In the 2026 U.S. housing market, home equity has become the primary driver of household wealth. As of March 2026, American homeowners hold over $30 trillion in total equity, with roughly $11 trillion of that considered "tappable."

Understanding how to calculate, build, and use this equity is essential for anyone looking to leverage their home as a financial asset rather than just a place to live.

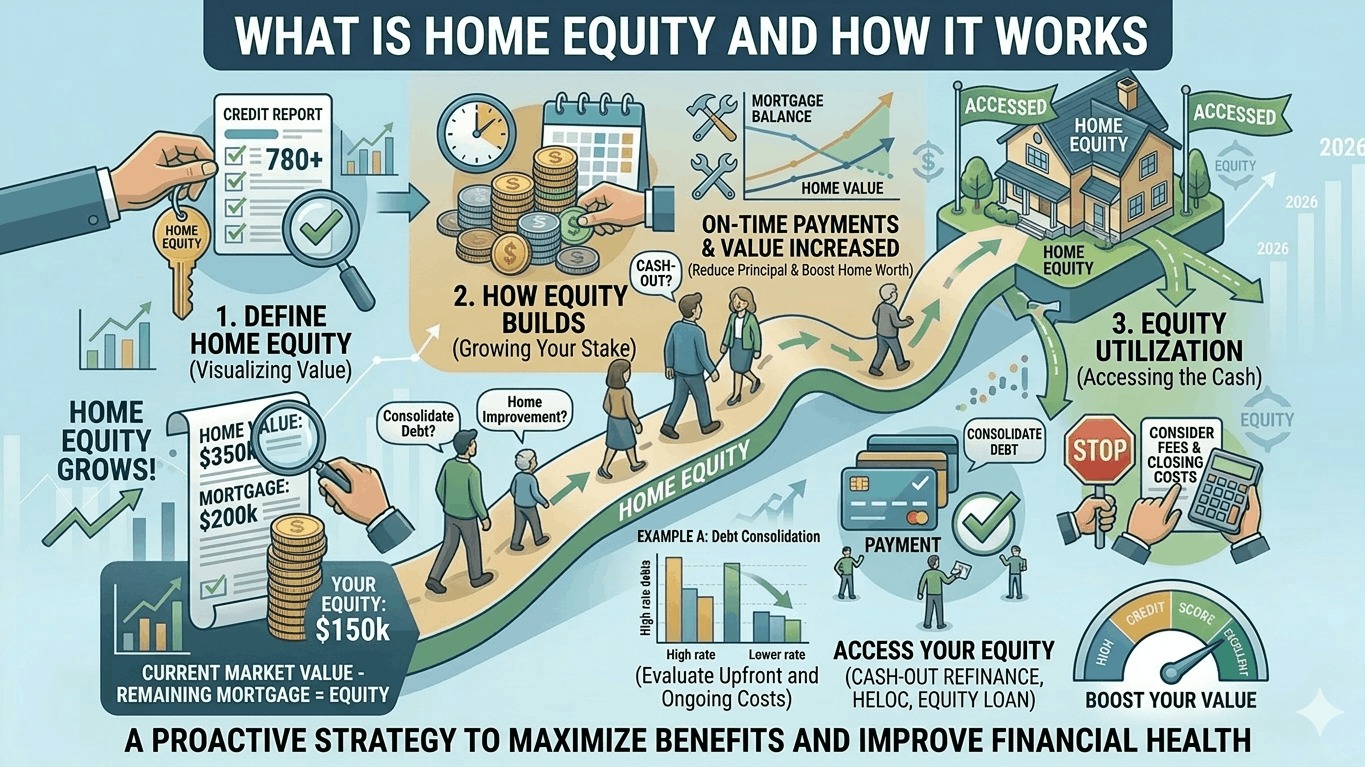

1. What Exactly Is Home Equity?

Home equity is the portion of your property that you truly "own." It is the difference between the current fair market value of your home and the outstanding balance of all loans secured by the property (including your primary mortgage and any second mortgages).

The 2026 Equity Formula:

Home Equity = Current Market Value - Total Loan Balances

Example: If your home would sell for $450,000 today and you owe $280,000 on your mortgage, you have $170,000 in home equity.

2. How Home Equity Grows in 2026

In the current market, equity typically grows through three main channels:

- Principal Reduction: Every month you make a mortgage payment, a portion goes toward the principal balance. In 2026, with average rates around 6.1%, the "forced savings" of paying down your loan remains a steady way to build ownership.

- Market Appreciation: Even with the "stalled" 0% to 2% national price growth projected for 2026, most homes still gain value over the long term. If the market value of your home rises, your equity increases dollar-for-dollar.

- Strategic Improvements: Adding value through renovations (like energy-efficient upgrades or ADUs, which are popular in 2026) can boost your home’s value faster than the general market.

3. How to "Tap" Your Equity (The 3 Main Methods)

Lenders in 2026 generally allow you to borrow up to 80% to 85% of your home's value (this is your Combined Loan-to-Value or CLTV).

| Method | How It Works | Best For... |

|---|---|---|

| Home Equity Loan | A "second mortgage" with a fixed interest rate and a lump-sum payout. | One-time, large expenses like a roof or debt consolidation. |

| HELOC | A revolving line of credit (like a credit card) with a variable interest rate. | Ongoing projects or emergency funds where you only pay for what you use. |

| Cash-Out Refi | Replaces your current mortgage with a new, larger one, giving you the difference in cash. | When current market rates (approx. 6.11%) are lower than your original rate. |

4. The Risks of Using Your Equity

While home equity is a powerful tool, it is not “free money.”

- Collateral Risk: Your home is the collateral. If you cannot make the payments on a home equity loan or HELOC, the lender can initiate foreclosure.

- Market Volatility: If home prices drop (as seen in some Sunbelt markets in early 2026), you could end up "underwater"—owing more than the home is worth—especially if you borrowed at the maximum 85% limit.

- Interest Costs: Second mortgages typically carry higher interest rates than primary mortgages. As of March 2026, average HELOC rates are hovering around 7.18%