Borrowing money is a normal part of life for many Americans. Whether you're buying your first car, paying for college, purchasing a home, or covering an unexpected expense, choosing the right type of loan can save you thousands of dollars over time.

The problem is that there isn't just one kind of loan. Banks, credit unions, online lenders, and government programs all offer different borrowing options, each designed for a specific purpose. Understanding how these loans work helps you make smarter financial decisions and avoid paying more interest than necessary.

In this guide, we'll break down the most common types of loans in the USA using simple language, practical examples, and useful tips so you can better understand which loan fits your needs.

Why Different Types of Loans Exist

Not every financial need is the same. Buying a house is very different from paying for a medical emergency or financing a college education. Because of that, lenders create different loan products with different repayment terms, interest rates, and qualification requirements.

For example:

- A mortgage may last 30 years.

- A car loan usually lasts between 3 and 7 years.

- A personal loan often ranges from 2 to 7 years.

- Student loans may offer flexible repayment plans that extend much longer.

Choosing the correct loan helps reduce borrowing costs while making repayment more manageable.

Loan Types at a Glance

| Loan Type | Best For | Typical Repayment |

|---|---|---|

| Personal Loan | Home improvements, emergencies, debt consolidation | 2–7 years |

| Mortgage Loan | Buying a home | 15–30 years |

| Auto Loan | Purchasing a vehicle | 3–7 years |

| Student Loan | Paying education expenses | 10–25 years (varies) |

| Home Equity Loan | Borrowing against home equity | 5–30 years |

| Payday Loan | Very short-term emergencies | Usually 2–4 weeks |

| Business Loan | Starting or expanding a business | Varies by lender |

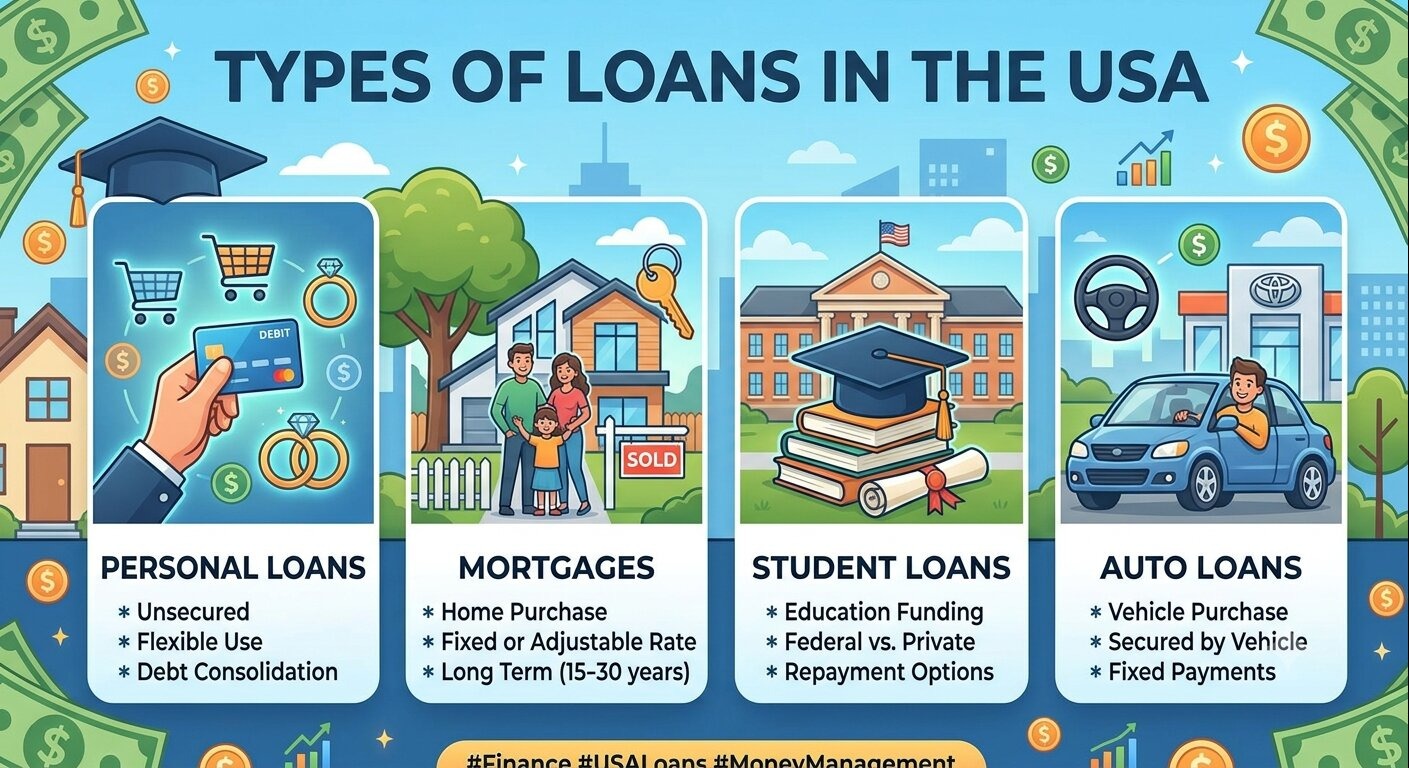

1. Personal Loans

A personal loan is one of the most flexible borrowing options available. You receive a lump sum of money and repay it in fixed monthly payments.

People commonly use personal loans for:

- Home renovations

- Medical expenses

- Weddings

- Vacations

- Debt consolidation

- Emergency expenses

Most personal loans are unsecured, meaning you don't need to pledge collateral like a house or vehicle.

If you'd like a deeper explanation, read How Personal Loans Work:

https://statush.com/credit-score-debt/how-personal-loans-work

If you're applying for your first loan, you may also enjoy Best Personal Loans for Beginners:

https://statush.com/credit-score-debt/best-personal-loans-for-beginners

2. Mortgage Loans

Mortgage loans help people purchase homes. Since homes are expensive, lenders allow borrowers to repay the loan over many years.

Common mortgage terms include:

- 15-year mortgage

- 20-year mortgage

- 30-year mortgage

Because the house serves as collateral, mortgage interest rates are generally lower than personal loan rates.

Real-world example

Sarah buys a $350,000 home. She makes a 20% down payment and finances the remaining amount through a 30-year mortgage. Instead of paying hundreds of thousands of dollars upfront, she makes affordable monthly payments over time.

3. Auto Loans

Auto loans are specifically designed to finance vehicles.

Most lenders require:

- A down payment

- Proof of income

- Credit review

The vehicle itself acts as collateral until the loan is fully repaid.

If you're deciding how to finance your next vehicle, check out:

- How Car Loans Work

https://statush.com/credit-score-debt/how-car-loans-work - Auto Loan vs Personal Loan

https://statush.com/credit-score-debt/auto-loan-vs-personal-loan

4. Student Loans

Higher education can be expensive, and student loans help students pay tuition, books, housing, and other education-related costs.

There are two major categories:

- Federal student loans

- Private student loans

Federal loans generally offer more flexible repayment options and borrower protections.

Related reading:

- How Student Loans Work in the USA

https://statush.com/credit-score-debt/how-student-loans-work-in-the-usa - Federal vs Private Student Loans

https://statush.com/credit-score-debt/federal-vs-private-student-loans

5. Home Equity Loans

Once homeowners build equity in their property, they may borrow against it.

Many people use home equity loans for:

- Major renovations

- Medical expenses

- Education

- Debt consolidation

Since the loan is secured by the home, interest rates are often lower than unsecured borrowing.

However, failing to repay could put the home at risk, so borrowers should use these loans carefully.

6. Business Loans

Business loans help entrepreneurs start, expand, or operate businesses.

They can be used for:

- Purchasing equipment

- Hiring employees

- Buying inventory

- Marketing

- Working capital

Business loans may come from banks, online lenders, or government-backed lending programs.

7. Payday Loans

Payday loans are short-term loans intended to cover emergency expenses until the borrower's next paycheck.

Although they may seem convenient, they often carry extremely high fees and interest rates.

Practical tip

If possible, consider alternatives such as:

- Personal loans

- Emergency savings

- Credit union small-dollar loans

Learn more in Payday Loans Explained (Pros and Cons):

https://statush.com/credit-score-debt/payday-loans-explained-pros-and-cons

Secured vs. Unsecured Loans

Loans generally fall into two categories.

Secured Loans

These require collateral.

Examples include:

- Mortgages

- Auto loans

- Home equity loans

Because lenders have collateral, secured loans often come with lower interest rates.

Unsecured Loans

No collateral is required.

Examples include:

- Most personal loans

- Many student loans

- Some business loans

Since lenders assume more risk, interest rates may be higher.

Read our complete comparison:

Secured vs Unsecured Loans

https://statush.com/credit-score-debt/secured-vs-unsecured-loans

What Affects Loan Approval?

Every lender evaluates borrowers differently, but common factors include:

- Credit score

- Credit history

- Income

- Employment stability

- Debt-to-income ratio

- Existing financial obligations

Improving these factors before applying can increase your approval chances and help you qualify for better interest rates.

Continue learning with:

- Loan Approval Factors Explained

https://statush.com/credit-score-debt/loan-approval-factors-explained - How Credit History Impacts Loan Approval

https://statush.com/credit-score-debt/how-credit-history-impacts-loan-approval

Practical Tips Before Borrowing

Before signing any loan agreement:

- Borrow only what you genuinely need.

- Compare multiple lenders rather than accepting the first offer.

- Read all fees, including origination charges and prepayment penalties.

- Understand whether the interest rate is fixed or variable.

- Make sure the monthly payment comfortably fits your budget.

- Avoid borrowing simply because you qualify for a larger amount.

A little research before applying can save hundreds—or even thousands—of dollars over the life of the loan.

Common Mistakes to Avoid

Many borrowers make avoidable mistakes, such as:

- Choosing a loan based only on the monthly payment.

- Ignoring the total interest paid over time.

- Missing payment due dates.

- Taking high-interest payday loans for non-emergencies.

- Borrowing more than necessary.

Being aware of these pitfalls helps you make better long-term financial decisions.

Final Thoughts

Loans can be powerful financial tools when used responsibly. The key is matching the loan to your specific need instead of choosing the first option available.

Whether you're financing a home, paying for college, purchasing a vehicle, or handling an emergency expense, understanding the differences between loan types makes borrowing less confusing and far more cost-effective.

As you continue exploring personal finance, learning about loan interest, repayment strategies, refinancing, and credit scores will help you become an even more confident borrower.