In the 2026 American credit ecosystem, your Credit Utilization Ratio has become the most dynamic and influential factor in your day-to-day credit score fluctuations. While payment history proves your reliability, utilization proves your stability.

With many U.S. lenders now using "Ultra-FICO" and VantageScore 4.0, which track "Trended Data" (your spending patterns over time rather than just a monthly snapshot), understanding this ratio is critical for anyone planning a major purchase like a home or car.

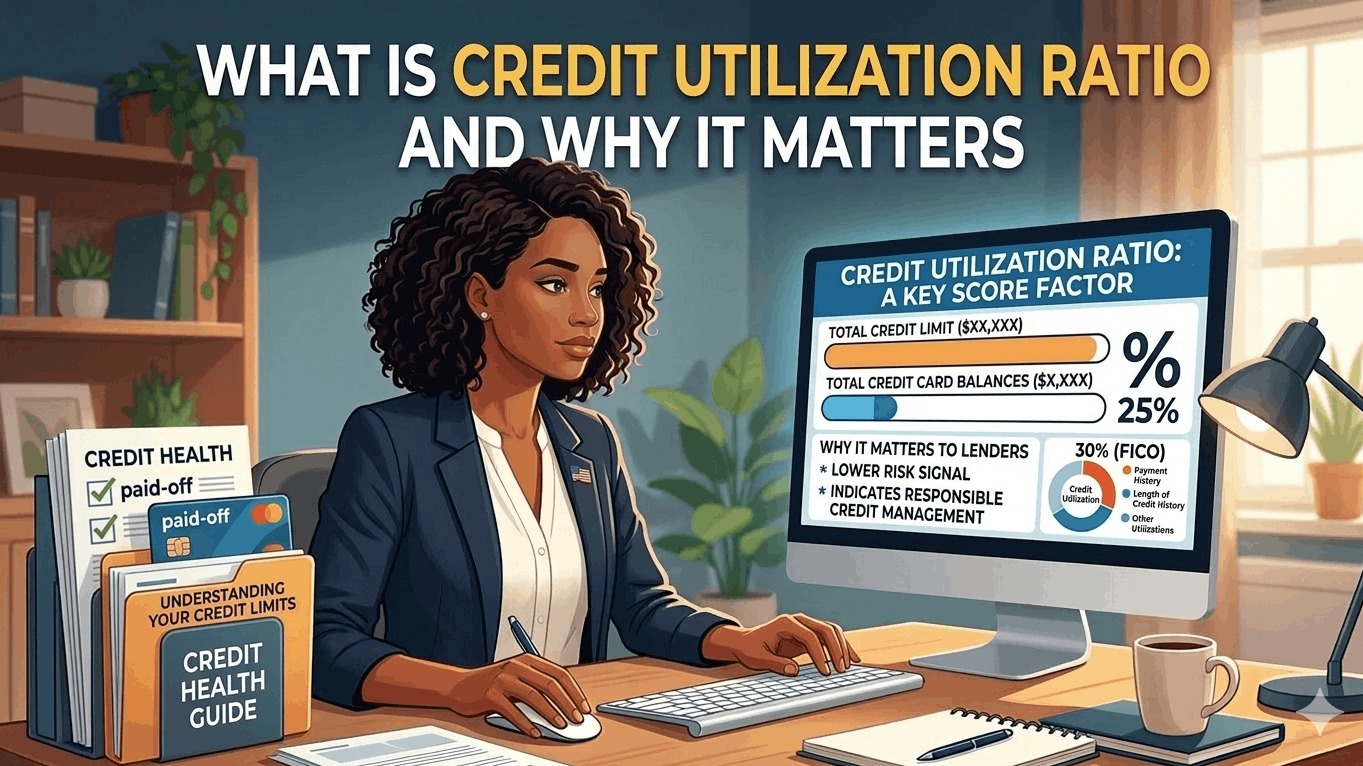

1. Defining the Ratio: The "Credit Thermometer"

Your Credit Utilization Ratio is the percentage of your total available credit that you are currently using. It is calculated both for individual cards and as a total aggregate across all your accounts.

The Formula:

Utilization Ratio = (Total Credit Card Balances / Total Credit Limits) x 100

For example, if you have one credit card with a $10,000 limit and a balance of $3,000, your utilization is 30%. If you have three cards with a combined limit of $50,000 and a total balance of $5,000, your aggregate utilization is 10%.

2. Why It Matters: The 30% Weight

In the FICO® scoring model, Amounts Owed (which is dominated by utilization) accounts for 30% of your total score. It is the second most important factor after payment history.

The "High Utilization" Red Flag

Lenders view high utilization as a sign of financial stress. If you are constantly "maxed out," the algorithm assumes you are overextended and rely too heavily on debt to cover daily expenses. This makes you a higher risk, even if you never miss a payment.

3. The "30% Rule" vs. The "10% Secret"

Common financial advice often suggests keeping your utilization below 30%. While this is a good baseline to avoid a score "crash," it is not the optimal level for a top-tier score.

- The 30% Ceiling: Crossing this threshold typically triggers a noticeable drop in your score.

- The 10% Sweet Spot: Data from 2026 shows that "Super-Prime" borrowers (those with scores above 800) typically maintain an aggregate utilization of less than 10%.

- The 0% Myth: Having 0% utilization across all cards can actually lower your score slightly compared to having a very small balance (e.g., 1%), because it looks like you aren't using your credit at all.

4. 2026 Trended Data: The End of "Score Shifting"

In the past, borrowers would "game the system" by paying off their balances right before applying for a loan to artificially boost their score.

In 2026, U.S. bureaus use Trended Data. This means they look at your utilization over the last 24 months. If you usually carry 80% utilization and suddenly pay it down to 5% one week before a mortgage application, the lender will still see your historical "high-utilization" behavior, which may affect your interest rate.

5. How to Lower Your Ratio (Without Paying Down Debt)

If you cannot immediately pay off your balances, you can improve your ratio by focusing on the "Limit" side of the equation:

- Request a Credit Limit Increase: Most U.S. banks allow you to request this via their app. If your limit goes from $5,000 to $10,000 while your balance stays the same, your utilization is instantly cut in half.

- The "AZEO" Method: (All Zero Except One). Pay off all your credit cards except for one, on which you leave a very small balance (under $50). This signals to the bureaus that you are active but extremely disciplined.

- Open a New Account: Adding a new card adds to your total available credit. However, be careful—the "Hard Inquiry" and the lower "Average Age of Accounts" might temporarily dip your score.