You can learn how the stock market works without jargon or guesswork, and this post will walk you through the essentials so you can make informed choices. The stock market is a system where companies sell ownership pieces (stocks) and investors buy and sell those pieces, letting you share in company profits and price movements.

You’ll get clear explanations of what stocks are, who moves the market, how trades happen, and the basic terms and strategies that matter. Expect practical steps for buying and selling, an overview of risks and rewards, and resources to build your knowledge and confidence.

Follow along to understand price drivers, different market venues, and simple ways to start investing that match your goals and risk tolerance.

What Is the Stock Market?

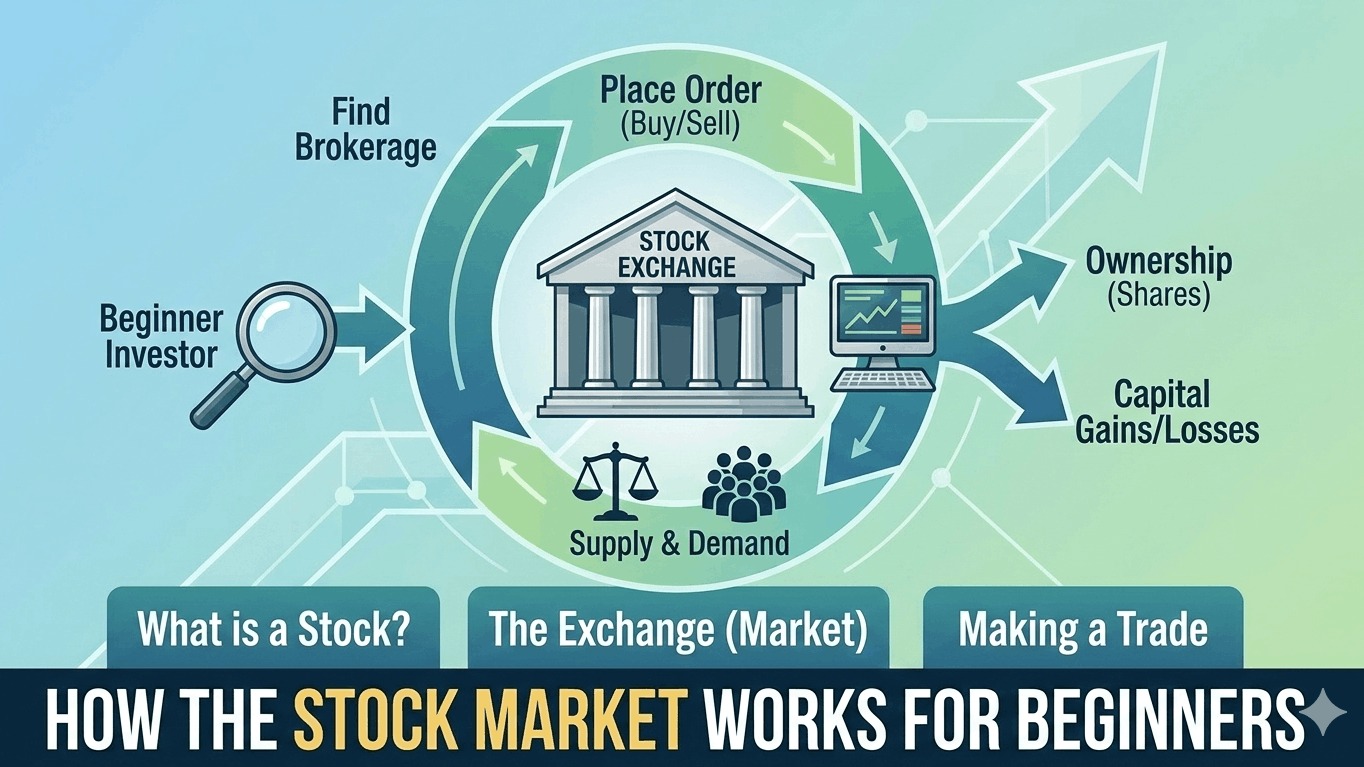

The stock market is a public place where investors buy and sell ownership stakes in companies, price discovery happens continuously, and capital flows from savers to businesses.

It connects companies that need money with people who want returns, and it sets prices based on supply and demand.

How Stock Exchanges Operate

Exchanges provide the infrastructure for trades, matching buyers and sellers either electronically or through market makers. You place orders through a broker, which routes them to an exchange or alternative trading venue where the trade executes.

Pricing results from continuous auction mechanics: bids (buy offers) and asks (sell offers) create an order book; transactions typically execute at the best available price. Liquidity—how easily you can buy or sell without drastically moving the price—depends on trading volume and the number of market participants.

Exchanges also enforce listing standards, maintain trading hours, publish real-time data, and clear and settle trades. Clearinghouses step in after a trade to guarantee settlement, reducing counterparty risk for you and other investors.

Types of Securities Traded

Stocks (equities) represent ownership in a company and come as common or preferred shares; common shareholders usually vote and share in capital gains, while preferred holders get priority on dividends. You buy stocks primarily for capital appreciation and dividend income.

Bonds are loans you make to governments or companies in exchange for fixed interest payments and principal repayment at maturity. They provide steady income and tend to be less volatile than stocks.

Exchange-traded funds (ETFs) and mutual funds pool many securities, giving you instant diversification. Derivatives—options and futures—derive value from underlying assets and let you hedge or speculate, but they carry higher complexity and risk. Other instruments include real estate investment trusts (REITs) and commercial paper, each serving different investment goals and risk profiles.

Market Capitalization

Market capitalization (market cap) equals share price × shares outstanding and measures a company’s public market value.

It classifies companies into large-cap, mid-cap, and small-cap, which helps you gauge typical growth potential and risk.

- Large-cap (e.g., over $10 billion): generally more stable, dividend-paying, and less volatile.

- Mid-cap ($2–10 billion): a balance of growth and stability.

- Small-cap (under $2 billion): higher growth potential but greater risk and price swings.

Market cap informs index inclusion and passive fund exposure, which affects liquidity and investor attention.

Remember that market cap changes with price; it does not reflect debt, cash reserves, or intrinsic valuation metrics like enterprise value or price-to-earnings ratio.

Investors and Traders

You choose between investing and trading based on time horizon and risk tolerance. Investors typically buy and hold shares to capture dividends and long-term growth; traders seek shorter-term gains by exploiting price moves.

Retail investors use online platforms and often buy fractional shares or exchange-traded funds (ETFs). Institutional investors — pension funds, mutual funds, hedge funds — execute large orders that can move markets and often use research teams and algorithmic strategies.

Traders include day traders, swing traders, and momentum players who focus on technicals, news, or event-driven catalysts. Both investors and traders must manage risk with position sizing, stop orders, and diversification to avoid outsized losses.

Brokers and Brokerage Firms

You need a broker to place orders on your behalf and access exchanges. Brokers route your buy and sell orders, offer order types (market, limit, stop), and provide execution and custody of your shares.

Full-service brokerages add research, advice, and wealth management for higher fees. Discount and online brokers give lower commissions and tools for self-directed trading. Some brokers act as market makers, internalizing order flow, which can affect execution quality and price improvement.

Review execution speed, commissions, margin rates, account types, and protection measures such as SIPC insurance. Check order routing policies and trade confirmations so you understand how your orders are handled and priced.

Types of Stock Markets

You will encounter two main ways stocks change hands: where companies sell new shares to raise capital, and where investors trade already-issued shares. Each operates under different rules, participants, and risks.

Primary Market

The primary market is where a company issues new shares directly to investors to raise cash. You’ll see initial public offerings (IPOs) and follow-on offerings here. In an IPO, the company, with underwriters, sets an offering price, files required disclosures, and sells shares to institutional and retail buyers.

Buying in the primary market usually means you become a shareholder at the offering price. Companies use proceeds for expansion, debt repayment, or acquisitions. You should check the prospectus for use of proceeds, dilution effects, lock-up periods, and underwriting fees.

Key points to review before participating:

- Prospectus: financials, risks, use of proceeds.

- Underwriting: who sets price and allocation.

- Lock-up: restrictions on insider sales.

- Dilution: how new shares affect existing ownership.

Secondary Market

The secondary market is where investors buy and sell existing shares after issuance. Most trading happens on exchanges (NYSE, Nasdaq) or over-the-counter venues. Prices move continuously based on supply and demand, company news, macro data, and investor sentiment.

You trade through brokers who route orders to exchanges or market makers. Settlement and clearing happen behind the scenes; you focus on order type (market, limit, stop) and liquidity. For your risk management, watch bid-ask spreads, trading volume, and volatility. Fees, taxes, and timing influence net returns more than small price differences.

Common trading considerations:

- Order types: control execution price and timing.

- Liquidity: affects ease of buying/selling and spreads.

- Market hours: regular vs. pre/post-market sessions.

- Costs: commissions, spreads, and short-term tax implications.

Basic Stock Market Terms

You will learn specific trading language that affects price execution, market direction, and income from shares. Knowing these terms helps you place orders, read market sentiment, and expect cash flow from holdings.

Bid and Ask

The bid is the highest price buyers are willing to pay for a share; the ask (or offer) is the lowest price sellers accept. The difference between them—the bid-ask spread—represents transaction friction and can widen for thinly traded or volatile stocks.

If you place a market order, your trade executes at the best available ask (if buying) or bid (if selling). That makes market orders fast but exposes you to unfavorable fills when spreads are wide.

Use limit orders to control execution price: a buy limit sets the maximum you pay; a sell limit sets the minimum you accept.

Keep an eye on real-time quotes and depth (level 2) if you trade actively; visible bids and asks reveal short-term supply and demand and help you judge likely execution and potential slippage.

Bull and Bear Markets

A bull market describes prolonged rising prices and positive investor sentiment, often tied to economic growth, improving corporate earnings, and low unemployment. You may see higher valuations, more IPOs, and momentum-driven buying during bulls.

A bear market means prolonged price declines—typically a 20% drop from recent highs—and signals pessimism, weaker earnings, or economic contraction. Volatility and defensive sector strength (utilities, consumer staples) are common in bears.

You can adjust strategies based on the cycle: favor growth or cyclical stocks in bulls and consider value, dividend payers, or hedges in bears.

Monitor indicators like moving averages, market breadth, and macro data to identify shifts rather than reacting to single-day moves.

Dividends

A dividend is a cash (or sometimes stock) payment a company distributes to shareholders from profits or retained earnings. Companies announce a declaration date, an ex-dividend date (you must own shares before this date to receive the next payout), and a payment date when cash is disbursed.

Dividend yield equals annual dividends divided by current share price; use it to compare income potential across stocks, but check payout ratio to assess sustainability.

Dividend-paying companies often include mature firms in utilities, consumer staples, and financials.

Reinvest dividends through a DRIP (dividend reinvestment plan) to compound returns, or take them as cash for income; choose based on your goals and tax considerations.

How to Buy and Sell Stocks

You choose a broker, place orders, and select the right order type to execute trades at prices and times that match your goals. Each step affects cost, speed, and the likelihood your trade fills.

Opening a Brokerage Account

Pick a brokerage that fits your goals: low commissions for frequent trading, robust research for stock picking, or fractional shares for small balances. Compare fees (commissions, SEC fees, margin rates), account types (individual taxable, Roth IRA, traditional IRA), and minimum deposit requirements before you sign up.

Prepare these documents: government ID, Social Security number (or tax ID), employment info, and bank routing/account numbers for funding. Expect an electronic identity check and possibly a short wait for account verification; transfers from another broker can take 3–7 business days.

Review platform features: mobile app quality, order execution speed, research tools, and customer service availability. If you plan to trade on margin or options, complete and understand the broker's margin agreement and risk disclosures.

Placing Orders

Log into your brokerage platform and navigate to the trade ticket for the stock ticker symbol you want. Choose buy or sell, enter the number of shares or dollar amount (if fractional shares are supported), and pick an order type that matches your intent.

Set order duration: “day” orders expire at market close if not filled, while “GTC” (good-till-canceled) orders remain active until you cancel or the broker's time limit. Review estimated fees and trading costs before submitting.

Monitor your order status after submission so you can cancel or modify if conditions change. Use limit or stop orders when you need price control; use market orders only when execution speed matters more than exact price.

Stock Market Orders Types

Market order: executes immediately at the best available price. Use it when you prioritize speed and the stock is liquid, but expect price slippage in fast-moving or thinly traded names.

Limit order: sets a maximum buy price or minimum sell price. The order fills only at your price or better. Use limits to control cost, but recognize the risk it may not fill.

Stop order (stop-loss): becomes a market order once the stop price triggers. Use it to limit losses or protect gains, but beware of gaps that can trigger execution far from the stop.

Stop-limit order: triggers a limit order at the stop price. It prevents unwanted prices after a trigger but can fail to execute if the limit is missed.

Additional types to consider:

- Trailing stop: moves the stop price with favorable price movement to lock in gains.

- Fill-or-kill (FOK): executes immediately in full or cancels.

- Immediate-or-cancel (IOC): fills any available portion immediately and cancels the rest.

Choose order types that match your risk tolerance and trading objectives to control price exposure and execution certainty.

Factors That Influence Stock Prices

Stock prices move because measurable data, company results, and investor behavior change the balance of buyers and sellers. Expect macro numbers, firm-specific reports, and shifts in market mood to drive most short- and medium-term price moves.

Economic Indicators

Economic indicators give you a snapshot of demand, inflation, and growth that affect corporate profits and interest rates. Key reports include GDP growth, CPI inflation, unemployment figures, and central bank policy statements. Rising GDP and falling unemployment generally support higher earnings expectations, which can lift stock prices. Conversely, accelerating inflation often pushes central banks to raise rates, increasing borrowing costs and pressuring equity valuations.

Look at yield curves and interest-rate expectations, too. A rising yield on government bonds can make stocks less attractive relative to fixed income, prompting rotation out of equities. Pay attention to sector sensitivity: consumer discretionary stocks react strongly to retail sales, while industrials track manufacturing PMIs.

Company Performance

Company performance ties directly to a stock's intrinsic value because it determines future cash flows. Monitor quarterly earnings, revenue trends, profit margins, free cash flow, and guidance. Be especially alert to changes in management commentary, margin compression, or one-time charges—those often trigger sharp price moves.

Use key metrics to compare peers: earnings per share (EPS) growth, return on equity (ROE), and debt-to-equity ratio. Watch for catalysts such as product launches, mergers and acquisitions, regulatory approvals, or contract wins. These events can materially alter expected cash flows and reprice the stock quickly.

Market Sentiment

Market sentiment captures the collective expectations and risk appetite of investors and traders. You can gauge sentiment through indicators like the VIX (fear index), put/call ratios, fund flow data, and news volume. Positive sentiment amplifies rallies; negative sentiment deepens sell-offs.

Behavioral factors matter: herd behavior, momentum trading, and headline-driven swings can move prices independently of fundamentals. Short-term spikes often reflect sentiment rather than long-term value, so differentiate between noise and signal. Combine sentiment measures with fundamentals to time entries and manage risk effectively.

Risks and Rewards of Stock Market Investing

You can gain substantial long-term returns, but you also face the chance of significant losses and short-term swings. Balancing growth potential with volatility through specific risk-management steps matters for most investors.

Potential for Growth

Stocks offer ownership in companies, which lets you capture profits when those companies grow. If a company increases earnings or expands its market share, its stock price can rise, producing capital gains. You can also receive dividends, which pay part of a company’s profits directly to shareholders.

Growth tends to compound over years. For example, broad U.S. stock indexes have averaged high single-digit to low double-digit annual returns historically, but individual stocks can outperform or underperform that average. Picking individual winners increases potential reward but requires research, time, and tolerance for ups and downs.

Market Volatility

Prices move every trading day based on news, earnings, economic data, and investor sentiment. Short-term volatility can stem from geopolitical events, interest-rate shifts, or company-specific problems like missed guidance. You should expect intraday swings and occasional large drops.

Volatility can erase value quickly; a 30% drop requires a ~43% gain to recover. If you need money soon, market downturns can force selling at a loss. If you have a multi-year horizon, you can often ride out volatility, but you must decide your time frame and emotional tolerance before investing.

Risk Management Strategies

Use diversification to reduce single-stock or sector-specific risk. Hold a mix of stocks across industries and market caps, and consider index funds or ETFs for instant broad exposure. Diversification won’t eliminate market risk, but it lowers the chance one event destroys your portfolio.

Set an asset allocation aligned with your time horizon and risk tolerance, then rebalance annually to maintain that mix. Use position sizing limits (for example, no more than 5% of your portfolio in one stock). Consider stop-loss orders and tax-aware harvesting, and increase cash or bonds as you near spending needs to preserve capital.

Common Investment Strategies

These strategies balance risk, time horizon, and effort. You’ll see approaches that focus on holding for growth, active buying and selling, and spreading risk across assets.

Long-Term Investing

Long-term investing means buying assets you expect to hold for years or decades, typically aiming for compound growth. You’ll favor broad index funds, ETFs, or high-quality individual stocks with consistent earnings, dividend histories, and competitive advantages.

Focus on low-cost funds to minimize fees that erode returns over decades. Use tax-advantaged accounts (IRAs, 401(k)s) when available to improve after-tax outcomes. Rebalance annually or semiannually to keep your target allocation—don’t react to every market swing.

Monitor fundamentals: revenue growth, profit margins, debt levels, and management quality. Dollar-cost averaging helps you invest steadily and reduce timing risk, especially if you add cash monthly or quarterly.

Short-Term Trading

Short-term trading covers holding periods from intraday to several months and relies on price movements rather than long-run fundamentals. You’ll use technical analysis, chart patterns, volume, and indicators like moving averages or RSI to time entries and exits.

Manage risk tightly: set stop losses, position-size rules (e.g., risk 1% of capital per trade), and define profit targets before entering. Trading demands discipline, fast execution, and attention to fees and taxes—short-term gains may face higher tax rates.

Start with a clear plan: strategy rules, watchlist, and a journal to record trades and outcomes. Backtest ideas on historical data before risking real capital and use a small portion of your portfolio for active trading if you also pursue long-term investing.

Diversification

Diversification reduces single-asset risk by spreading capital across uncorrelated holdings so one loss won’t derail your goals. You’ll diversify across asset classes (stocks, bonds, cash), sectors (technology, healthcare, consumer), geographic regions, and styles (growth vs. value).

Use simple tools: target-date funds or multi-asset ETFs if you prefer a hands-off approach. For more control, build an allocation (e.g., 60% stocks / 40% bonds) that matches your risk tolerance, then rebalance to maintain it.

Avoid over-diversifying into tiny positions that are hard to manage. Periodically review correlations—assets that once diversified well can converge in crises—so you adjust allocations based on changing market relationships.

Getting Started as a Beginner

Decide what you want to achieve with specific timeframes, learn how to evaluate companies and funds, and assemble a mix of investments that matches your goals and risk tolerance.

Setting Financial Goals

Write down clear, measurable goals with deadlines. Example: “Save $20,000 for a house down payment in 5 years” versus “grow retirement savings.” Assign each goal a priority and an approximate target date.

Calculate how much you must invest monthly to reach a goal. Use a conservative expected return (for example, 5–7% real return for a long-term, diversified stock portfolio) to estimate required contributions. Factor in emergency savings—keep 3–6 months of living expenses in cash before investing money you might need soon.

Decide on time horizon and risk tolerance for each goal. Short-term goals (under 3 years) favor low-volatility investments; long-term goals (10+ years) can accept more stock exposure. Record your risk preferences and revisit them annually or after major life events.

Researching Stocks

Start with company fundamentals: revenue growth, profit margins, cash flow, and debt levels. Use annual reports (10-K), quarterly filings (10-Q), and earnings calls to confirm trends rather than relying on headlines.

Compare valuation metrics to industry peers: price-to-earnings (P/E), price-to-sales (P/S), and enterprise value-to-EBITDA (EV/EBITDA). Look for consistency between growth expectations and the price you pay. Beware of one-off spikes in earnings or revenue.

Assess competitive advantages and management quality. Search for durable moats—brand, network effects, cost advantages—and read manager biographies and shareholder letters. For ETFs and mutual funds, evaluate expense ratios, tracking error, and underlying holdings.

Building a Portfolio

Choose a core allocation between stocks and bonds according to your goals and risk profile. Example allocation method: (100 − your age) = approximate equity percentage, then adjust for comfort. Rebalance at set intervals (quarterly or annually) or when allocations drift by a preset threshold (e.g., ±5%).

Diversify across sectors, geographies, and market caps to reduce company-specific risk. Hold a mix of broad-market index ETFs (domestic and international) and a few high-conviction individual stocks only if you understand them. Limit single-stock exposure to a small percentage (e.g., 2–5% of portfolio) unless you have strong reasons.

Control costs and taxes: prefer low-cost index funds for core holdings, use tax-advantaged accounts (IRA, 401(k)) when possible, and harvest tax losses to offset gains. Keep a written plan for contributions, rebalancing, and criteria for selling to avoid emotional decisions.

Resources for Learning More

Start with reputable beginner guides and official sites. Investor.gov and educational pages from established financial publishers explain basics like how stocks trade, types of accounts, and common fees.

Use books and courses to build structured knowledge. Look for beginner-friendly titles on investing fundamentals and online courses that cover diversification, risk, and long-term strategies.

Track markets and practice with low-stakes tools. Many brokerages offer simulated trading (paper trading) and free market data so you can learn without risking real money.

Follow a mix of ongoing resources to stay informed:

- News outlets for market developments.

- Financial blogs and tutorials for how-to guides.

- Podcasts and videos for concise explanations and interviews.

Consider these learning goals as you explore:

- Understand order types, spreads, and commissions.

- Learn to read financial statements and basic ratios.

- Practice constructing a simple diversified portfolio.

Quick checklist to evaluate resources:

| Resource type | What to expect | How it helps you |

|---|---|---|

| Official/Regulatory sites | Clear, unbiased rules | Learn fees, protections, account types |

| Books/Courses | Structured lessons | Build foundational knowledge |

| Simulators/Tools | Realistic practice | Test strategies without risk |

| News/Analysis | Timely insights | See how events affect markets |

Keep learning regularly and verify facts across multiple reputable sources before making investment decisions.