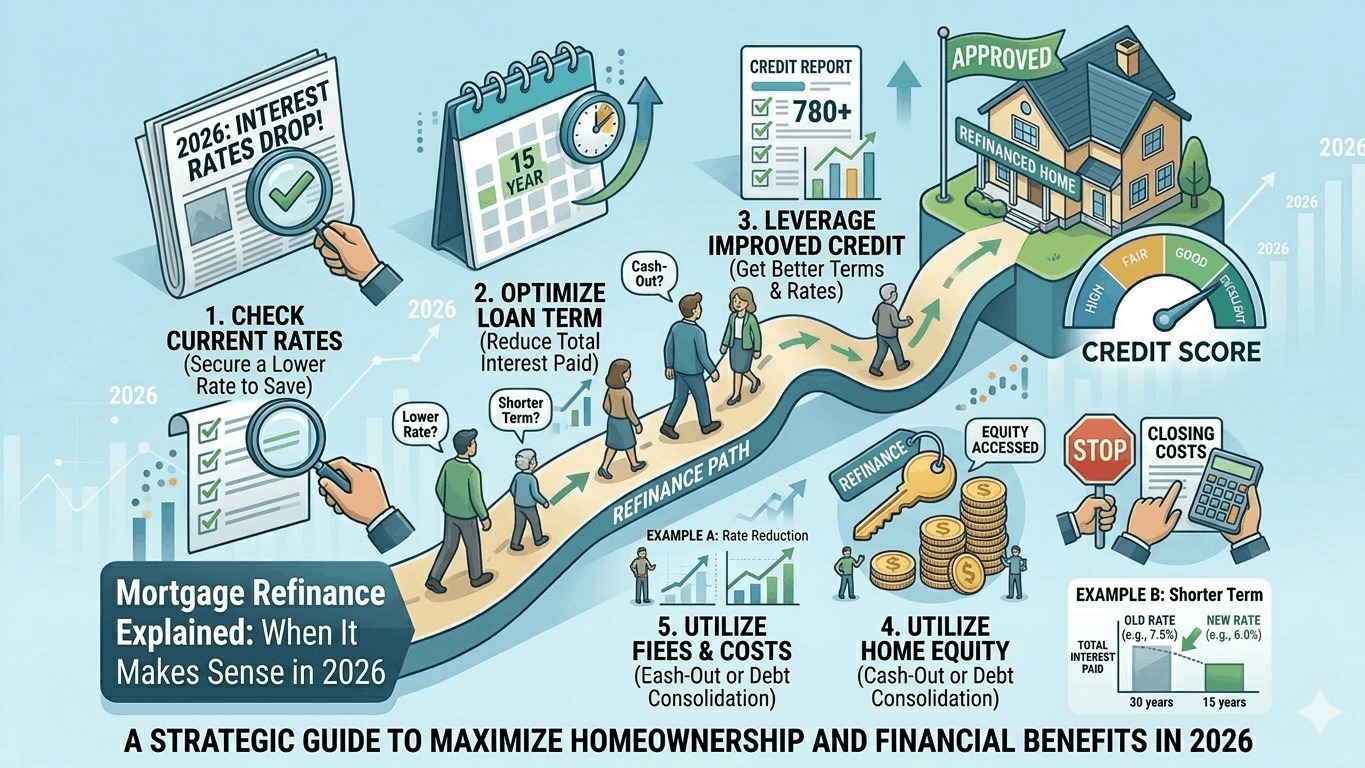

In the first quarter of 2026, the "refinance wave" has officially returned to the USA. After years of record-high rates, the market has settled into a "new normal," with 30-year fixed rates hovering between 6.1% and 6.7%.

Refinancing is the process of replacing your current mortgage with a new one, typically to secure a lower interest rate, change your loan term, or tap into your home's equity. However, because refinancing carries closing costs, it is a math problem that requires a clear "break-even" analysis.

1. Types of Refinancing in 2026

A. Rate-and-Term Refinance

This is the most common "vanilla" refinance. You swap your old loan for a new one with a better interest rate or a different length (e.g., switching from a 30-year to a 15-year mortgage).

- Goal: Lower monthly payments or pay off the house faster.

B. Cash-Out Refinance

If your home has gained value, a cash-out refinance allows you to take out a loan for more than you owe and pocket the difference in cash. In 2026, lenders typically allow you to take out up to 80% of your home's appraised value.

- Goal: Funding home improvements, consolidating high-interest debt, or paying for education.

C. Cash-In Refinance

The opposite of a cash-out. You bring a lump sum of cash to the closing table to pay down your principal.

- Goal: Lowering your LTV (Loan-to-Value) to remove PMI or qualify for a much lower interest rate.

2. When Does Refinancing Make Sense?

Refinancing isn't just about the rate—it's about the Break-Even Point. This is the moment when your monthly savings finally surpass the cost of getting the loan.

The "Rule of Thumb" vs. The Math

Historically, people said to refinance if rates dropped by 1.0%. In 2026, with higher home balances, even a 0.50% to 0.75% drop can save enough to justify the costs.

How to Calculate Your Break-Even Point:

Formula: Total Closing Costs ÷ Monthly Savings = Months to Break Even

Example: * Closing Costs: $6,000

- Monthly Savings: $250

- Calculation: $6,000 / $250 = 24 Months

- Verdict: If you plan to stay in the home for more than 2 years, the refinance makes sense.

3. The Costs of Refinancing

Refinancing is not free. Expect to pay between 2% and 5% of the loan amount in fees. Typical 2026 costs include:

- Application/Origination Fees: 0.5% – 1.5% of loan.

- Appraisal Fee: $500 – $800.

- Title Search & Insurance: $700 – $1,500.

- Credit Report Fee: $50 – $100.