In 2026, your credit score is the most important "financial grade" you own. While the 300–850 range has remained the standard for decades, the way lenders interpret these numbers has evolved. With the full integration of FICO 10T and VantageScore 4.0, banks now look at "trended data"—not just where your score is today, but whether your financial health is improving or declining over time.

Understanding where you fall on the 300–850 scale is the first step toward unlocking lower interest rates and better housing options.

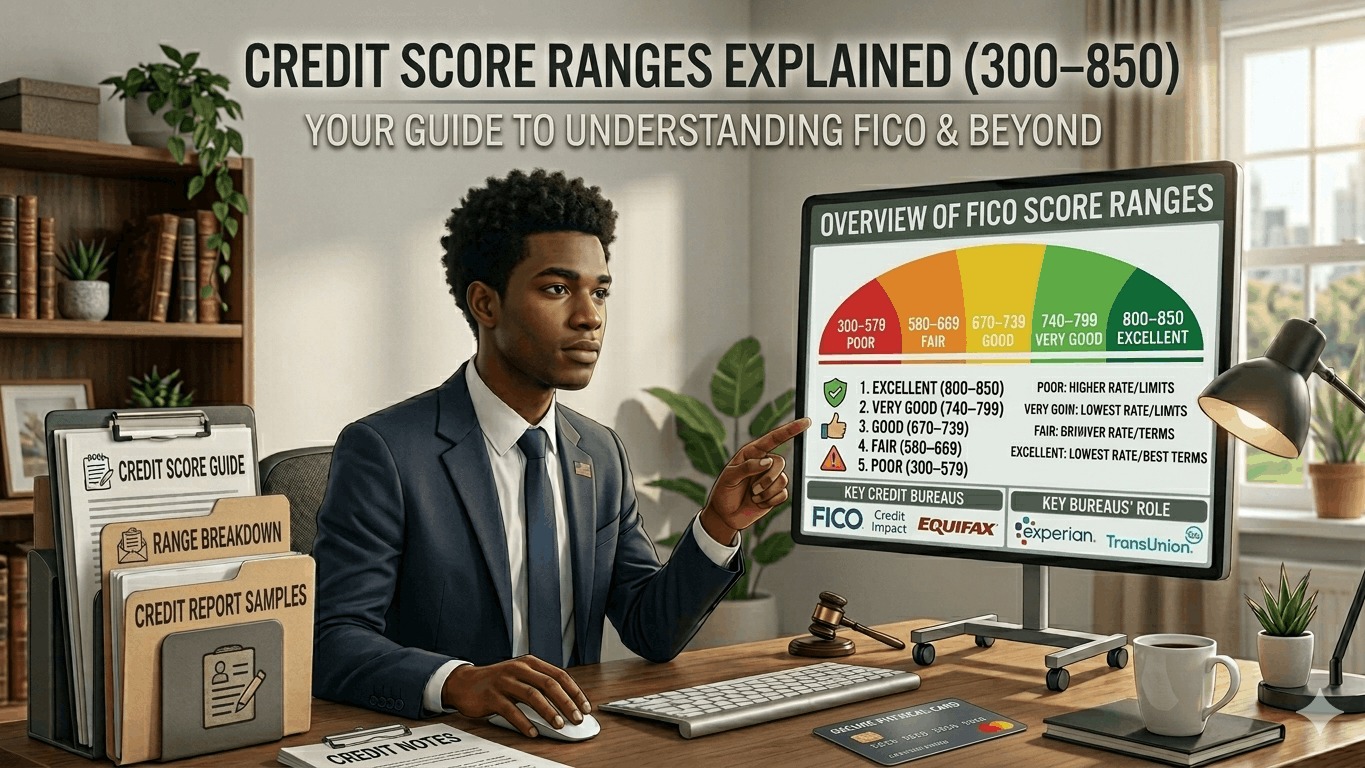

1. The FICO vs. VantageScore Tiers

In the USA, you actually have two main scores. FICO is used by 90% of top lenders (especially for mortgages), while VantageScore is common in credit card apps and personal loan platforms. They use the same 300–850 range but group the numbers differently.

FICO Score 8 & 10T Ranges

| Range | Rating | What it Means for You |

|---|---|---|

| 800 – 850 | Exceptional | You are a "top-tier" borrower; you get the lowest possible rates. |

| 740 – 799 | Very Good | You are highly likely to be approved for any premium credit card. |

| 670 – 739 | Good | The US average. You are a "prime" borrower with solid options. |

| 580 – 669 | Fair | "Near-prime." You may face higher interest rates or smaller limits. |

| 300 – 579 | Poor | You may need a "Secured" card or a co-signer to get approved. |

VantageScore 4.0 Ranges

- 781 – 850 (Superprime): Elite status; immediate approvals.

- 661 – 780 (Prime): Reliable borrower; standard competitive rates.

- 601 – 660 (Near Prime): Moderate risk; might require higher deposits.

- 300 – 600 (Subprime): High risk; likely limited to credit-builder products.

2. Why "Trended Data" Matters in 2026

In previous years, your score was a snapshot. If you maxed out a card today, your score dropped tomorrow. In 2026, the FICO 10T model looks at your behavior over the last 24 months.

- The "Ladder" Effect: If a lender sees your balances consistently decreasing every month, they may give you a better rate than someone with the same score whose balances are stagnant.

- The "Inclusion" Factor: VantageScore 4.0 now includes on-time rent and utility payments (if reported), helping millions of "thin-file" borrowers reach the "Good" range faster.

3. What Each Range Actually Costs You

Your credit score range directly dictates your "cost of living." On a $400,000 mortgage in 2026:

- 760+ Score: You might get a 6.1% APR ($2,424/month).

- 620 Score: You might get a 7.7% APR ($2,853/month).

- The Difference: Having "Fair" credit instead of "Exceptional" credit costs you $154,440 extra over 30 years.

4. How to Move Between Tiers

- To move from Poor to Fair: Open a Secured Credit Card and use the Experian Boost tool to add your phone and utility bills to your report.

- To move from Fair to Good: Focus on Utilization. Paying your balances down to under 10% of your limits can jump your score 40+ points in a single month.

- To move from Good to Exceptional: Time is your friend. This tier requires a "Credit Mix" (e.g., a card, an auto loan, and a mortgage) and a long history of on-time payments.

5. Summary: The 2026 "Magic Numbers"

- 620: The minimum for a Conventional mortgage.

- 670: The threshold to be considered "Prime."

- 740: The "Rate Ceiling"—above this, you rarely get better interest rates; you just get more "buffer" against score drops.