Building wealth is not just about finding the next hot stock or chasing whatever investment is trending online. For most people in the United States, long-term investing works better when it is built on balance, patience, and risk management. That is where diversification comes in.

A diversified investment portfolio is a portfolio that spreads money across different types of assets, sectors, industries, and sometimes even countries. The goal is simple: reduce the damage that any single investment can cause if it performs poorly. Instead of relying too heavily on one stock, one industry, or one asset class, diversification helps create a more stable foundation for long-term growth.

This does not mean diversification eliminates risk. No investment strategy can do that. Markets can still fall, and portfolios can still lose value. But diversification can help reduce concentration risk and smooth out some of the ups and downs that come with investing.

For beginner investors and experienced investors alike, learning how to build a diversified portfolio is one of the most important steps in creating a smart long-term investment plan.

What Is a Diversified Investment Portfolio?

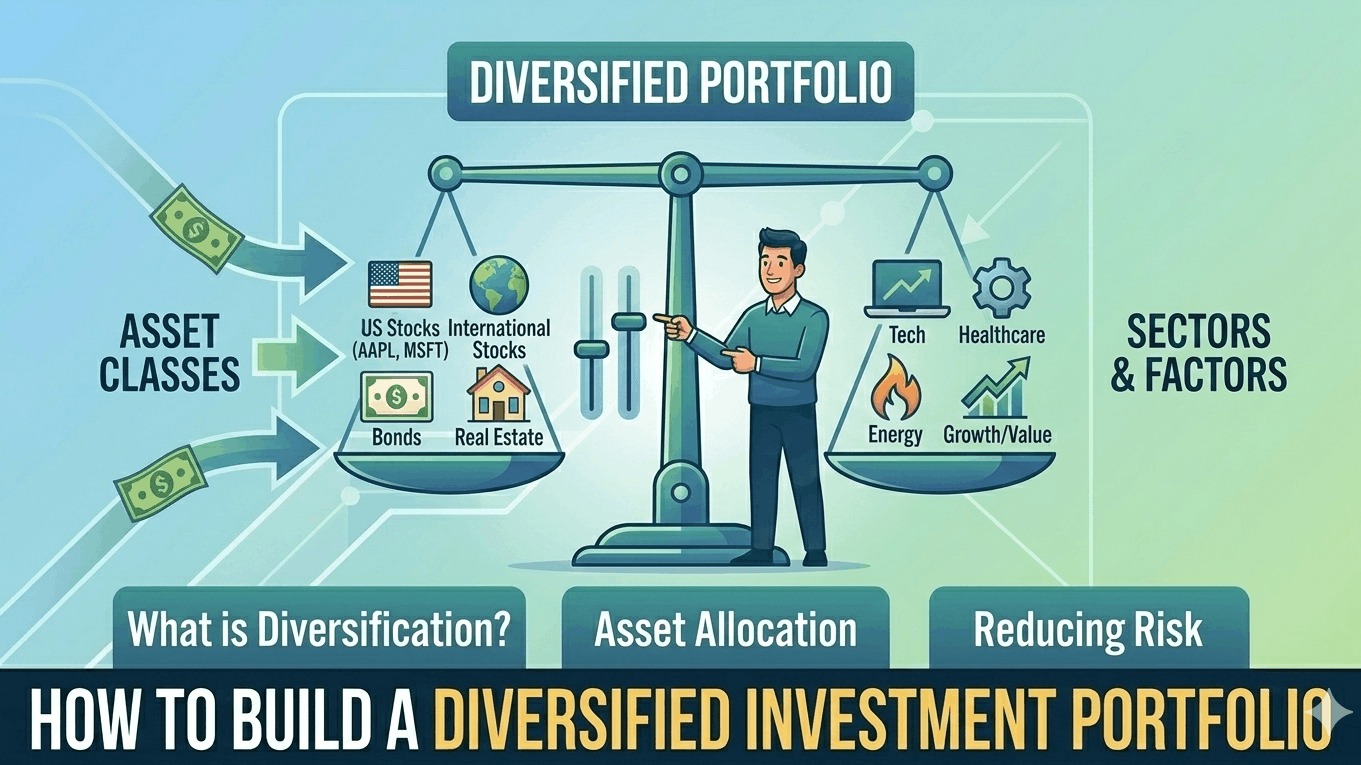

A diversified investment portfolio is a mix of different investments designed to work together rather than depend on one outcome. Instead of putting all your money into one company or one type of asset, you spread it across multiple areas of the market.

A diversified portfolio can include:

- U.S. stocks

- International stocks

- Bonds

- Cash or cash equivalents

- Real estate-related investments

- Index funds or ETFs

- Dividend-focused funds

- Growth and value investments

The purpose is to avoid having your entire portfolio rise or fall based on one narrow part of the market.

For example, if someone invests only in technology stocks, their portfolio may do very well when that sector is strong. But if technology struggles, the entire portfolio may suffer. A diversified approach spreads exposure across different areas so that weakness in one section may be offset by strength in another.

Why Diversification Matters

Diversification matters because markets are unpredictable. Different investments perform differently at different times. Stocks may surge while bonds lag. U.S. markets may outperform international markets for a period, then the opposite may happen later. One industry may boom while another struggles.

A diversified portfolio is built around the idea that you do not need to predict exactly which asset will perform best next year. Instead, you build a portfolio that can participate in growth across different areas while lowering the risk of extreme concentration.

Here are a few reasons diversification is so valuable:

It reduces concentration risk

It can smooth volatility

It supports long-term discipline

It creates flexibility

The Main Building Blocks of a Diversified Portfolio

To build a diversified investment portfolio, it helps to understand the major asset classes and the role each can play.

1. U.S. stocks

U.S. stocks are often a core part of a long-term portfolio. They offer growth potential and exposure to companies across major industries such as technology, healthcare, finance, industrials, and consumer goods.

Investors can diversify within U.S. stocks by owning:

- Large-cap stocks

- Mid-cap stocks

- Small-cap stocks

- Growth stocks

- Value stocks

- Broad index funds

Many people use total market funds or S&P 500 index funds to get broad exposure.

2. International stocks

A portfolio invested only in the U.S. market may miss opportunities outside the country. International stocks provide exposure to companies in developed markets and emerging markets.

This adds another layer of diversification because economic conditions, interest rates, currency movements, and growth trends vary across regions.

International investing can help reduce reliance on the performance of the U.S. economy alone.

3. Bonds

Bonds are often used to add stability, reduce volatility, and provide income. They usually play a larger role in portfolios for conservative investors or those closer to retirement.

A portfolio may include:

- U.S. Treasury bonds

- Corporate bonds

- Municipal bonds

- Total bond market funds

Bonds do not offer the same long-term growth potential as stocks, but they can help balance risk.

4. Cash or cash equivalents

Cash, money market funds, and similar low-risk holdings are not major growth assets, but they can provide liquidity and stability. Investors may keep some cash for emergencies, short-term needs, or to reduce overall portfolio volatility.

5. Real estate-related investments

Some investors add diversification through real estate investment trusts, often called REITs, or through broader real estate funds. These can provide exposure to property-related income and market segments outside traditional stocks and bonds.

Diversification by Asset Class vs Diversification Within Asset Class

A lot of people think diversification simply means owning many different stocks. But true diversification goes deeper than that.

You can diversify between asset classes, such as holding stocks, bonds, and cash. You can also diversify within each asset class, such as spreading stock exposure across U.S. companies, international companies, sectors, and company sizes.

For example, owning 20 technology stocks is not the same as owning a truly diversified stock portfolio. Even though you own many investments, they are all tied to the same sector. If that sector performs poorly, your portfolio may still drop sharply.

A stronger approach is to diversify across:

- Asset classes

- Market sectors

- Geographic regions

- Company sizes

- Investment styles

How to Build a Diversified Investment Portfolio Step by Step

Building a diversified portfolio does not need to be overly complicated. In many cases, a few well-chosen funds can provide broad diversification.

Step 1: Define your investment goal

Start by deciding what the portfolio is meant to do. Are you investing for retirement, long-term wealth building, a future home purchase, or financial independence?

The goal affects how much risk you can take and how long you can stay invested.

Someone investing for retirement 25 years away may want a growth-focused portfolio. Someone who needs money in three years may need a more conservative approach.

Step 2: Know your time horizon

Your time horizon is the amount of time before you expect to need the money.

A longer time horizon usually allows for more stock exposure because there is more time to recover from market downturns. A shorter time horizon often calls for less volatility and more emphasis on capital preservation.

Step 3: Understand your risk tolerance

Risk tolerance is your ability and willingness to handle market declines. This is not just about how much return you want. It is about how you react when your investments drop in value.

A diversified portfolio should match your comfort level. If a portfolio is too aggressive, you may panic and sell at the wrong time.

Step 4: Choose your asset allocation

Asset allocation is the mix of stocks, bonds, cash, and other investments in your portfolio. This is one of the most important decisions in portfolio design.

A younger investor with a long time horizon may choose a stock-heavy portfolio. A more conservative investor may include a larger bond allocation.

Here is a simple example table showing sample portfolio allocations for different investor styles:

| Investor Type | U.S. Stocks | International Stocks | Bonds | Cash/Other |

|---|---|---|---|---|

| Aggressive | 60% | 25% | 10% | 5% |

| Moderate | 45% | 20% | 30% | 5% |

| Conservative | 25% | 10% | 55% | 10% |

These are only general examples, but they show how diversification can look different depending on the investor.

Step 5: Use broad funds to simplify diversification

Many investors build diversified portfolios using low-cost index funds or ETFs. This can be much easier than selecting many individual securities.

For example, an investor might use:

- A total U.S. stock market fund

- An international stock fund

- A U.S. bond fund

- A REIT fund or cash allocation if needed

This structure can provide broad exposure while keeping the portfolio manageable.

Step 6: Diversify within your stock allocation

Even inside the stock portion of the portfolio, diversification matters. A good stock mix may include different company sizes, sectors, and regions.

For example:

- Large-cap U.S. companies

- Small-cap U.S. companies

- Developed international markets

- Emerging markets

This helps avoid overdependence on one narrow segment.

Step 7: Rebalance periodically

Over time, some investments grow faster than others. This can shift your portfolio away from its target allocation.

For example, if stocks rise sharply, they may become too large a percentage of your portfolio. Rebalancing means adjusting the portfolio back to the desired mix.

This helps keep risk aligned with your plan.

Example of a Simple Diversified Portfolio

A beginner investor who wants a simple long-term approach might build a portfolio like this:

| Investment Type | Example Allocation | Role in Portfolio |

|---|---|---|

| U.S. total stock market fund | 50% | Core growth |

| International stock fund | 20% | Global diversification |

| U.S. bond market fund | 25% | Stability and income |

| REIT or cash | 5% | Extra diversification or liquidity |

This is only an example, but it shows how a portfolio can be spread across different areas without becoming too complex.

Diversified Portfolio Example by Life Stage

Different stages of life often call for different portfolio structures. Here is a general example table:

| Life Stage | Typical Diversification Focus | Portfolio Style |

|---|---|---|

| Early career | Growth and long time horizon | Higher stock allocation |

| Mid-career | Growth plus balance | Mix of stocks and bonds |

| Near retirement | Stability and income | Higher bond allocation |

| Retirement | Income, preservation, controlled growth | Balanced and lower volatility |

This does not mean everyone in the same age group should invest the same way. But life stage often affects time horizon and risk needs.

Limits of Diversification

Diversification is powerful, but it does have limits.

It does not guarantee profits. It does not prevent losses in a market crash. If most markets are falling at the same time, a diversified portfolio can still decline.

Also, too much complexity can make a portfolio harder to manage. A diversified portfolio should be broad enough to reduce concentration risk, but simple enough to understand and maintain.

Good diversification is about thoughtful balance, not owning as many investments as possible.

Final Thoughts

Learning how to build a diversified investment portfolio is one of the most important parts of successful long-term investing. A diversified portfolio spreads money across different asset classes, market segments, and regions so that your financial future is not tied too closely to one investment or one trend.

For most U.S. investors, diversification is not about making a portfolio exciting. It is about making it durable.

A strong diversified portfolio often includes a mix of U.S. stocks, international stocks, bonds, and other supporting assets based on your goals, time horizon, and risk tolerance. It can be built with individual investments, but many people simplify the process with index funds and ETFs.

The best diversified portfolio is not the most complicated one. It is the one you can understand, maintain, and stick with over the long term. When your portfolio is built around balance and discipline instead of guesswork, you give yourself a stronger foundation for long-term growth and financial stability.