In 2026, the decision to close a credit card is more significant than ever. With lenders now heavily relying on FICO 10T and VantageScore 4.0, your "trended data" and "credit depth" are under a microscope. While closing an account might feel like "cleaning up" your finances, in the world of credit algorithms, it often triggers a red flag.

Understanding the mechanics of a closed account is the difference between maintaining a "Superprime" score and seeing an unexpected 50-point drop.

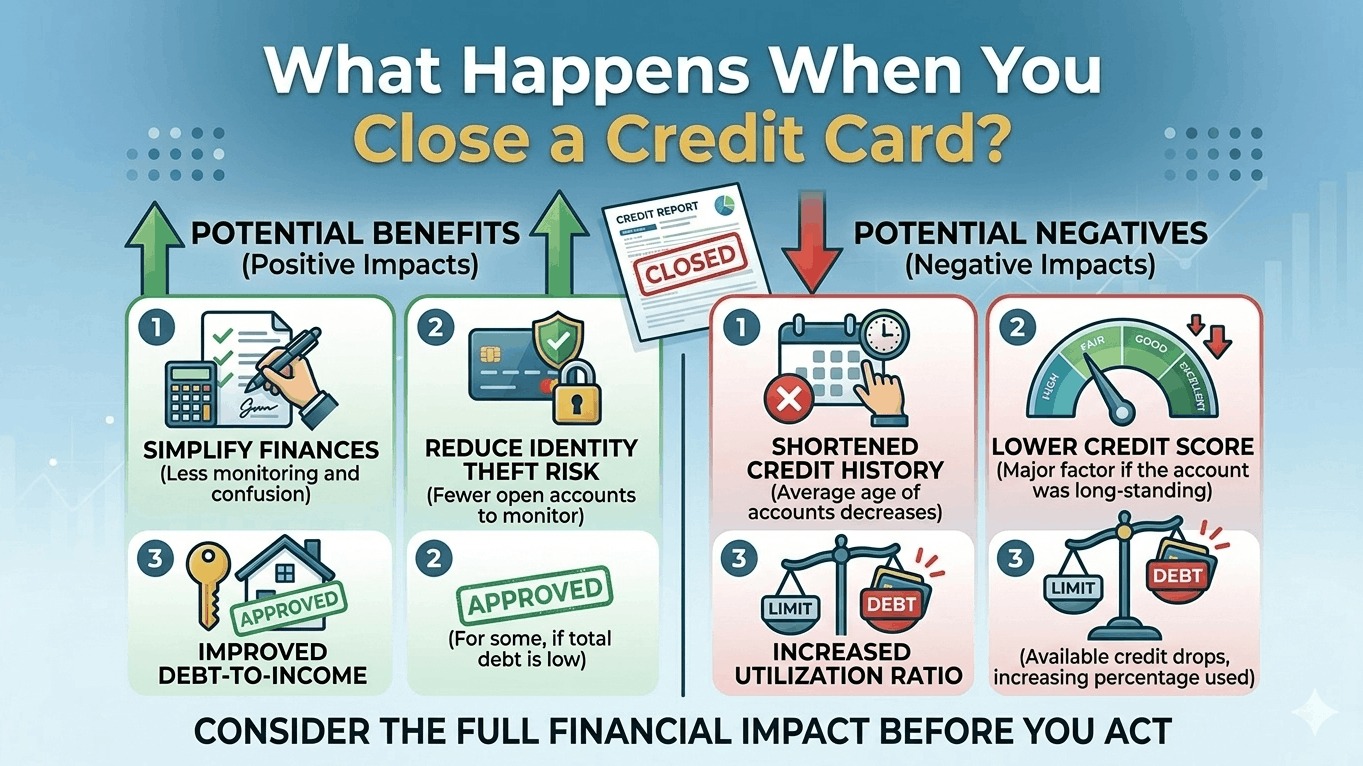

1. The "Immediate" Impact: The Utilization Spike

The most sudden change happens to your Credit Utilization Ratio (which accounts for 30% of your score).

- The Math: If you have $5,000 in debt across three cards with a total limit of $20,000, your utilization is 25% (Good). If you close a card with a $10,000 limit, your available credit drops to $10,000. Your utilization instantly jumps to 50% (High Risk).

- 2026 Shift: Under FICO 10T, this jump doesn't just hurt you for one month. The model records this "utilization spike" as a trend, which can signal to lenders that you are becoming more reliant on your remaining credit lines.

2. The "Delayed" Impact: Credit Age

A common 2026 myth is that closing a card "removes" its history immediately. This is false for FICO scores but potentially true for VantageScore.

- FICO Protocol: Accounts closed in good standing remain on your report for 10 years. They continue to age and contribute to your "Average Age of Accounts" during this decade.

- The 10-Year Cliff: The real damage happens exactly 10 years after closure. When that old account finally "falls off" your report, your average credit age will plummet, which could cause a sudden score drop years down the line.

- VantageScore Protocol: This model may stop counting a closed account toward your age immediately, leading to an instant score decrease on apps like Credit Karma.

3. The 2026 "Keep vs. Close" Checklist

Before you close a card in 2026, ask these three questions:

| Feature | Keep the Card If... | Close the Card If... |

|---|---|---|

| Annual Fee | There is no fee, or rewards outweigh it. | The fee is high and you don't use the perks. |

| Credit Age | It is your oldest or second-oldest card. | It is a "new" card you've had for <1 year. |

| Spending Habit | You can manage the temptation to spend. | The card is a trigger for impulsive debt. |

4. Better Alternatives to Closing

If you want to get rid of a card but protect your score, try these 2026 strategies:

- The "Product Change": Instead of closing a high-fee card, ask the bank to "downgrade" it to a no-annual-fee version. This keeps the account number, the credit limit, and the entire age history intact.

- The "Sock Drawer" Method: If there is no fee, just stop using it. Charge a small $5 subscription to it once every six months to prevent the bank from closing it for inactivity.

- The "Limit Shift": If you have two cards with the same bank (e.g., Chase), you can often ask them to move the credit limit from the card you want to close to the card you want to keep. This prevents your total utilization from spiking.

5. If You Must Close: The Safe Shutdown Process

- Pay it to $0: Ensure there are no "pending" transactions or interest charges.

- Redeem Rewards: Most banks wipe out your points/cash-back the moment the account is closed.

- Notify the Bank: Call or use the secure chat to request the account be "Closed at Customer Request."

- Download Statements: You may lose access to your online portal immediately; save your last 12 months of PDFs for your records.