In the 2026 financial landscape, where lenders use advanced models like FICO 10T and VantageScore 4.0, your "credit age" has become a vital indicator of stability. While your payment history shows if you pay your bills, your credit history length shows how long you’ve been doing it.

Lenders view a long credit history as a proven track record. In 2026, the "Length of Credit History" accounts for 15% of your FICO Score and is considered "Highly Influential" (roughly 20%) for your VantageScore.

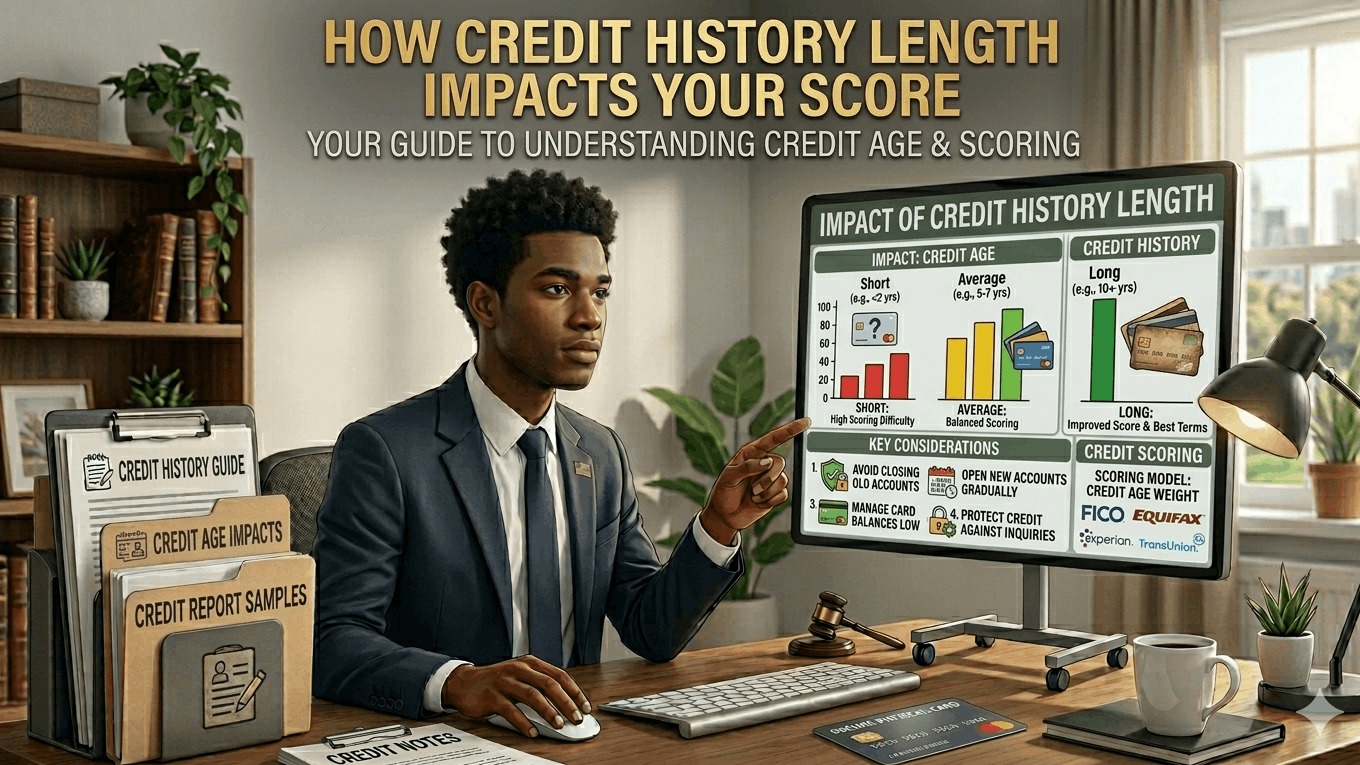

1. The Three Components of Credit Age

Lenders don't just look at one date. They calculate your "age" using three specific metrics:

- The Age of Your Oldest Account: This establishes your "entry point" into the U.S. financial system. Even if you don't use your oldest card, keeping it open maintains this anchor.

- The Age of Your Newest Account: This tells lenders if you are currently "credit-hungry." Opening a new card in 2026 resets this clock to zero months.

- The Average Age of Accounts (AAoA): This is the most sensitive metric. It is the sum of the ages of all your accounts divided by the number of accounts.

Example: If you have one card that is 10 years old and you open a brand new one today, your Average Age of Accounts instantly drops from 10 years to 5 years.

2. FICO vs. VantageScore: The 2026 Difference

In 2026, the two major scoring models treat age slightly differently, especially regarding closed accounts.

- FICO Models: These are the "Gold Standard" for mortgages. FICO typically continues to count closed accounts in your average age for 10 years after they are closed (if they were in good standing).

- VantageScore: Some older versions of VantageScore stop counting an account the moment it is closed. This is why you might see a sudden score drop on apps like Credit Karma when you close a card, even if your FICO score remains stable.

3. The "Authorized User" Hack

If you have a "thin" credit file (less than 2 years of history), 2026 lenders still allow "piggybacking."

- The Move: A family member adds you as an Authorized User on a card they’ve had for 15 years.

- The Result: That 15-year history is often added to your report, instantly increasing your oldest account age and your average age without you ever spending a dollar.

4. Why You Should Never Close Your Oldest Card

The most common mistake in 2026 is closing an "old" card because it doesn't have good rewards.

- The Impact: Closing your oldest card will eventually shorten your credit history. While the impact might not be immediate on a FICO score, it reduces your "Total Available Credit," which can hurt your Utilization Ratio (30% of your score) instantly.

- The 2026 Fix: Instead of closing it, "Product Change" it. Ask the bank to swap the card to a different version with no annual fee so you can keep the account age active forever.

5. Timeline: How Much Age is "Enough"?

In the 2026 market, credit age is a slow-burn factor. You cannot rush time, but you can understand the tiers:

- Short (Under 2 years): Considered a "Thin File." You may struggle to get the absolute lowest mortgage rates.

- Moderate (2–7 years): You are becoming an established borrower.

- Strong (7–10+ years): This is the "sweet spot." Most people with 800+ credit scores have an average account age of at least 9 years.