Student loan debt has become one of the defining financial challenges for millions of Americans. For many, it represents an investment in education and future income—but it also creates long-term financial pressure that can affect nearly every aspect of life.

Understanding student loan debt statistics helps you see the bigger picture: how much people owe, how it varies across age groups, and how it impacts financial decisions like saving, investing, and buying a home.

What Is Student Loan Debt?

Student loan debt is money borrowed to pay for education expenses such as tuition, housing, books, and other related costs.

These loans typically fall into two categories:

- Federal student loans (issued by the government)

- Private student loans (issued by banks or lenders)

Unlike many other types of debt, student loans often cannot be easily discharged and may take years—or even decades—to repay.

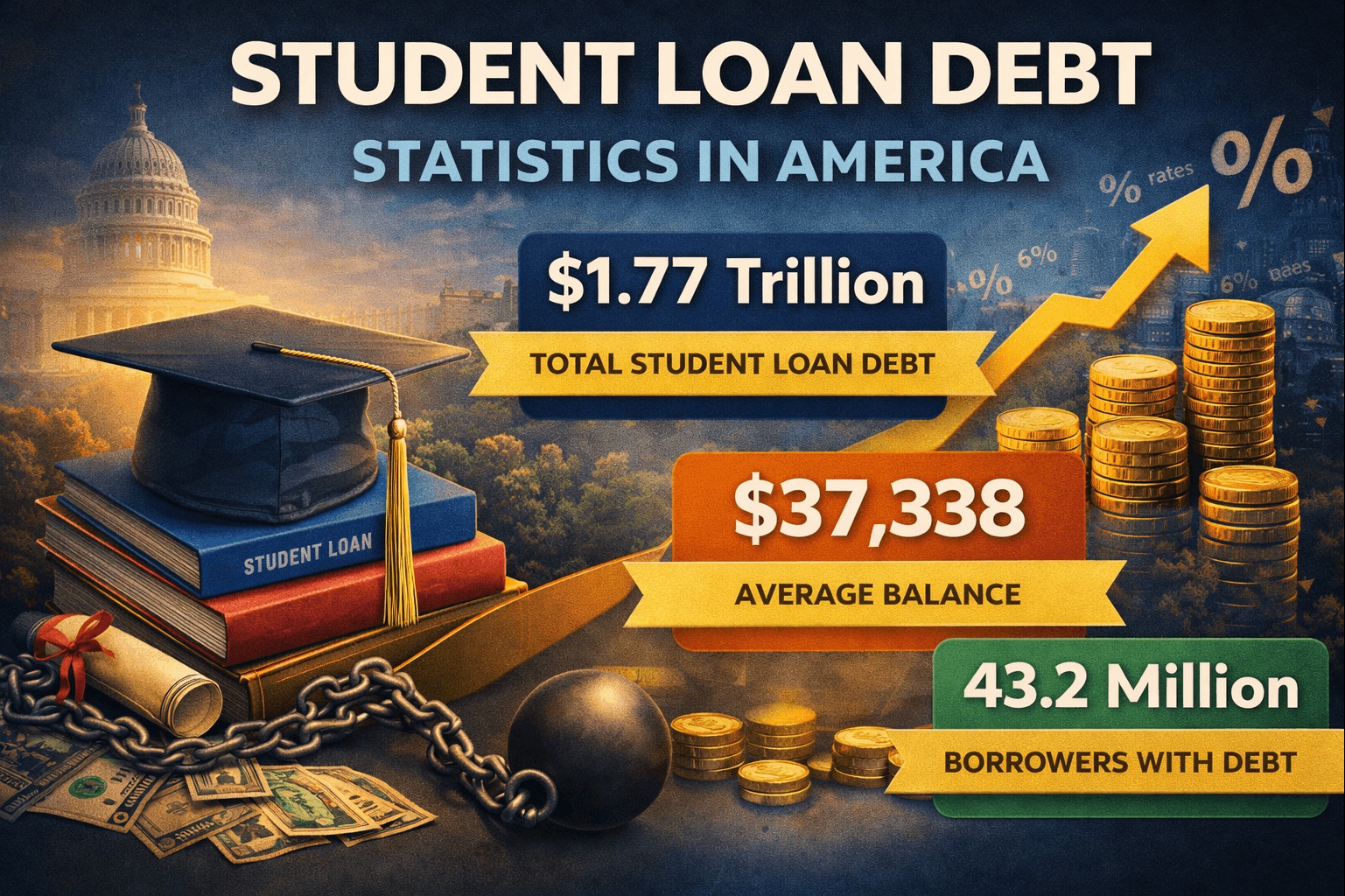

The Big Picture: Student Loan Debt in the USA

Student loan debt in the United States has grown significantly over the past few decades.

Today:

- Total student loan debt exceeds trillions of dollars

- Millions of borrowers carry outstanding balances

- Average debt per borrower continues to rise

This growth reflects increasing education costs and greater reliance on borrowing to fund college.

Average Student Loan Debt by Age

Student loan debt doesn’t disappear quickly. Many borrowers carry it well into adulthood.

| Age Group | Debt Pattern | Explanation |

|---|---|---|

| 18–24 | Rapid increase | Borrowing begins during college |

| 25–34 | Highest balances | Early career, repayment just starting |

| 35–49 | Gradual decline | Ongoing repayment, but still significant |

| 50+ | Lower but persistent | Long-term borrowers, delayed repayment |

Why Student Loan Debt Has Increased

The rise in student loan debt is not random—it’s driven by several key factors.

Rising Cost of Education

College tuition has increased significantly over time, making it harder for families to pay out of pocket.

Greater Access to Loans

Student loans are relatively accessible, allowing more people to pursue higher education—but also increasing total debt levels.

Longer Repayment Periods

Many borrowers take years to repay loans, especially if they have large balances or lower starting salaries.

Real-World Example

Let’s consider a typical borrower:

- Loan amount: $30,000

- Interest rate: 5%

- Monthly payment: around $300

Over 10 years:

- Total repayment: over $36,000

This shows how interest increases the total cost of borrowing.

Student Loan Debt vs Other Debt Types

Student loan debt is different from other types of debt in several ways.

| Debt Type | Interest Level | Flexibility |

|---|---|---|

| Student Loans | Moderate | Long repayment terms |

| Credit Card Debt | High | Short-term, high cost |

| Mortgage | Low | Long-term, asset-backed |

While student loans typically have lower interest than credit cards, they can still create long-term financial pressure.

Impact on Financial Life

Student loan debt affects more than just monthly payments—it influences major life decisions.

Many borrowers delay:

- Buying a home

- Starting a business

- Saving for retirement

This ripple effect can slow overall wealth building.

To understand how finances grow over time:

How Taxes Impact Wealth Building – https://statush.com/finance-statistics/how-taxes-impact-wealth-building

The Connection Between Income and Debt

Not all borrowers experience student debt the same way.

Those with higher-paying jobs may repay loans faster, while others may struggle with long repayment periods.

Example

- Borrower A earns $80,000 → pays off loans quickly

- Borrower B earns $40,000 → takes much longer to repay

This difference highlights how income plays a major role in debt management.

Repayment Trends in America

Borrowers typically fall into a few categories:

- Those who repay loans quickly

- Those who follow long-term repayment plans

- Those who struggle and fall behind

Understanding these patterns helps explain why student loan debt remains a widespread issue.

Common Challenges Borrowers Face

Many people face similar obstacles when dealing with student loan debt.

These include:

- High monthly payments

- Accumulating interest

- Limited financial flexibility

- Difficulty saving or investing

These challenges often overlap, making debt harder to manage over time.

Strategies to Manage Student Loan Debt

Managing student loans requires planning and consistency.

Focus on Regular Payments

Making consistent payments helps reduce both principal and interest over time.

Pay More When Possible

Extra payments can shorten repayment time and reduce total interest.

Choose the Right Repayment Plan

Different plans offer flexibility based on income and financial situation.

Avoid Missing Payments

Late payments can lead to penalties and negatively affect your financial standing.

Using Tools to Plan Repayment

Understanding your repayment strategy becomes easier with financial tools.

- Student Loan Calculator – https://statush.com/student-loan-calculator

- Debt Payoff Calculator – https://statush.com/debt-payoff-calculator

- Savings Goal Calculator – https://statush.com/savings-goal-calculator

These tools help you visualize how long repayment will take and how to optimize your plan.

Long-Term Perspective

Student loan debt is often a long-term commitment, but it doesn’t have to define your financial future.

With the right approach, you can:

- Manage payments effectively

- Build savings alongside repayment

- Gradually reduce financial pressure

The key is balancing debt repayment with long-term financial goals.

Final Thoughts

Student loan debt statistics in America reveal a clear reality: education often comes with a significant financial cost, and many people carry that burden for years.

The key takeaway is simple:

- Student loans are an investment, but they require careful management

- Interest and time can increase the total cost

- Consistent repayment and planning are essential

When you understand how student loan debt works—and take control of your repayment strategy—you can move forward with greater confidence and financial stability.