In the 2026 U.S. housing market, choosing between an FHA loan (government-backed) and a Conventional loan (private-backed) is the most critical financial decision a homebuyer will make.

While FHA loans have historically been the "go-to" for first-time buyers, new 2026 updates to FICO 10T scoring and shifting mortgage insurance premiums have narrowed the gap. Your choice now depends less on a single credit score and more on your long-term "trended" financial health.

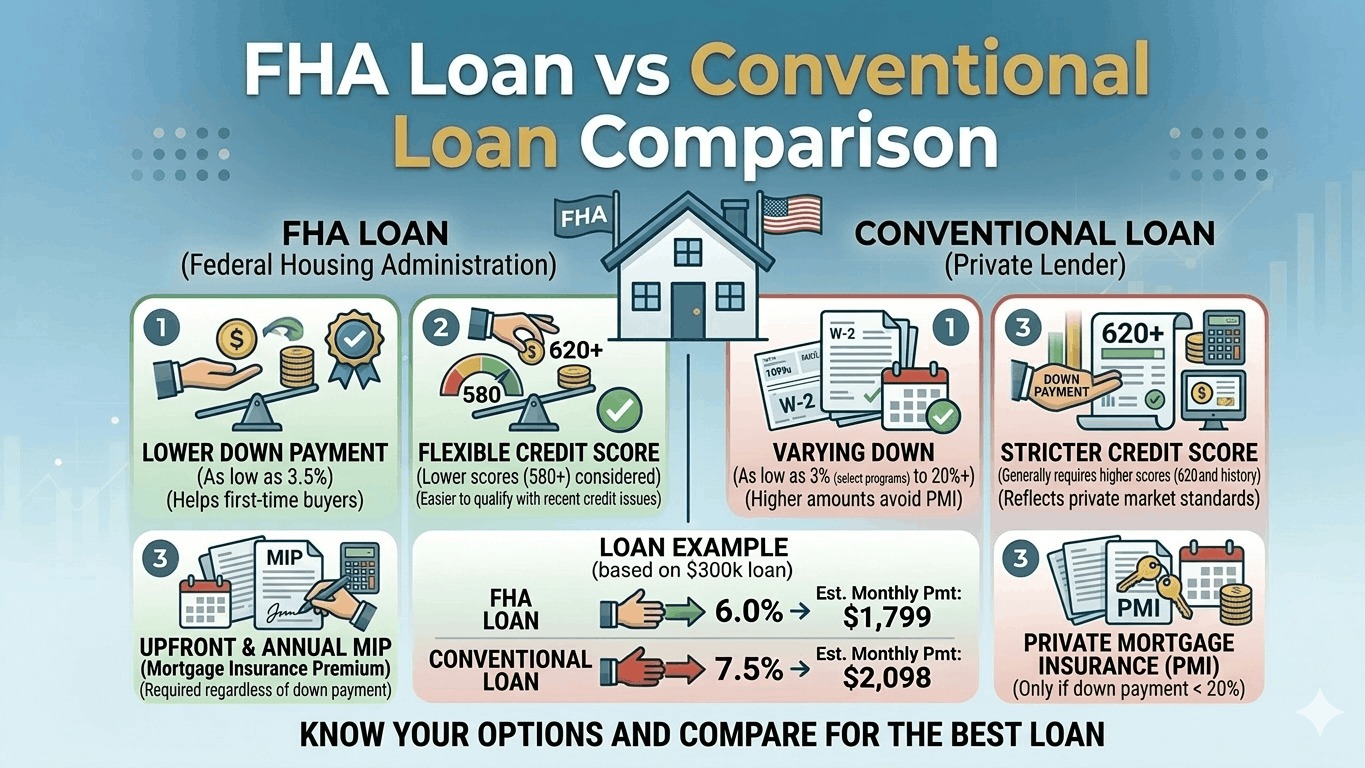

1. At-a-Glance Comparison (2026)

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Credit Score | 500 (10% down) or 580 (3.5% down) | 620 (Baseline) |

| Minimum Down Payment | 3.5% | 3% (for qualified first-time buyers) |

| Mortgage Insurance | MIP: Upfront (1.75%) + Monthly | PMI: Monthly only |

| Insurance Removal | Lifetime (usually) | Removable at 20% equity |

| Max DTI Ratio | Up to 50% (Flexible) | Usually 43% – 45% (Stricter) |

| Property Type | Primary Residence only | Primary, Second Home, or Investment |

2. Key Differences in 2026

The "Mortgage Insurance" Trap

This is often the deciding factor.

- FHA (MIP): You pay an upfront fee of 1.75% (can be rolled into the loan) and a monthly premium. If you put down less than 10%, you pay this for the entire life of the loan.

- Conventional (PMI): You only pay monthly insurance if your down payment is under 20%. Critically, PMI automatically cancels once you reach 22% equity, potentially saving you hundreds of dollars a month later on.

Loan Limits for 2026

Every year, the government adjusts how much you can borrow.

- Conventional Floor: $832,750 for single-family homes in most of the USA.

- FHA Floor: $541,287 in low-cost areas, reaching up to $1,249,125 in high-cost counties.

- Note: If the home you want is $600k in a low-cost area, you may be forced into a Conventional loan because it exceeds the FHA limit.

Appraisal Strictness

- FHA Appraisals: These are "health and safety" inspections. If the house has peeling paint, missing handrails, or an old roof, the FHA will require repairs before closing.

- Conventional Appraisals: These focus primarily on value. They are generally faster and less "nitpicky" about minor cosmetic or maintenance issues.

3. Which One Should You Choose?

Choose FHA if...

- Your credit score is between 500 and 620.

- You have a high debt-to-income ratio (e.g., high student loans).

- You are receiving a gift for 100% of your down payment (FHA is very flexible with gift funds).

- You don't mind refinancing later to drop the mortgage insurance.

Choose Conventional if...

- Your credit score is 720 or higher (to get the best PMI rates).

- You can afford a 3% to 5% down payment but want to remove insurance eventually.

- You are buying a second home or an investment property.

- You are in a competitive "bidding war" (sellers often prefer conventional offers because the appraisal process is smoother).