Navigating the mortgage market in 2026 requires a mix of traditional financial discipline and an understanding of new "trended data" scoring models. Whether you are a first-time buyer or a seasoned investor, qualifying for a home loan is no longer just about a single credit score—it's about your entire financial story.

1. The Core Qualification Pillars

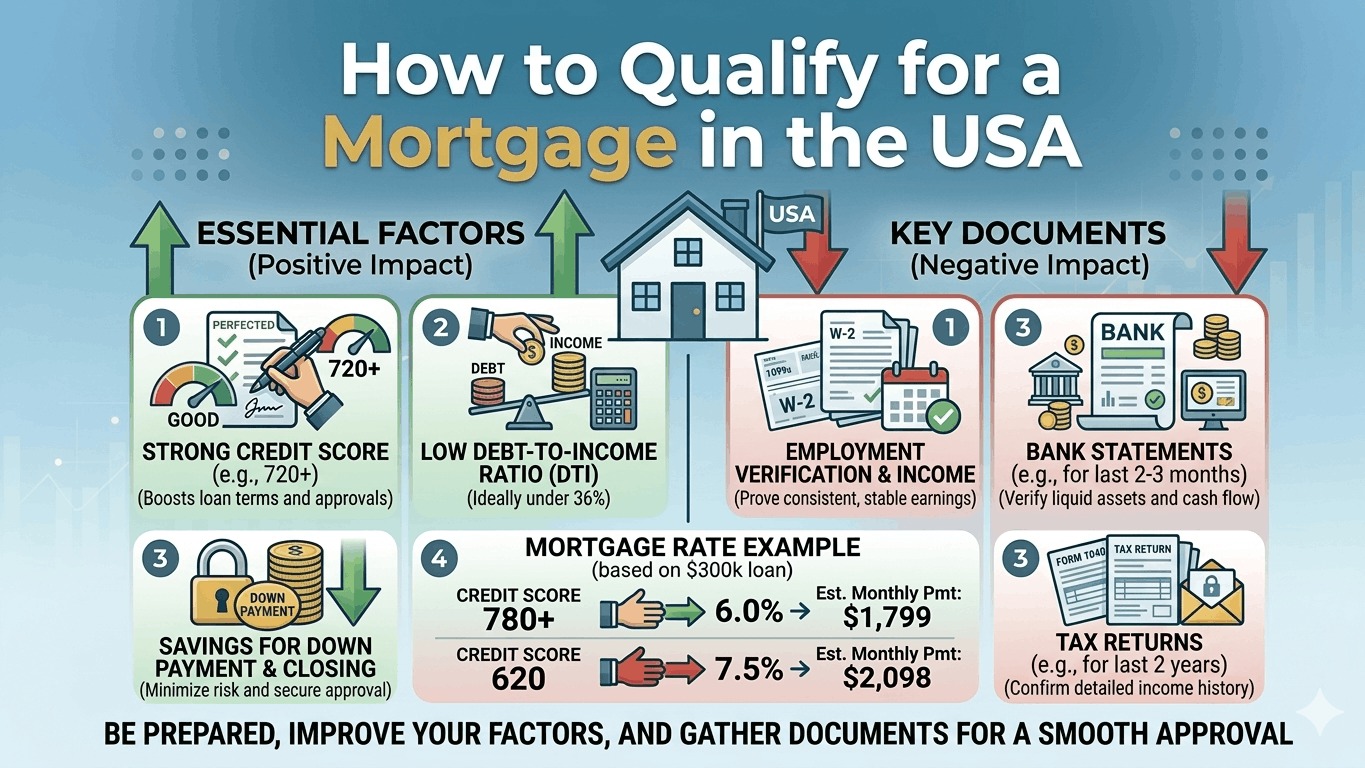

Lenders in 2026 evaluate your application based on four primary "pillars." If one is weak, you may need to over-perform in another to compensate.

A. Credit Score & History

While FICO 10T is the new standard, the minimum thresholds for 2026 remain relatively consistent across loan types:

- Conventional: 620 minimum (760+ for best rates).

- FHA: 580 for a 3.5% down payment; 500–579 for a 10% down payment.

- VA & USDA: Generally 580–640, though VA loans are more flexible for veterans.

B. Debt-to-Income Ratio (DTI)

Your DTI is the percentage of your gross monthly income that goes toward debt payments (including your future mortgage).

- Ideal: 36% or lower.

- Maximum: Most 2026 lenders cap DTI at 43%, though some FHA and VA loans allow up to 50% with "compensating factors" like high cash reserves.

C. Down Payment

The "20% down" rule is a myth in 2026. The median down payment for first-time buyers is currently around 10%.

- 3% – 5%: Common for Conventional and FHA loans.

- 0%: Available for qualified veterans (VA) and rural buyers (USDA).

D. Employment & Income Stability

Lenders typically require two years of consistent income in the same field. If you are self-employed, you will need two years of tax returns showing stable or increasing net income.

2. 2026 Mortgage Comparison Table

| Loan Type | Best For | Min. Down Payment | Min. Credit Score |

|---|---|---|---|

| Conventional | High credit scores | 3% | 620 |

| FHA | Lower credit/savings | 3.5% | 580 |

| VA | Veterans/Service Members | 0% | 580–620 |

| USDA | Rural/Suburban buyers | 0% | 640 |

| Jumbo | Luxury homes (>$832,750) | 10% – 20% | 700+ |

3. The 5-Step Qualification Process

- Check Your "Mortgage Ready" Score: Pull your reports from all three bureaus. In 2026, lenders use the middle score of the three.

- Get Pre-Approved: This is a "hard" look at your finances. A pre-approval letter in 2026 is usually valid for 60–90 days and is essential before touring homes.

- Find Your Home & Negotiate: Once your offer is accepted, the official "underwriting" begins.

- The Appraisal & Inspection: The lender will hire an appraiser to ensure the home is worth the loan amount. If the appraisal comes in low, you may need to bridge the gap in cash.

- Final Underwriting & Closing: The "Clear to Close" is the final hurdle. You’ll sign documents, pay closing costs (usually 2%–5% of the loan), and get your keys.