In 2026, the mortgage landscape has shifted. With the widespread adoption of FICO 10T, lenders are no longer just looking at a "snapshot" of your score—they are looking at your trended data over the last 24 months. This means that "quick fixes" right before applying are less effective than they used to be.

To secure the best 2026 interest rates, you generally need a score of 760 or higher. Improving your score from a 680 to a 760 can save you over $50,000 in interest over the life of a typical 30-year loan.

1. The 2026 "Trended Data" Strategy

Unlike older models, FICO 10T rewards borrowers who show a consistent pattern of paying down debt rather than just keeping it steady.

- The "Spend-Down" Trend: If your credit card balances have been decreasing month-over-month for the last year, you may receive a higher score than someone with the same total debt who only makes minimum payments.

- Avoid the "Last-Minute" Scrub: In the past, you could pay off a card the day before applying to "boost" your score. In 2026, lenders see that your historical trend was high usage, which may temper the score increase. Start your aggressive pay-down at least 6 months before applying.

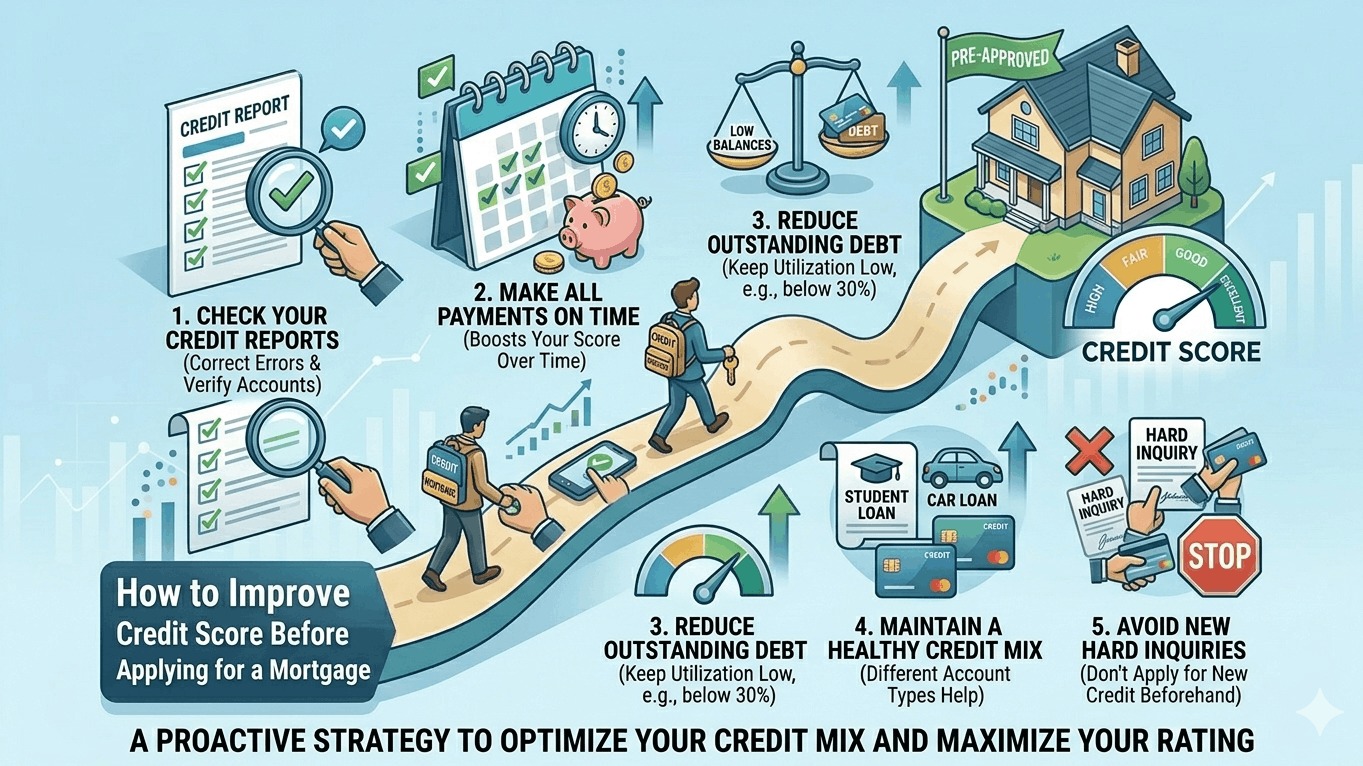

2. Master Your Utilization (The 10% Rule)

While the old advice was to stay under 30% utilization, the 2026 "Superprime" borrowers stay under 10%.

- Micro-Payments: To keep your reported balance low, pay your credit card bill twice a month: once mid-cycle and once right before the statement closing date. This ensures the "snapshot" sent to the bureaus shows a near-zero balance.

- Request Limit Increases: Call your card issuers and ask for a higher limit without a "hard pull." This instantly lowers your utilization ratio without you paying an extra cent in debt.

3. The "New Credit" Freeze

In 2026, "new credit" accounts for 10% of your score, but for mortgage lenders, it’s a major red flag for Debt-to-Income (DTI) stability.

- The 12-Month Rule: Avoid opening any new credit cards, auto loans, or "Buy Now, Pay Later" (BNPL) accounts for at least 12 months before your mortgage application.

- The Inquiry Hit: Every "hard inquiry" can drop your score by 2–5 points. While one inquiry is minor, three or more in a year can signal financial distress to 2026 AI-underwriting models.

4. Dispute Inaccuracies (The 2026 Way)

Under the Fair Credit Reporting Act, you are entitled to accurate data. In 2026, automated dispute tools make this faster, but human-led manual reviews are still the most effective for mortgages.

- Check All Three: Pull your reports from Equifax, Experian, and TransUnion via AnnualCreditReport.com.

- Focus on "Disputed" Status: If you are currently disputing a charge, many lenders cannot finish your mortgage application until that dispute is resolved. Clear all disputes at least 60 days before applying for your loan.