If you've ever looked at your paycheck and wondered why so much is missing — or panicked thinking a raise might actually cost you money — you're not alone. Tax brackets confuse millions of Americans every year. The good news? Once you understand how they actually work, you'll never fear them again.

This guide breaks down everything you need to know about U.S. federal tax brackets in plain, simple language, updated with the latest 2025 and 2026 figures from the IRS.

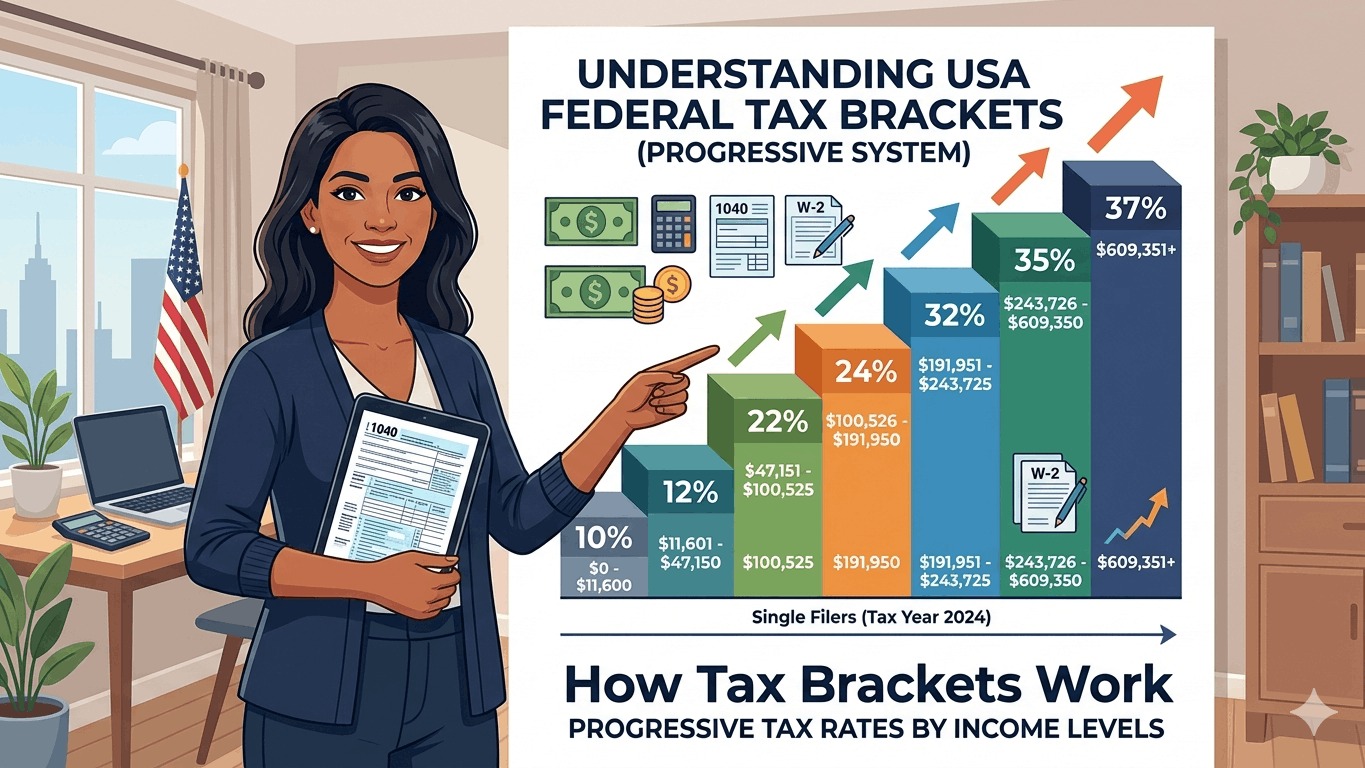

What Is a Tax Bracket?

A tax bracket is a range of income that is taxed at a specific rate. The United States uses a progressive tax system, meaning the more you earn, the higher the rate you pay — but only on the portion of income that falls within each bracket.

This is one of the most misunderstood concepts in personal finance. Many people believe that earning more money can leave them with less take-home pay. That is a myth — and we will explain exactly why below.

To understand what counts as income in the first place, read our full guide on What Is Taxable Income.

What's New in 2025–2026? (One Big Beautiful Bill Act)

A major tax law update happened in July 2025. The One Big Beautiful Bill Act (OBBBA) permanently extended most provisions of the 2017 Tax Cuts and Jobs Act (TCJA) that were set to expire at the end of 2025. Key changes include:

- The seven tax brackets (10%–37%) are now permanently locked in

- The standard deduction saw significant increases

- An additional "bonus" deduction for seniors aged 65+ was introduced

- The Child Tax Credit increased to $2,200 for 2025 and 2026

- The 37% bracket now has a limitation on itemized deduction benefits for top earners

These are the most consequential tax law changes since the original TCJA passed in 2017 and directly affect your 2025 return (filed in 2026) and your 2026 planning.

2025 Federal Tax Brackets (Single Filers)

(Income earned in 2025 — returns filed in early 2026)

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 – $11,925 |

| 12% | $11,926 – $48,475 |

| 22% | $48,476 – $103,350 |

| 24% | $103,351 – $197,300 |

| 32% | $197,301 – $250,525 |

| 35% | $250,526 – $626,350 |

| 37% | Over $626,350 |

2025 Federal Tax Brackets (Married Filing Jointly)

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 – $23,850 |

| 12% | $23,851 – $96,950 |

| 22% | $96,951 – $206,700 |

| 24% | $206,701 – $394,600 |

| 32% | $394,601 – $501,050 |

| 35% | $501,051 – $751,600 |

| 37% | Over $751,600 |

2026 Federal Tax Brackets (Single Filers)

(Income earned in 2026 — returns filed in early 2027)

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 – $12,400* |

| 12% | $12,401 – $50,250* |

| 22% | $50,251 – $105,700* |

| 24% | $105,701 – $201,900* |

| 32% | $201,901 – $256,100* |

| 35% | $256,101 – $640,600 |

| 37% | Over $640,600 |

2026 Federal Tax Brackets (Married Filing Jointly)

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 – $24,850* |

| 12% | $24,851 – $100,500* |

| 22% | $100,501 – $211,400* |

| 24% | $211,401 – $403,800* |

| 32% | $403,801 – $512,200* |

| 35% | $512,201 – $768,600 |

| 37% | Over $768,600 |

*Note: For 2026, the OBBBA applied a special 4% inflation adjustment to the bottom two brackets (10% and 12%) and a 2.3% adjustment to upper brackets. Exact thresholds for all brackets are per IRS Revenue Procedure 2025-32.

The top marginal rate of 37% applies to income above $640,600 for single filers and $768,600 for married filers in 2026.

How Tax Brackets Actually Work: Step-by-Step Example

Many people assume their entire salary is taxed at their bracket's rate. That is not how it works. Let's walk through it clearly.

Scenario: You are a single filer with $70,000 in taxable income in 2025.

Here is how your federal tax is calculated — layer by layer:

| Bracket | Income Taxed | Rate | Tax Owed |

|---|---|---|---|

| 10% | $11,925 | 10% | $1,192.50 |

| 12% | $36,550 ($11,926–$48,475) | 12% | $4,386.00 |

| 22% | $21,525 ($48,476–$70,000) | 22% | $4,735.50 |

| Total | $10,314 |

Your marginal tax rate = 22% (your highest bracket) Your effective tax rate = $10,314 ÷ $70,000 = ~14.7%

Even though you're "in the 22% bracket," you only pay 22 cents on the dollar for income above $48,475. Everything below is taxed at lower rates.

Marginal Tax Rate vs. Effective Tax Rate

This distinction is crucial for smart financial planning:

| Term | What It Means | When It Matters |

|---|---|---|

| Marginal Rate | Tax rate on your next dollar of income | Deciding whether to take a bonus, contribute to a 401(k), or defer income |

| Effective Rate | Your actual average tax rate on all income | Comparing your real tax burden year over year |

Most Americans pay an effective federal tax rate well below their marginal bracket rate — because the progressive system taxes the lower layers at lower rates.

2025 & 2026 Standard Deductions

Tax brackets apply to taxable income, not your gross paycheck. Before a single dollar hits the brackets, you subtract deductions. Here are the updated numbers:

| Filing Status | 2025 Standard Deduction | 2026 Standard Deduction |

|---|---|---|

| Single | $15,000 | $16,100 |

| Married Filing Jointly | $30,000 | $32,200 |

| Head of Household | $22,500 | $24,150 |

The OBBBA also added a temporary bonus deduction for seniors (age 65+): an extra $2,000 for single filers and $1,600 per eligible spouse for married filers, beginning in the 2025 tax year.

To understand which deduction strategy saves you the most money, read our guide: Standard Deduction vs Itemized Deduction.

Real-World Scenario: What You Actually Owe

Meet James, a single professional earning $85,000/year in 2025.

Step 1 — Calculate Taxable Income:

- Gross income: $85,000

- Standard deduction: −$15,000

- Taxable income: $70,000

Step 2 — Apply the 2025 Brackets:

- 10% on $11,925 = $1,192.50

- 12% on $36,550 = $4,386.00

- 22% on $21,525 = $4,735.50

Total Federal Tax: $10,314 Effective Tax Rate: ~12.1% Marginal Tax Rate: 22%

James pays just 12.1 cents on every dollar earned — far less than the 22% bracket label suggests. That's the progressive tax system working exactly as designed. For a full breakdown of how gross income becomes taxable income, see our article on What Is Taxable Income.

Will a Raise Ever Hurt You? Absolutely Not.

This is the most persistent tax myth in America: "If I earn more, I'll be pushed into a higher bracket and take home less."

This is false. Here's why:

Only the dollars above a bracket threshold move to the higher rate. If you earn $48,475 (the top of the 12% bracket in 2025) and get a $1,000 bonus, only that $1,000 is taxed at 22%. Your first $48,475 stays taxed at 10% and 12% — exactly as before.

You will always take home more money by earning more. The system is designed to ensure that.

Key 2025–2026 Tax Numbers at a Glance

| Item | 2025 | 2026 |

|---|---|---|

| Top bracket threshold (Single) | $626,350 | $640,600 |

| Top bracket threshold (MFJ) | $751,600 | $768,600 |

| Standard deduction (Single) | $15,000 | $16,100 |

| Standard deduction (MFJ) | $30,000 | $32,200 |

| Child Tax Credit | $2,200 | $2,200 |

| 401(k) contribution limit | $23,500 | TBD by IRS |

| IRA contribution limit | $7,000 | $7,500 |

| Estate tax exemption | $13,990,000 | $15,000,000 |

| Gift tax annual exclusion | $19,000 | $19,000 |

Federal Brackets vs. State Income Taxes

The brackets above are federal only. Most Americans also owe state income taxes, calculated completely separately. Each state has its own rules:

- No income tax states (9): Texas, Florida, Nevada, Washington, Alaska, Wyoming, South Dakota, Tennessee, New Hampshire

- Flat tax states: One rate for all income (e.g., Illinois at 4.95%, Colorado at 4.4%)

- Progressive tax states: Multiple brackets (e.g., California tops out at 13.3%, New York at 10.9%)

Federal and state taxes are filed independently and do not interact with each other's brackets. Our detailed guide Federal vs State Taxes Explained walks through how both systems work side by side.

Tips to Reduce Your Tax Bracket Exposure in 2025–2026

You can legally reduce your taxable income — and potentially drop into a lower bracket — through smart strategies:

1. Max out your 401(k) The 2025 contribution limit is $23,500 (up from $23,000 in 2024). Pre-tax contributions directly reduce your taxable income dollar-for-dollar.

2. Contribute to a Traditional IRA For 2025, you can contribute up to $7,000 ($8,000 if you're 50+). The 2026 limit rises to $7,500. Deductible contributions lower your taxable income.

3. Use an HSA Health Savings Account contributions are fully tax-deductible. The 2025 limit is $4,300 for self-only coverage and $8,550 for family coverage.

4. Choose your deduction method wisely The standard deduction is larger than ever — but if your mortgage interest, charitable contributions, and state taxes exceed the threshold, itemizing can save more. See our comparison: Standard Deduction vs Itemized Deduction.

5. Seniors: Claim your bonus deduction Adults 65 and older can now claim an extra $2,000 (single) or $1,600 per eligible spouse (joint) thanks to the OBBBA. Don't leave this on the table.

6. Consider tax-loss harvesting If you have investment losses, they can offset capital gains and up to $3,000 of ordinary income per year.

For a deeper understanding of how all these strategies connect to your overall income tax picture, visit our guide: How Income Taxes Work in the USA.

How the IRS Adjusts Brackets Each Year

Every fall, the IRS announces updated bracket thresholds, deduction amounts, and credit limits for the following year. They use the Chained Consumer Price Index (C-CPI-U) — a measure of inflation — to calculate how much each threshold should move.

This annual process, called inflation indexing, prevents "bracket creep" — a situation where rising prices push workers into higher tax brackets even without any real increase in their purchasing power.

For 2025, the average adjustment was about 2.8% across most provisions. For 2026, the OBBBA added a special 4% inflation adjustment specifically to the bottom two brackets (10% and 12%), giving lower-income earners extra relief.

Common Tax Bracket Myths — Busted

| Myth | Reality |

|---|---|

| "A raise can push me into a higher bracket and I'll take home less" | False — only the additional income is taxed at the higher rate |

| "My whole income is taxed at my bracket's rate" | False — each slice of income is taxed at its own rate |

| "Everyone in the same bracket pays the same tax" | False — deductions and credits vary widely by individual |

| "The 37% bracket applies to most high earners" | False — it only applies above $626,350 (2025 single) |

| "The tax brackets changed dramatically in 2025" | Partially — the OBBBA made rates permanent and increased deductions, but the seven-rate structure stayed the same |

Final Thoughts

Understanding how tax brackets work is one of the most empowering personal finance lessons available. The U.S. tax system is progressive — but it is structured so that earning more always puts more money in your pocket. The real opportunity is in knowing how to reduce your taxable income through deductions, retirement accounts, and smart planning.

With the permanent changes brought by the One Big Beautiful Bill Act in 2025, now is an especially important time to revisit your tax strategy.

For the complete picture of how your taxes are calculated from the ground up, start with our comprehensive guide: How Income Taxes Work in the USA.