In the 2026 investment landscape, where volatility often tests the nerves of even seasoned investors, the Dividend Reinvestment Plan (DRIP) has emerged as a favorite "set-it-and-forget-it" tool for building long-term wealth. A DRIP is a programmed approach to investing that takes the cash dividends a company pays you and immediately uses that money to buy more shares of the same company.

Instead of receiving a cash deposit in your brokerage account—which you might be tempted to spend on a weekend getaway or a new gadget—the DRIP keeps your money working in the market, fueling a powerful cycle of compounding.

Definition Box:

Dividend Reinvestment Plan (DRIP): An automated investment strategy where cash dividends paid by a corporation or fund are automatically used to purchase additional shares or fractional shares of the underlying asset, rather than being distributed to the investor as cash.

How a DRIP Operates in 2026

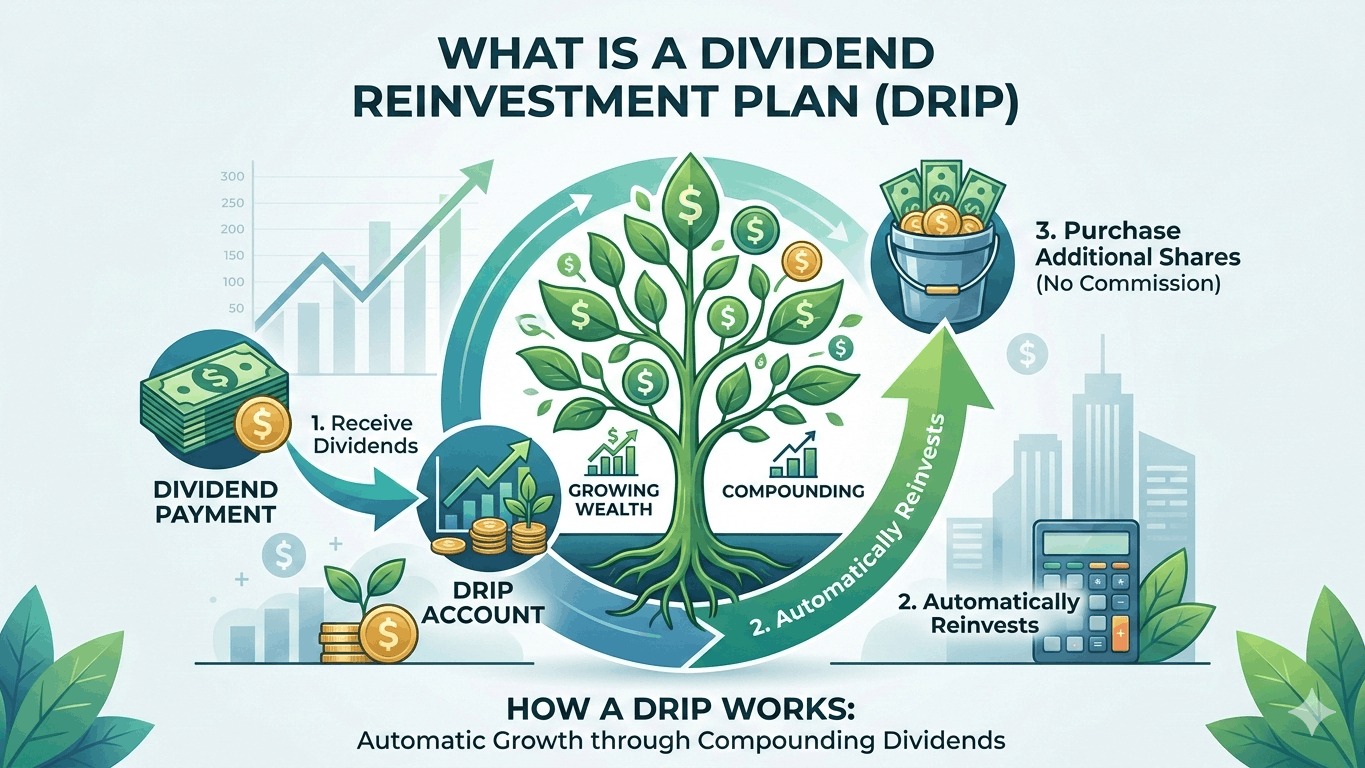

Most major U.S. brokerages and many dividend-paying corporations offer DRIPs. When you "enroll" a specific stock in a DRIP, the process becomes entirely hands-off.

- The Dividend Event: A company you own, such as a "Dividend King," declares and pays a quarterly dividend.

- Automatic Purchase: On the dividend payment date, your broker (or the company’s transfer agent) uses that cash to buy more shares.

- Fractional Shares: Because dividends are rarely the exact price of a full share, modern DRIPs in 2026 allow for fractional shares. If a stock costs $200 and your dividend is $50, you will see your holdings increase by 0.25 shares.

The "Math Magic" of Compounding

The true power of a DRIP isn't seen in a single quarter; it is seen over decades. This strategy creates a "snowball effect." As you acquire more shares through reinvestment, your next dividend payment is calculated based on a larger number of shares, which in turn buys even more shares.

Quick Example:

Imagine you own 100 shares of a company trading at $100 with a 4% annual dividend yield ($1 per share, paid quarterly).

- Quarter 1: You receive $100 in dividends. Instead of taking the cash, the DRIP buys you 1 new share. You now own 101 shares.

- Quarter 2: Your dividend is now calculated on 101 shares, giving you $101. This buys slightly more than one share.

- Over 20 Years: Without adding a single penny of your own money, your share count—and your quarterly "paycheck"—can more than double simply by letting the dividends "re-up" themselves.

Strategic Advantages of DRIPs

1. Dollar-Cost Averaging (DCA)

DRIPs are a natural form of dollar-cost averaging. Because the reinvestment happens automatically on a set date, you buy more shares when the stock price is low and fewer shares when the price is high. This lowers your average cost per share over time and removes the emotional stress of trying to “time the market.”

2. No Commission Fees

In 2026, most brokerage-operated DRIPs are entirely commission-free. While buying $50 worth of a stock manually might sometimes incur a small fee or spread at certain firms, DRIP transactions are usually executed as a service to shareholders at no extra cost.

3. Psychological Discipline

The greatest enemy of a long-term investor is often their own behavior. By automating the reinvestment, you remove the "decision fatigue" of what to do with your dividends. It ensures that 100% of your investment returns stay invested, preventing "leakage" where small cash amounts are slowly drained away for non-investment purposes.

The Tax Consideration (The "Catch")

It is a common misconception that because you didn't "touch" the cash, you don't owe taxes. In the eyes of the IRS in 2026, a reinvested dividend is treated exactly like a cash dividend.

If you hold your DRIP-enrolled stocks in a taxable brokerage account, you will still receive a 1099-DIV form at the end of the year and owe taxes on those dividends. For this reason, many investors prefer to run their DRIP strategies inside tax-advantaged accounts like a Roth IRA or 401(k), where the growth and reinvestment remain shielded from the taxman.

Is a DRIP Right for You?

If you are in the "Accumulation Phase" of your life—meaning you are working and building wealth for the future—a DRIP is almost always the right move. It automates your growth and ensures your portfolio is constantly expanding.

However, if you are in the "Distribution Phase" (retirement), you might choose to turn off the DRIP. At that stage, you may need that quarterly cash to cover your living expenses, using the dividends as a "salary" while keeping your original shares intact.