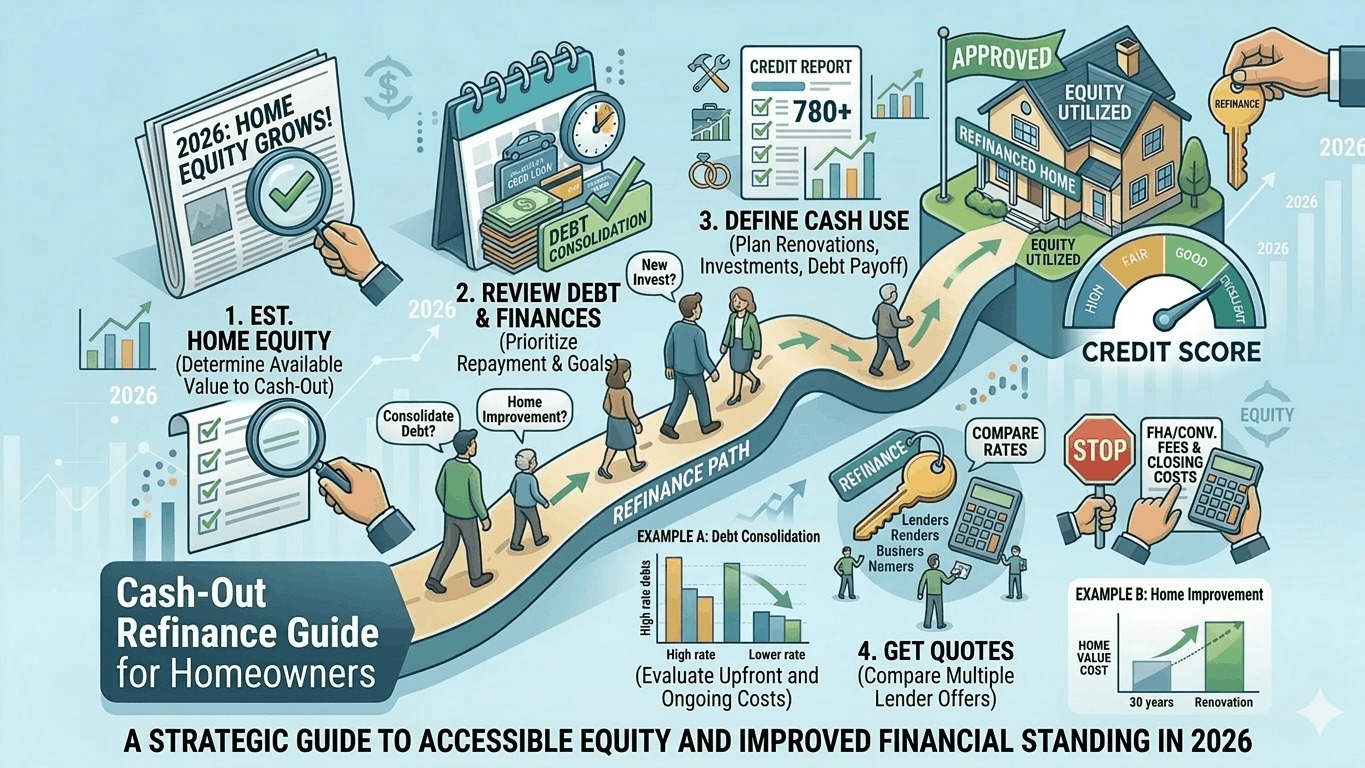

With home values in the USA reaching new highs in early 2026, many homeowners are sitting on a "gold mine" of untapped equity. A cash-out refinance allows you to replace your current mortgage with a larger one, taking the difference in tax-free cash.

Whether you're looking to consolidate high-interest debt, renovate your kitchen, or fund a major life milestone, here is exactly how a cash-out refinance works in today's market.

1. How the "Cash-Out" Math Works

Lenders generally allow you to borrow up to 80% of your home's current appraised value. This is known as the Loan-to-Value (LTV) limit.

The Calculation Example:

- Home Appraisal (2026): $500,000

- Max Loan (80% LTV): $400,000

- Current Mortgage Balance: $250,000

- Gross Cash Available: $150,000

- Net Cash: ~$138,000 (after estimated 3% closing costs)

2. 2026 Guidelines by Loan Type

Requirements vary significantly depending on which government-backed or private program you choose:

| Feature | Conventional | FHA Cash-Out | VA Cash-Out |

|---|---|---|---|

| Max LTV | 80% | 80% | 90% – 100% |

| Min. Credit Score | 620 – 660 | 580 (some 500) | 580 – 620 |

| Mortgage Insurance | None (if LTV ≤ 80%) | Mandatory (MIP) | No PMI |

| Seasoning (Wait Time) | 12 months | 12 months | 210 days / 6 payments |

3. Current 2026 Market Rates

As of March 2026, cash-out refinance rates typically carry a "premium" of 0.25% to 0.50% over standard rate-and-term refinance rates.

- National Average (30-Year Fixed Cash-Out): ~6.75% – 7.00%

- VA Cash-Out Rates: ~6.15% – 6.45%

- 15-Year Fixed Options: ~5.50% – 5.85%

4. Smart Ways to Use the Funds

In 2026, homeowners are primarily using cash-out equity for:

- High-Interest Debt Consolidation: Swapping 24% APR credit card debt for a ~6.8% mortgage rate.

- Home Appreciation Projects: Upgrading kitchens or adding ADUs (Accessory Dwelling Units) to increase property value.

- Investment Capital: Using equity as a down payment for a second property or business venture.

- Emergency Reserves: Liquidating equity to create a safety net in a fluctuating economy.