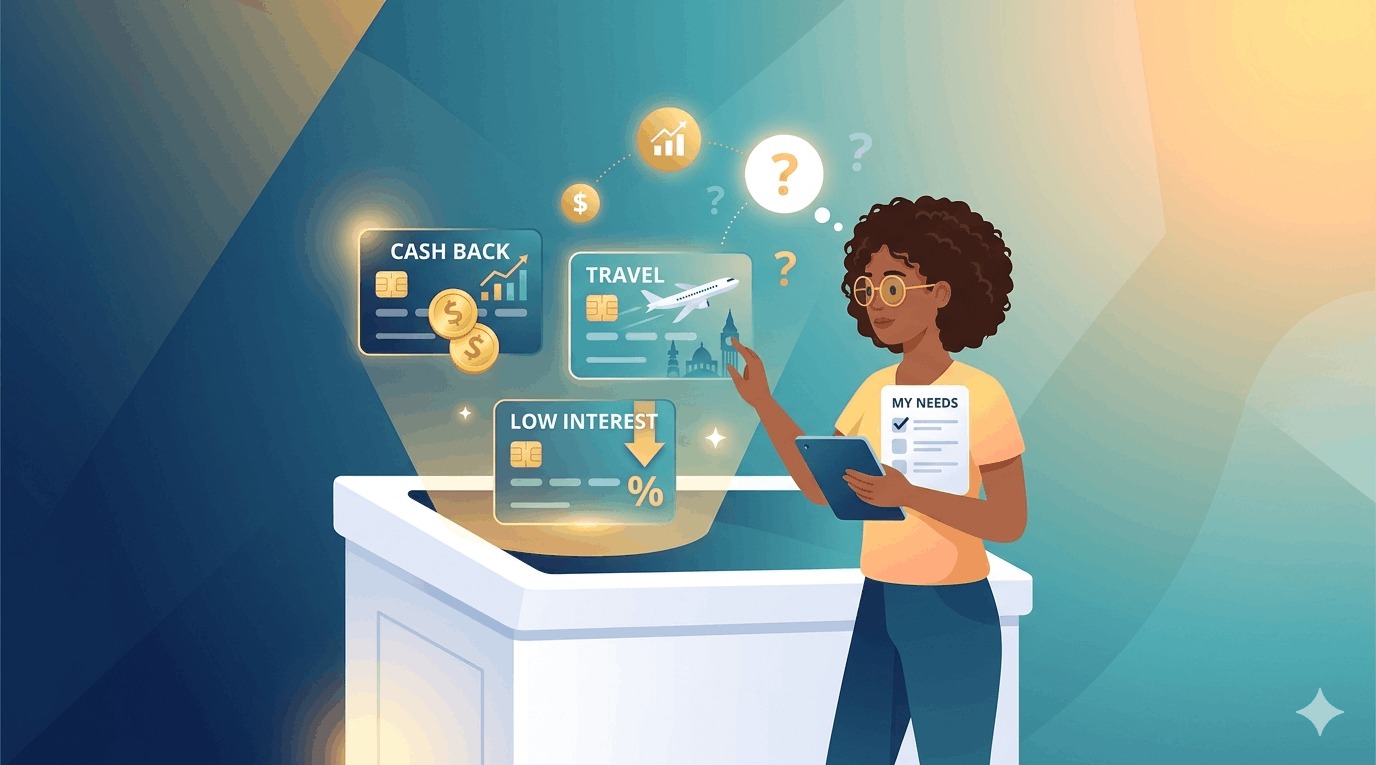

Choosing the right credit card in the United States can feel overwhelming. There are hundreds of options—cashback cards, travel cards, balance transfer offers, premium cards with annual fees—and they all promise great benefits.

But here’s the truth: the “best” credit card isn’t universal. The right card depends entirely on your lifestyle, spending habits, and financial goals.

This guide will help you cut through the noise and choose a credit card that actually works for you.

Why Choosing the Right Card Matters

A credit card isn’t just a payment method—it’s a financial tool that can either help or hurt you.

The right card can:

- Earn rewards on everyday spending

- Help build your credit score

- Save money through benefits and perks

The wrong card can:

- Lead to unnecessary fees

- Encourage overspending

- Cost you money through interest

That’s why choosing carefully at the beginning makes a big difference over time.

For a complete understanding of how cards work:

How Credit Cards Work in the USA

https://statush.com/credit-cards-banking/how-credit-cards-work-in-the-usa

Start with Your Financial Goal

Before comparing cards, you need to be clear about what you want.

Are you trying to:

- Build credit from scratch?

- Earn cashback on daily spending?

- Travel more using points or miles?

- Pay off existing credit card debt?

Each goal points to a different type of card.

For example, if you’re just starting out, a simple beginner card is better than a premium rewards card.

Guide:

Best Credit Cards for Beginners

https://statush.com/credit-cards-banking/best-credit-cards-for-beginners

Understand the Main Types of Credit Cards

To choose the right card, you need to understand the main categories available.

Cashback Credit Cards

Cashback cards are straightforward. You earn a percentage of your spending back as cash.

They are ideal for people who want simplicity and predictable rewards.

Travel Rewards Credit Cards

Travel cards offer points or miles that can be redeemed for flights, hotels, and other travel expenses.

They can provide higher value—but require more effort to maximize.

Learn more:

Best Travel Credit Cards in the USA

https://statush.com/credit-cards-banking/best-travel-credit-cards-in-the-usa

Balance Transfer Credit Cards

These cards are designed to help you pay off existing debt by offering low or 0% introductory interest rates.

They can be useful if used strategically.

More details:

Credit Card Balance Transfer Explained

https://statush.com/credit-cards-banking/credit-card-balance-transfer-explained

Credit-Building Cards

These include secured and student cards designed for people with little or no credit history.

They focus on building a strong financial foundation.

Guide:

Best Credit Cards for Building Credit

https://statush.com/credit-cards-banking/best-credit-cards-for-building-credit

Key Factors to Compare

Once you know your goal, it’s time to compare cards based on important features.

Interest Rate (APR)

APR determines how much you’ll pay if you carry a balance.

If you plan to pay your balance in full every month, APR matters less. But if you might carry a balance, a lower APR is important.

To understand this:

What Is APR on Credit Cards?

https://statush.com/credit-cards-banking/what-is-apr-on-credit-cards

Annual Fees

Some cards charge an annual fee, while others are free.

A card with a fee can still be worth it if the rewards and benefits exceed the cost. But if you’re not using the benefits, the fee becomes unnecessary.

Learn more:

What Is an Annual Fee Credit Card

https://statush.com/credit-cards-banking/what-is-an-annual-fee-credit-card

Rewards Structure

Different cards offer different reward systems:

- Flat-rate cashback

- Category-based rewards

- Travel points or miles

Choose a card that matches your spending habits.

For example, if you spend a lot on groceries, look for a card that rewards grocery purchases.

Fees Beyond Annual Fee

Credit cards may include additional costs such as:

- Late payment fees

- Foreign transaction fees

- Balance transfer fees

Understanding these can help you avoid unnecessary charges.

More details:

Credit Card Fees Explained

https://statush.com/credit-cards-banking/credit-card-fees-explained

Simple Comparison Table

| Factor | Why It Matters |

|---|---|

| APR | Cost of carrying a balance |

| Annual Fee | Yearly cost of the card |

| Rewards | Value you earn from spending |

| Fees | Extra costs to watch out for |

Real-World Example

Let’s compare two people choosing different cards.

Scenario 1: Simple Cashback User

Riya chooses a no-fee cashback card with 2% rewards. She uses it for groceries and bills and earns around $300 per year.

Scenario 2: Travel Enthusiast

Karan chooses a travel rewards card with a $95 annual fee. He travels frequently and uses points for flights, gaining $700+ in value annually.

Both made the right choice—because they chose cards that fit their lifestyle.

Match the Card to Your Spending Habits

One of the most common mistakes is choosing a card based on marketing instead of actual usage.

If you rarely travel, a travel card may not provide much value.

If you prefer simplicity, a complex rewards system may feel frustrating.

The best card is the one that fits naturally into your daily life.

Don’t Ignore Your Credit Score

Your credit score plays a big role in which cards you can qualify for.

- No credit → Secured or beginner cards

- Fair credit → Basic unsecured cards

- Good to excellent credit → Premium rewards cards

Applying for cards beyond your eligibility can lead to rejection and unnecessary credit inquiries.

Avoid Common Mistakes

Choosing a credit card can go wrong if you’re not careful.

One common mistake is focusing only on rewards while ignoring fees and interest.

Another mistake is applying for multiple cards at once, which can hurt your credit score.

Overspending to earn rewards is another trap that can lead to debt.

To stay safe:

How to Avoid Credit Card Debt

https://statush.com/credit-cards-banking/how-to-avoid-credit-card-debt

Think Long-Term

Your first credit card doesn’t have to be perfect. It just needs to be a good starting point.

As your credit improves, you’ll have access to better cards with higher rewards and more benefits.

The key is to start with a card you can manage responsibly and build from there.

A Simple Decision Framework

If you’re unsure, use this simple approach:

- Want simplicity → Choose cashback

- Want travel rewards → Choose travel card

- Want to build credit → Choose secured/student card

- Want to reduce debt → Choose balance transfer card

This makes the decision much easier.

Final Thoughts

Choosing the right credit card isn’t about finding the most popular or highest-paying option—it’s about finding the one that fits your needs.

Focus on your goals, understand the key features, and avoid unnecessary complexity.

When used correctly, the right credit card can help you earn rewards, build credit, and manage your finances more effectively.

And once you make the right choice, the next step is simple—use it wisely.