As of March 2026, the barrier to entry for the stock market has never been lower. With the rise of fractional shares, zero-commission trading, and AI-driven portfolio builders, anyone with a smartphone and $10 can become an owner of the world’s most powerful companies. However, for a beginner standing at the starting line, the first major tactical decision is often the most daunting: Should you buy index funds or pick individual stocks?

This choice isn't just about "which makes more money." It is about your personality, your time, and your ability to stomach the "rollercoaster" of market volatility. In the current 2026 economy—where AI is reshuffling the S&P 500 leaderboard and interest rates have finally found a "new normal"—understanding the structural difference between these two paths is the key to long-term wealth.

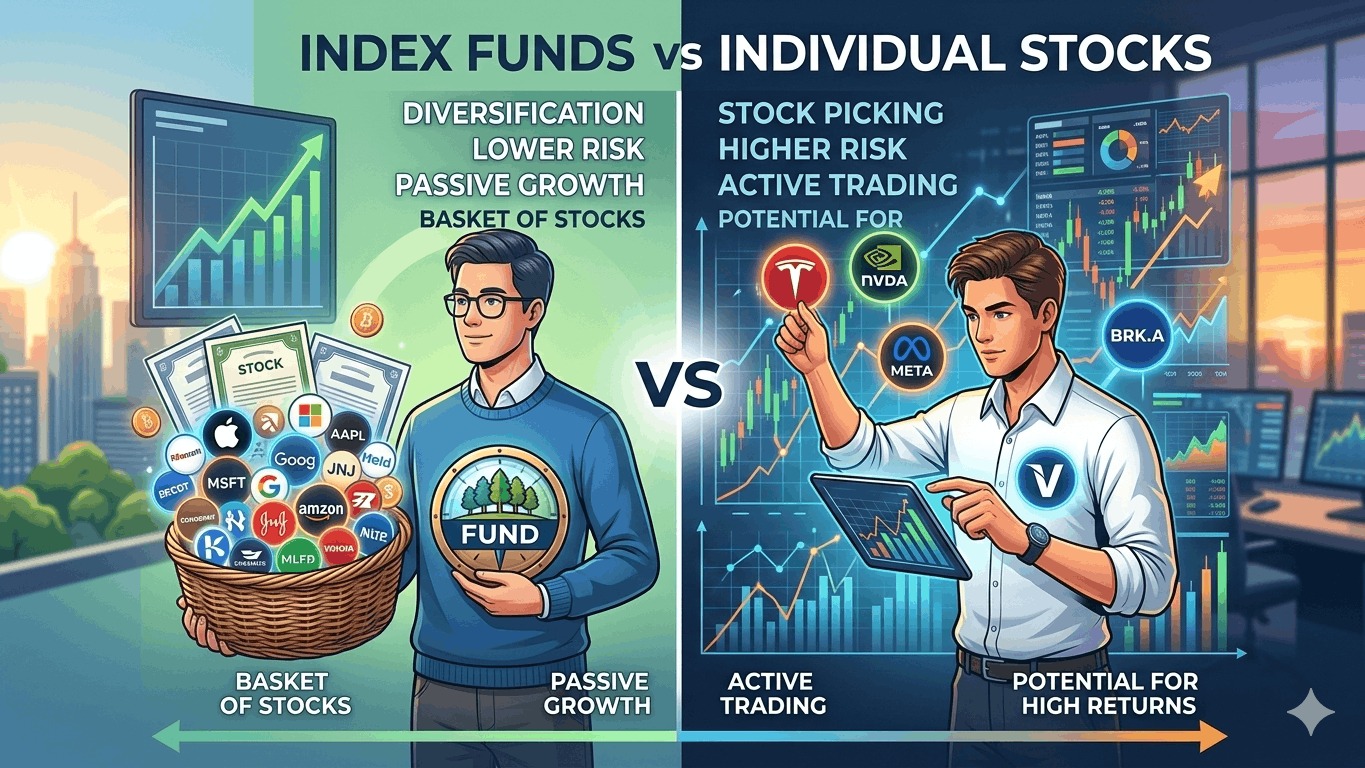

Definition Box:

Index funds are diversified funds that track a market index (like the S&P 500), while individual stocks are shares of single companies that investors choose one by one.

1. The Case for Index Funds: The "Set and Forget" Strategy

An index fund is a type of mutual fund or Exchange-Traded Fund (ETF) with a portfolio constructed to match or track the components of a financial market index. When you buy an S&P 500 index fund, you are essentially buying a tiny "slice" of the 500 largest profitable companies in the United States.

The Power of Diversification

The biggest advantage of index funds is instant diversification. If you put all your money into one tech stock and that company faces a massive regulatory scandal or a failed product launch, your net worth could plummet overnight. In an index fund, if one company fails, it is balanced out by 499 others. In fact, if a company in the index consistently underperforms, the index simply "kicks them out" and replaces them with the next rising star.

Low Costs and "Average" Success

Index funds are "passively managed," meaning there isn't a highly-paid fund manager trying to beat the market. This keeps the fees (expense ratios) incredibly low—often near 0.03%.

Why Beginners Love Index Funds in 2026

In 2026, the "Total Stock Market" approach remains the gold standard for beginners. It removes the "analysis paralysis" of trying to figure out which AI chipmaker or green energy firm will win the decade. By owning the whole market, you are guaranteed to capture the winners.

Quick Comparison:

Index funds are usually simpler and less risky for beginners, while individual stocks offer more control and potentially higher returns with more risk.

2. The Case for Individual Stocks: The "High Conviction" Strategy

Buying individual stocks means you are selecting specific companies—like Apple, Tesla, or a specialized biotech firm—because you believe that specific business will outperform the broader market.

The Potential for Outsized Returns

While an index fund might give you a steady 8% to 10% annual return, an individual stock could potentially double or triple in value in a short period. This is the primary "hook" for individual stock picking: the chance to find the "next big thing" before the rest of the world does.

Control and Alignment

Picking stocks allows you to build a portfolio that reflects your personal values or professional expertise. If you work in cybersecurity and see a specific firm's software being adopted everywhere, you can choose to "overweight" that company in your portfolio. You have total control over what you own and when you sell.

3. The Reality Check: Risk vs. Effort

For a beginner in 2026, the "cost" of picking individual stocks isn't just the money—it's the time.

- The Index Fund Effort: Roughly 10 minutes a month. You set up an automated transfer from your bank account and check your balance once a quarter.

- The Individual Stock Effort: Roughly 5–10 hours a week. To do this "safely," you must read earnings reports, listen to CEO calls, analyze debt-to-equity ratios, and keep a pulse on global competitors.

The Hard Truth: Data shows that roughly 90% of professional fund managers fail to beat the S&P 500 over a 15-year period. If the pros with supercomputers and Ph.D.s struggle to beat the index, a beginner picking stocks based on "gut feeling" is statistically likely to underperform.

4. The 2026 "Hybrid" Approach

Many successful investors in 2026 use a strategy called “Core and Satellite.”

- The Core (80-90%): You place the vast majority of your money into a broad-market index fund (like VTI or VOO). This ensures you will reach your long-term goals (like a $1 million retirement) with high probability.

- The Satellite (10-20%): You use a smaller "fun" portion of your money to pick individual stocks. This allows you to learn about business analysis and potentially "juice" your returns without risking your entire financial future if one pick goes to zero.

5. Identifying Your "Investor Type"

To decide which is better for you, ask yourself these three questions:

- Do I enjoy reading financial statements? If yes, you might enjoy individual stocks. If the thought makes you yawn, stick to index funds.

- Can I handle seeing a 50% drop in one of my holdings? Individual stocks can be incredibly volatile. Index funds drop too, but they rarely go to zero.

- What is my goal? If your goal is "Financial Freedom" by age 50, the index fund path is the most reliable "slow and steady" route.

6. Common 2026 Pitfalls for Beginners

- Chasing Hype: In 2026, "AI-themed" individual stocks are everywhere. Beginners often buy at the peak because of "FOMO" (Fear Of Missing Out). Index funds protect you from this by automatically balancing your exposure.

- Over-Diversification of Stocks: If you buy 50 different individual stocks, you have essentially created your own "expensive index fund" but with way more paperwork. If you want 50+ companies, just buy the index.

- Ignoring Taxes: Every time you sell an individual stock for a profit, you owe the government a cut. Index funds are generally more "tax-efficient" because they have lower turnover.

Summary: The Final Verdict

For the vast majority of beginners in 2026, index funds are the better choice. They offer the highest probability of success with the lowest amount of stress.

However, the "best" strategy is the one you can actually stick to. If owning a few shares of a company you love keeps you interested in the market and encourages you to save more, then a small allocation to individual stocks is a great way to learn. Just remember: build your "Core" first, and only play with the "Satellite" once your foundation is secure.