In the fast-moving 2026 real estate market, a mortgage pre-approval is no longer a "nice-to-have"—it is your ticket to entry. Sellers often won't even grant a home tour without one, and in a multiple-offer situation, a pre-approved buyer will almost always beat a buyer who is “just looking.”

Unlike a quick "pre-qualification," a pre-approval is a rigorous financial audit that proves to a seller you have the backing of a lender to close the deal.

1. Pre-Approval vs. Pre-Qualification: The 2026 Difference

Many buyers use these terms interchangeably, but in 2026, lenders and AI-driven underwriting models distinguish them sharply:

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| Verification | Self-reported data (no proof needed). | Documents verified (W-2s, tax returns, etc.). |

| Credit Check | Usually a "Soft Pull" (no score impact). | Hard Pull (comprehensive credit review). |

| Strength | Very low; used for personal budgeting. | High; required for making serious offers. |

| Timeline | Instant to 24 hours. | 24 to 72 hours (Standard). |

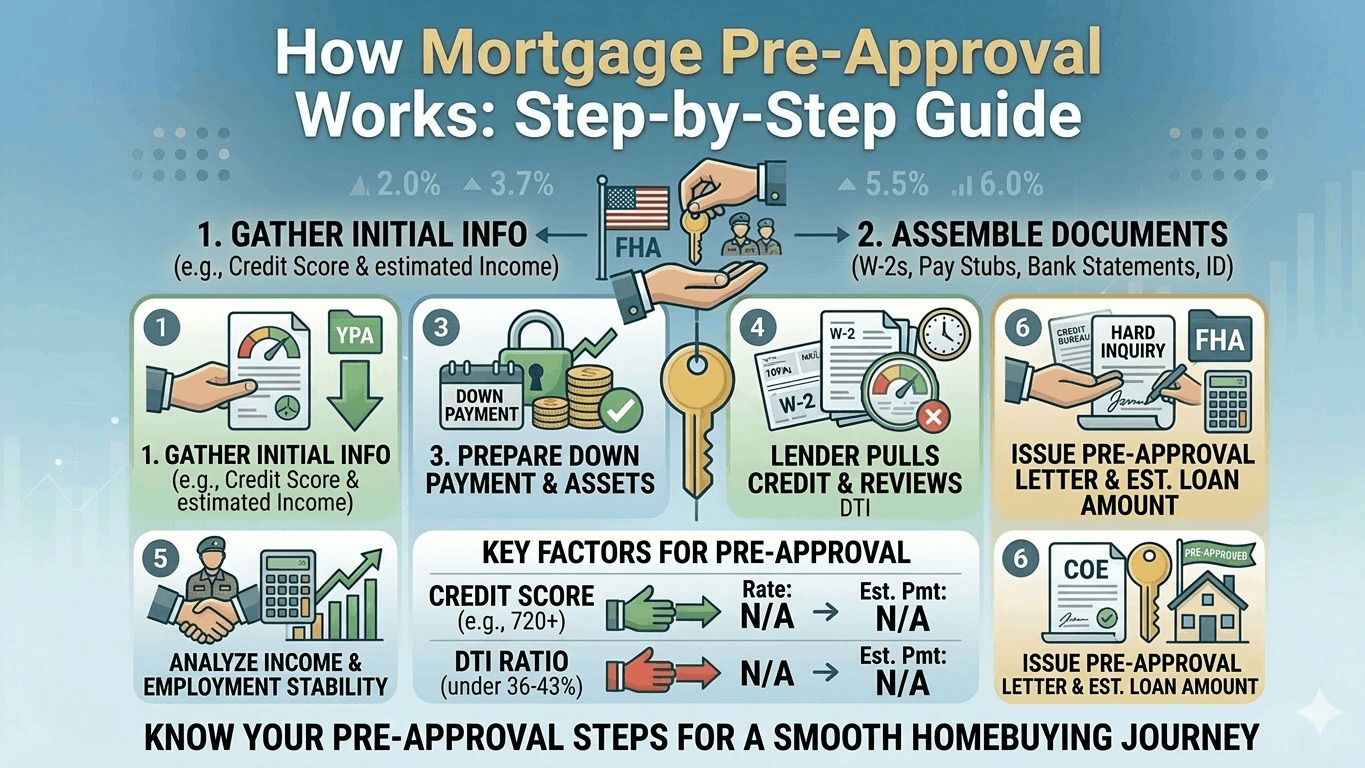

2. The 4-Step Pre-Approval Process

Step 1: The Initial Application (1003 Form)

You’ll complete a Uniform Residential Loan Application (often called a "1003"). This covers your personal identity, employment history for the last two years, and an itemized list of your assets (savings) and liabilities (debts).

Step 2: Documentation & The "Digital Vault"

In 2026, most lenders use secure portals to verify your data. You will typically need:

- Income: Last 30 days of pay stubs and last 2 years of W-2s.

- Assets: Last 60 days of bank statements (every page, even blank ones).

- Tax Returns: Last 2 years of federal filings (especially if self-employed).

- Identity: Government-issued ID and Social Security number.

Step 3: Credit Analysis & Underwriting

The lender performs a tri-merge credit report, pulling from Experian, Equifax, and TransUnion. They are looking for your Middle Score. They also calculate your Debt-to-Income (DTI) ratio—most 2026 lenders prefer this to be under 43%, though some programs allow more.

Step 4: The Pre-Approval Letter

If you pass the audit, you receive an official letter. This document will state:

- The specific loan amount you are approved for.

- The loan program (Conventional, FHA, VA, etc.).

- The estimated interest rate (though not locked yet).

- The expiration date (typically 60 to 90 days).

3. Why Pre-Approvals Expire

A pre-approval letter is a "snapshot" in time. In 2026, lenders set an expiration (usually 90 days) because:

- Interest Rates Fluctuate: A rate hike can lower your maximum buying power.

- Financial Changes: If you change jobs or take out a new car loan, your DTI changes.

Credit Refresh: Credit reports "expire" in the eyes of an underwriter after 90–120 days.

Tip: If your letter expires, you don't usually have to start over. A simple "refresh" of your most recent pay stub and bank statement is often enough to extend it.

4. The "Golden Rules" After Pre-Approval

Once you have your letter, your financial life must enter "Stasis" until you close on the house. To avoid losing your approval:

- DO NOT quit or change your job.

- DO NOT make large, unexplained cash deposits into your bank accounts.

- DO NOT finance new purchases (cars, furniture, appliances).

- DO NOT co-sign for anyone else’s loan.