In the financial markets of 2026, risk tolerance is often described as the "sleep-at-night" factor. It is the degree of variability in investment returns that you are willing and able to withstand. While every investor wants high returns, not everyone is prepared for the "rollercoaster" ride required to get there.

Understanding your risk tolerance is the difference between staying the course during a market dip and panicking to sell at the worst possible time.

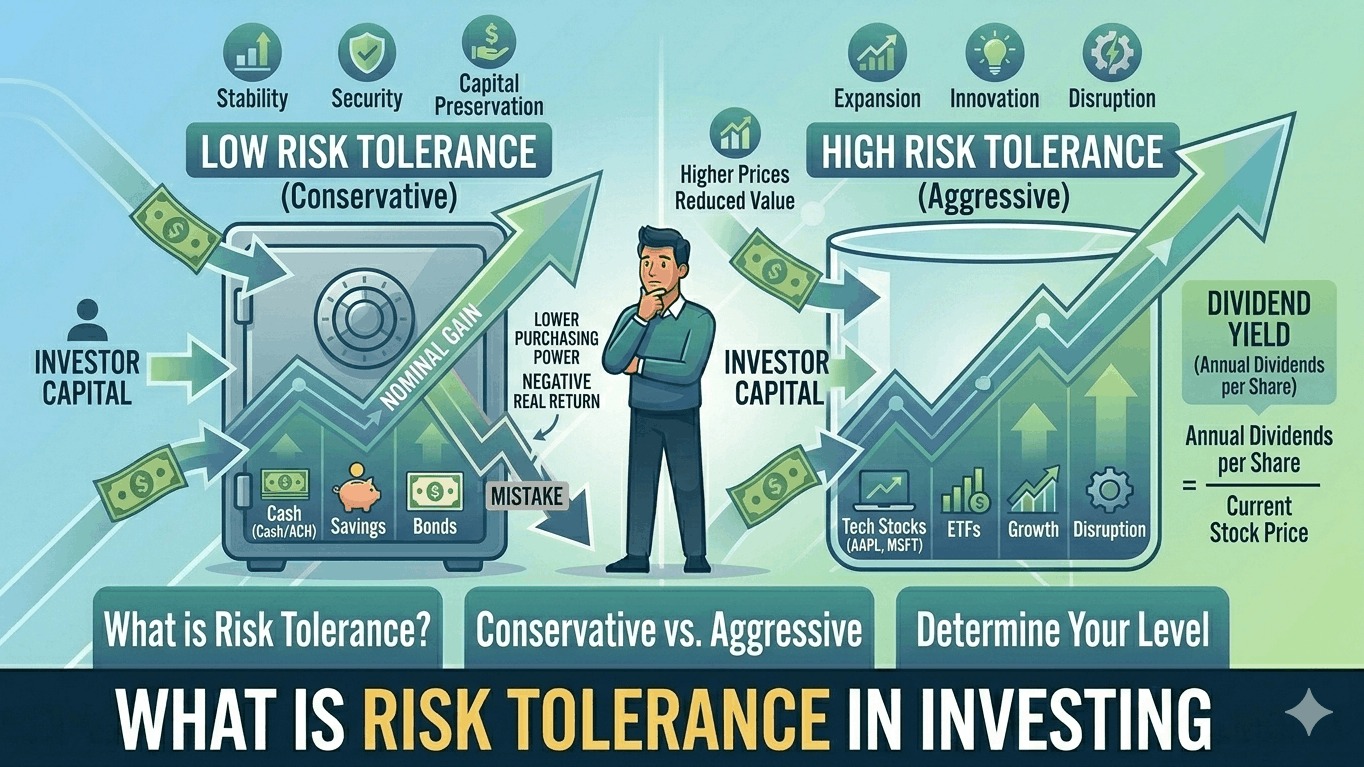

1. The Two Pillars of Risk: Willingness vs. Capacity

Risk tolerance is not just a single feeling; it is a calculation based on two distinct factors that often conflict with one another.

A. Risk Willingness (Psychological)

This is your emotional reaction to seeing your account balance drop.

- The Test: If the S&P 500 dropped 20% tomorrow, would you:

- Sell everything to "save" what’s left?

- Do nothing and wait for a recovery?

- Buy more because stocks are "on sale"?

- Your answer reveals your psychological temperament. Some people are naturally adventurous, while others prioritize security above all else.

B. Risk Capacity (Financial)

This is your objective ability to lose money without it ruining your life. It is dictated by your financial “math.”

- Factors: Your age, income stability, emergency fund size, and time horizon.

- Example: A 25-year-old software engineer with a $50,000 emergency fund has high risk capacity because they have 40 years to recover from a market crash. A 64-year-old planning to retire in six months has low risk capacity, regardless of how "brave" they feel emotionally.

2. Real-World Examples of Risk Profiles

The "Conservative" Investor (Low Tolerance)

- Goal: Capital Preservation.

- Strategy: They prefer the certainty of bonds, CDs, and high-yield savings accounts. They are okay with smaller gains as long as their initial "nest egg" stays safe.

- 2026 Example: A retiree who needs their portfolio to generate a steady monthly check. A 10% drop in their account would directly impact their ability to pay rent.

The "Moderate" Investor (Medium Tolerance)

- Goal: Balanced Growth.

- Strategy: A "60/40" split (60% stocks, 40% bonds). They want to participate in the stock market's growth but want a "buffer" to soften the blow when things get volatile.

- 2026 Example: A mid-career professional in their 40s. They want their money to grow for another 20 years but don't want to see half their net worth disappear in a single bad month.

The "Aggressive" Investor (High Tolerance)

- Goal: Maximum Appreciation.

- Strategy: 90% to 100% in equities (stocks), including emerging markets or individual tech sectors.

- 2026 Example: A young investor who understands that while the market might drop 30% this year, the historical trend over 30 years is overwhelmingly positive. They view market crashes as "buying opportunities."

3. Factors That Shift Your Tolerance

Your risk profile is not permanent. It evolves as your life changes:

- Time Horizon: The longer you have until you need the money, the more risk you can typically afford.

- Knowledge: As you learn more about how markets work, your "fear of the unknown" decreases, often raising your willingness to take risks.

- Life Events: Getting married, having a child, or losing a job can instantly lower your risk capacity, forcing a more conservative strategy.

4. Why Getting It Right Matters

In 2026, we see two common mistakes:

- The Cautious Trap: Investing so conservatively that your money grows slower than inflation, meaning you actually lose purchasing power over time.

- The Overconfident Trap: Thinking you are "aggressive" during a bull market, only to find out you have low tolerance when the first real crash happens, leading to a "panic sell" that locks in your losses.