For U.S. Veterans, Active Duty Service Members, and eligible surviving spouses, the VA Home Loan remains the most powerful mortgage tool in the 2026 market. Backed by the Department of Veterans Affairs, these loans are designed to provide significant financial advantages that conventional or FHA loans simply cannot match.

1. The "Big Three" Benefits in 2026

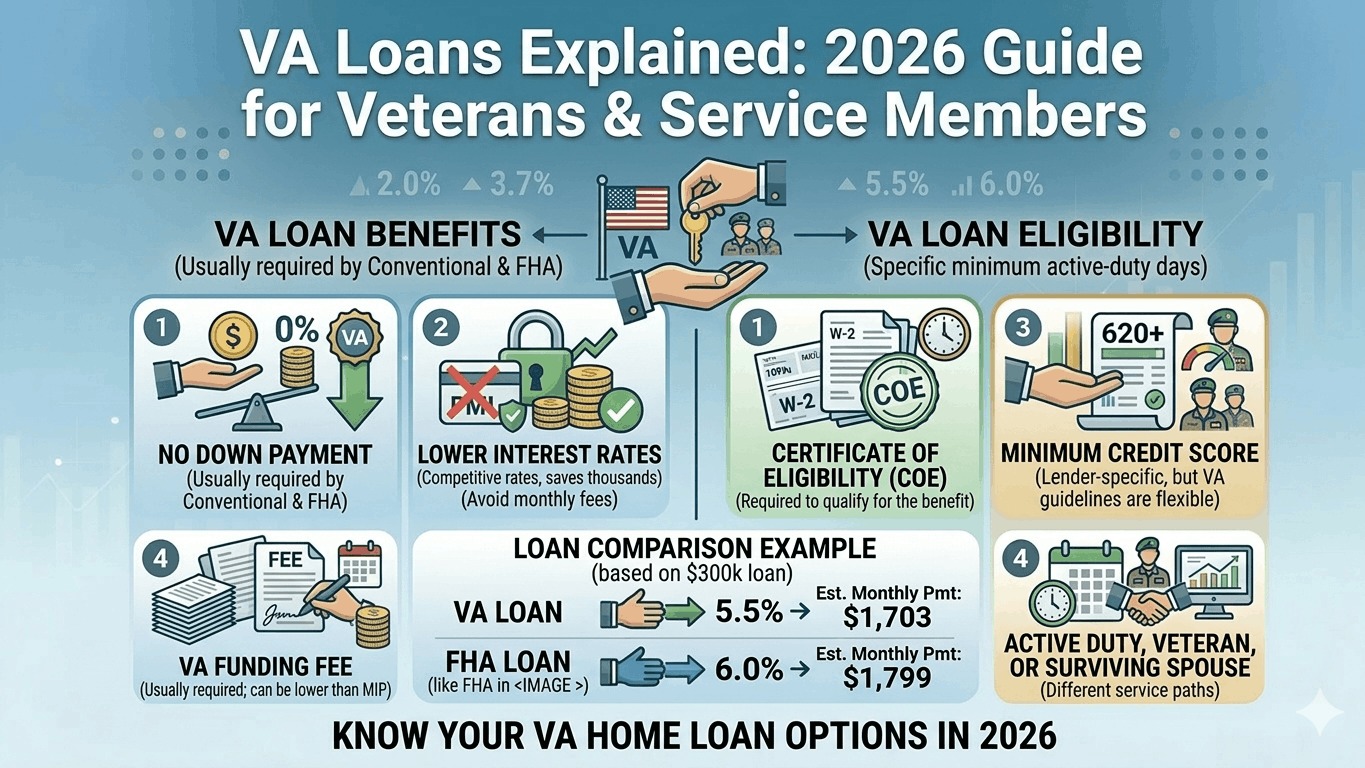

In a high-cost housing market, the VA loan provides three "deal-breakers" that save Veterans thousands of dollars both upfront and monthly:

- $0 Down Payment: You can finance 100% of the home’s purchase price. In 2026, where a 10% down payment on a median home can exceed $45,000, this benefit allows Veterans to enter the market without years of aggressive saving.

- No Monthly Mortgage Insurance (PMI): Unlike Conventional loans (which require PMI with less than 20% down) or FHA loans (which have lifetime MIP), VA loans have zero monthly mortgage insurance. This typically saves borrowers $200–$400 per month.

- Competitive Interest Rates: Because the VA guarantees 25% of the loan to the lender, VA interest rates are often 0.50% to 1.0% lower than conventional rates.

2. 2026 Loan Limits & Entitlement

A common myth is that there is a "cap" on how much you can borrow.

- Full Entitlement: If you have never used your VA loan (or have paid one off and sold the home), there is no maximum loan limit. You can borrow as much as a lender will approve based on your income with $0 down.

- Partial Entitlement: If you currently have an active VA loan and want to buy a second home using your remaining benefit, your $0-down limit is tied to the 2026 Conforming Loan Limit.

- National Baseline: $832,750

- High-Cost Areas: Up to $1,249,125 (e.g., Los Angeles, DC, NYC)

- Special Statutory Areas: Up to $1,873,675 (Alaska, Hawaii, Guam)

3. The 2026 VA Funding Fee

Instead of monthly insurance, the VA charges a one-time "Funding Fee" to keep the program running. Most borrowers roll this fee into their total loan amount.

| Usage Category | Down Payment | First-Time Use Fee | Subsequent Use Fee |

|---|---|---|---|

| Purchase / Construction | $0 Down | 2.15% | 3.30% |

| Purchase / Construction | 5% Down | 1.50% | 1.50% |

| Purchase / Construction | 10% Down | 1.25% | 1.25% |

Pro Tip: Veterans with a service-connected disability rating of 10% or higher are typically exempt from paying the Funding Fee entirely.

4. Minimum Property Requirements (MPRs)

The VA appraisal is famous for being strict, but it’s designed to protect you from buying a "money pit." The home must meet MPRs (Minimum Property Requirements):

- Heating: Must be able to maintain a temperature of 50°F in areas with plumbing.

- Roof: Must have "reasonable future utility" (usually 3–5 years of life remaining).

- Safety: No peeling lead-based paint (if built before 1978), no active termite infestations, and working electrical/plumbing systems.