In the financial world of 2026, the relationship between interest rates and the stock market remains one of the most closely watched dynamics by investors. While they don't always move in perfect opposition, interest rates act like gravity on stock valuations: when rates rise, they pull valuations down; when they fall, the market feels "lighter" and tends to climb.

As of March 2026, with the Federal Reserve maintaining the federal funds rate at 3.50% to 3.75%, understanding this tug-of-war is essential for navigating today’s volatile landscape.

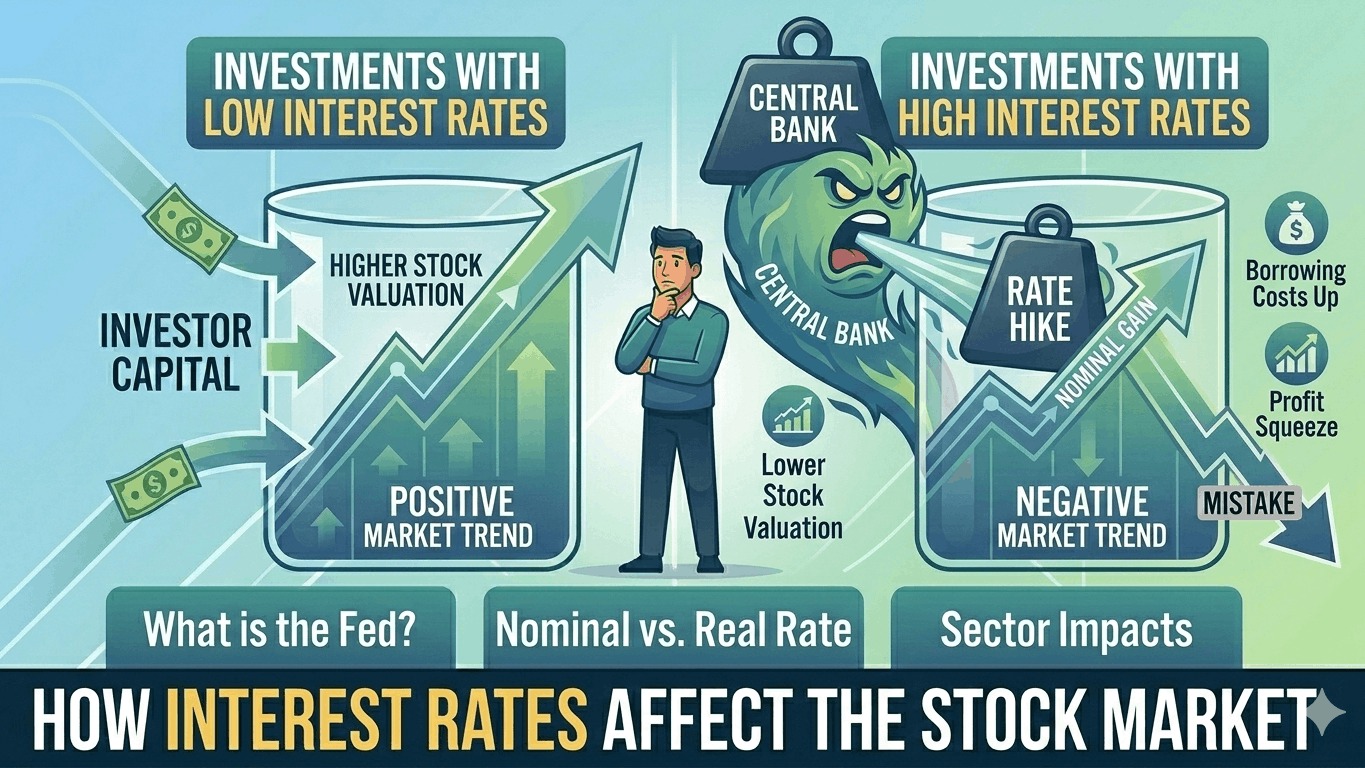

1. The Core Mechanism: Why It Happens

Interest rates represent the cost of borrowing money. When the central bank (the Fed) changes these rates, it triggers a ripple effect through the entire economy via three main channels:

A. The Discount Rate (Valuation Math)

Analysts value stocks using a Discounted Cash Flow (DCF) model. This formula calculates what a company’s future earnings are worth in “today’s dollars.”

- When rates rise: The "discount rate" in the formula goes up, which mathematically makes those future earnings worth less today.

- Impact: This hit is hardest on Growth Stocks (like AI and Tech) because their biggest profits are expected far in the future.

B. Corporate Profitability

Most companies carry debt to fund their operations.

- Higher Rates: Interest expenses go up, which directly eats into net profit margins.

- Lower Rates: Refinancing debt becomes cheaper, freeing up cash for dividends, buybacks, or expansion.

C. The "Competition" for Capital

Investors always seek the best risk-adjusted return.

- When interest rates are at 1%, a 5% return in the stock market looks amazing.

- When "safe" Government Bonds or Savings Accounts offer 4.5% or 5% (as seen in early 2026), investors often pull money out of "risky" stocks and move it into the safety of bonds.

2. Real-World Example: The "Fed Pause" of March 2026

We saw this play out vividly just, March 18, 2026.

The Federal Reserve elected to hold interest rates steady at 3.75%. While a "hold" is usually neutral, the market reacted with a sharp retreat. Why? Because the Fed's "dot plot" suggested only one rate cut for the rest of the year instead of the two or three the market had “priced in.”

The Result: The S&P 500 and Nasdaq slid as investors realized the "Higher for Longer" environment would persist. Tech giants, which rely on low-cost capital for AI infrastructure, saw immediate selling pressure because their "cheap money" dreams were delayed.

3. Sector Winners and Losers

Not all stocks react the same way to interest rate shifts.

| Sector | Reaction to Rising Rates | Why? |

|---|---|---|

| Technology / Growth | Negative | High valuations rely on low discount rates; high R&D costs. |

| Financials / Banks | Positive | Banks can charge more for loans (wider net interest margins). |

| Real Estate (REITs) | Negative | Highly sensitive to borrowing costs and mortgage rates. |

| Utilities | Negative | Often carry high debt and compete with bonds for "income" investors. |

| Value / Energy | Neutral/Positive | These companies often have "cash now" and are less sensitive to future discounting. |

4. The 2026 "AI Exception"

In 2026, we are seeing a unique phenomenon where the AI Supercycle is occasionally "breaking" the interest rate rule. Even with rates at 3.75%, companies like NVIDIA and specialized AI infrastructure firms have seen gains.

Explanation: If a company’s earnings growth is so explosive (e.g., 40% annually) that it outweighs the 4% cost of capital, the stock can still rise despite high rates. This is known as "Earnings Trumping Rates."