In 2026, your credit score is the single most influential factor in determining your mortgage interest rate. While the Federal Reserve's policies set the "floor" for rates, your credit score determines how many floors up you’ll be living.

With the full 2026 implementation of FICO 10T and VantageScore 4.0 by Fannie Mae and Freddie Mac, lenders now have a more granular view of your financial health, rewarding those with stable "trended data" while penalizing those with recent debt spikes.

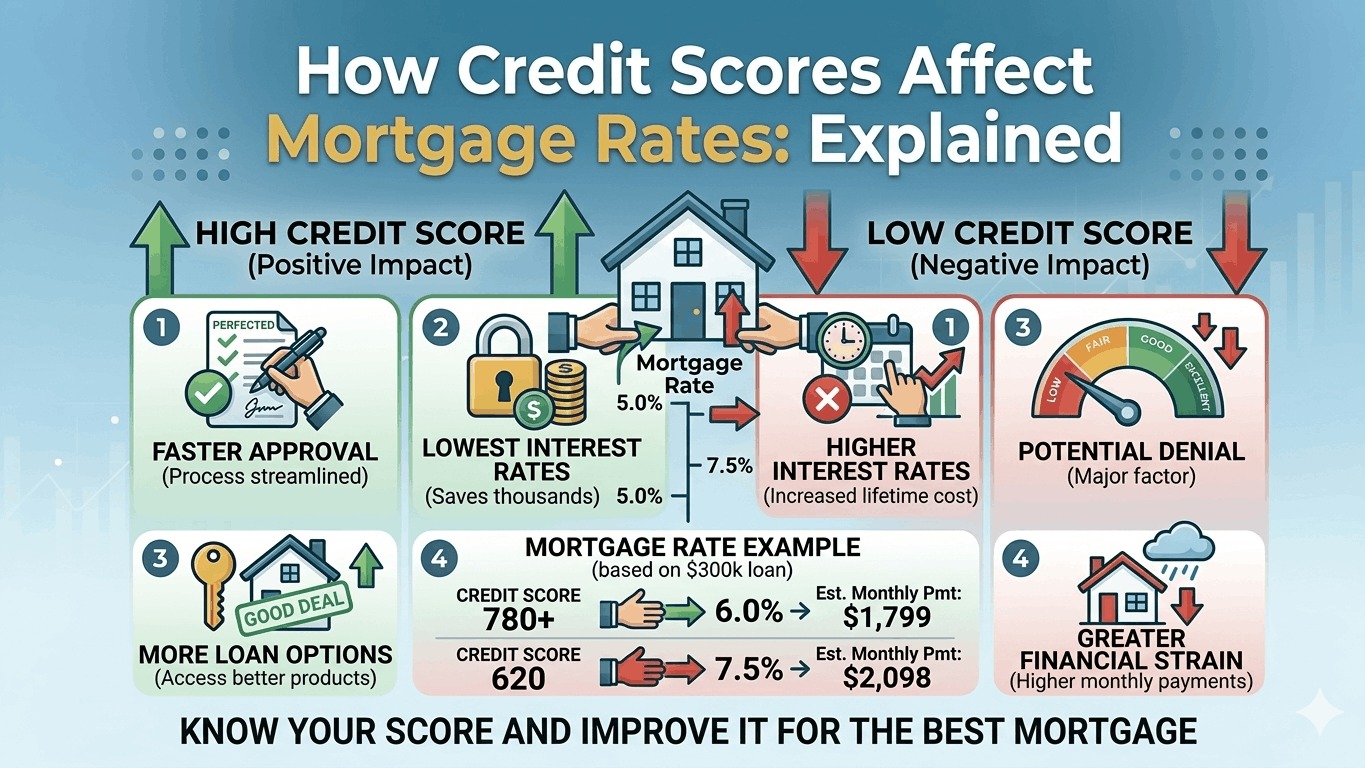

1. 2026 Mortgage Rate Tiers

As of March 2026, the gap between a "Fair" and "Exceptional" credit score can mean a difference of over 1.5% in interest. On a $400,000 loan, that small percentage gap equals roughly $150,000+ in extra interest over 30 years.

Estimated 30-Year Fixed Rates (March 2026)

| Credit Score Range | Typical Interest Rate | Monthly Principal & Interest* |

|---|---|---|

| 760 – 850 | 5.95% | $2,385 |

| 700 – 759 | 6.40% | $2,502 |

| 680 – 699 | 6.85% | $2,621 |

| 620 – 679 | 7.45% | $2,783 |

| < 620 | 8.10%+ (or FHA Only) | $2,965 |

*Estimates based on a $400,000 loan. Actual rates vary daily by lender.

2. The LLPA Factor: Why Your Rate Varies

In the U.S., most conventional loans are governed by Loan-Level Price Adjustments (LLPAs). These are mandatory risk fees set by the FHFA.

- The 2026 Reality: If you have a 640 score, you are hit with a higher LLPA fee than someone with a 780 score. Lenders don't usually ask you to pay this fee in cash; instead, they "bake" it into your interest rate.

- The "Sweet Spot": In 2026, the best rate breaks often occur at the 720, 740, and 760 marks. Crossing into the 760+ tier is often the final threshold to unlock the "advertised" rates you see on TV.

3. FICO 10T: The New "Stability" Score

Starting in 2026, mortgage lenders are officially looking back 24 months into your history using FICO 10T.

- Old Way: If you paid off all your credit cards right before applying, your score would jump, and you’d get a better rate.

- New Way: FICO 10T looks at whether you've been carrying high balances for the last two years. If your balances have been steadily decreasing, you’ll likely see a better rate than someone who just made a "last-minute" payment to fix their score.

4. Strategies to Improve Your Rate Before Applying

If you are planning to buy a home in 2026, use these three tactics 6–12 months in advance:

- The "Utilization Anchor": Keep your credit card usage below 3% of your limits. In the trended data era, showing a long-term pattern of low utilization is the fastest way to a "Superprime" rate.

- Avoid "New Credit" Shocks: Do not open new credit cards or auto loans within 12 months of your mortgage application. New accounts lower your "Average Age of Accounts," which can push you down into a lower rate tier.

- The Middle Score Rule: Most lenders pull three scores (Equifax, Experian, TransUnion) and use the middle number. If your scores are 720, 745, and 760, your "mortgage score" is 745. Focus on the bureau with the lowest score to bring your middle number up.