When it comes to retirement planning in the United States, a Roth IRA is often considered one of the most powerful—and flexible—accounts available.

Unlike traditional retirement accounts, a Roth IRA offers tax-free income in retirement, which can be a game-changer if you plan ahead.

In this guide, we’ll break down the tax benefits of a Roth IRA in simple terms, with real-world examples and practical tips you can actually use.

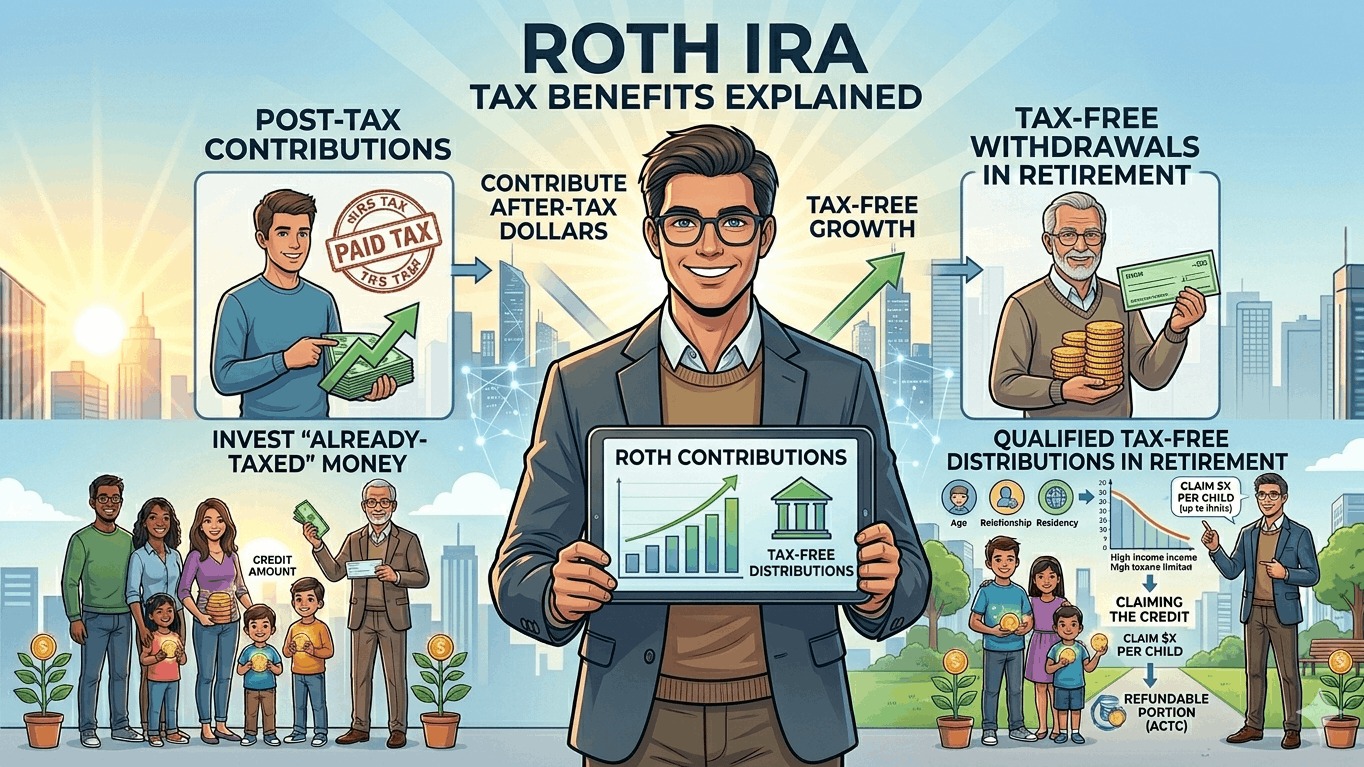

What Is a Roth IRA? (Simple Explanation)

A Roth IRA (Individual Retirement Account) is a retirement account where:

- You contribute money after paying taxes

- Your investments grow over time

- Withdrawals in retirement are completely tax-free

Think of it this way:

You pay taxes now so you don’t have to worry about taxes later.

1. Tax-Free Withdrawals in Retirement

This is the biggest advantage of a Roth IRA.

How it works:

- You already paid taxes on your contributions

- All future growth is tax-free

- Withdrawals after age 59½ are not taxed

Real-world example:

- You invest $6,000 per year

- After 25 years, it grows to $400,000

With a Roth IRA:

- You pay zero tax on that $400,000 withdrawal

That’s a massive advantage compared to taxable accounts.

2. No Taxes on Investment Growth

Inside a Roth IRA:

- No taxes on dividends

- No taxes on capital gains

- No annual tax reporting

Why this matters:

Your full investment stays working for you, allowing maximum compounding.

Example:

In a taxable account, taxes reduce your returns every year.

In a Roth IRA, your money grows uninterrupted.

Related reading:

How Taxes Impact Wealth Building

https://statush.com/finance-statistics/how-taxes-impact-wealth-building

3. No Required Minimum Distributions (RMDs)

Unlike traditional retirement accounts, Roth IRAs do not require you to withdraw money at a certain age.

What this means:

- You can keep your money invested as long as you want

- More time for growth

- Better control over your retirement income

Practical example:

If you don’t need the money at 73, you can leave it invested and let it continue growing tax-free.

This flexibility is a major advantage for long-term investors.

4. Withdraw Contributions Anytime (Tax-Free)

One unique feature of a Roth IRA is flexibility.

You can withdraw:

- Your original contributions

- At any time

- Without taxes or penalties

Example:

If you contributed $30,000 over time:

- You can withdraw up to $30,000 anytime

- No tax, no penalty

Important note:

- This applies only to contributions, not earnings

This makes a Roth IRA useful as a backup emergency fund (though it’s best used for retirement).

5. Ideal for Future Higher Tax Rates

A Roth IRA is especially valuable if you expect your income (and tax rate) to increase.

Example:

- Current tax rate: 12%

- Future tax rate: 25%

By paying taxes now at a lower rate, you avoid higher taxes later.

My take:

If you’re early in your career, Roth accounts are often a smart choice.

6. No Capital Gains Tax Ever

In a regular brokerage account:

- You pay capital gains tax when selling investments

In a Roth IRA:

- You never pay capital gains tax

Related guide:

Capital Gains Tax Explained

https://statush.com/finance-statistics/capital-gains-tax-explained

This makes it ideal for long-term investing and portfolio adjustments.

7. Tax-Free Income Strategy in Retirement

A Roth IRA gives you a unique advantage when planning retirement withdrawals.

Why this matters:

- Withdrawals don’t increase taxable income

- Doesn’t affect Social Security taxation

- Helps reduce overall tax burden

Example strategy:

- Use traditional accounts for basic income

- Use Roth IRA for tax-free withdrawals

This combination can significantly reduce taxes in retirement.

8. Estate Planning Benefits

A Roth IRA is also a powerful tool for passing wealth to the next generation.

Benefits:

- Heirs receive tax-free distributions (with rules)

- Continued tax-free growth potential

- No income tax burden on beneficiaries

This makes it more efficient than many other inheritance options.

9. Diversification of Tax Risk

Most people don’t think about this, but it’s important.

Having both:

- Taxable accounts

- Tax-deferred accounts (like 401(k))

- Tax-free accounts (Roth IRA)

Gives you flexibility to manage taxes in retirement.

Related:

Tax Optimization Strategies

https://statush.com/finance-statistics/tax-optimization-strategies

10. Simple and Flexible Investment Options

Roth IRAs are easy to manage:

- Wide range of investment choices

- No employer dependency

- Full control over your portfolio

This makes it ideal for independent investors.

Roth IRA vs Traditional IRA (Quick Comparison)

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Contributions | After-tax | Pre-tax |

| Tax benefit now | No | Yes |

| Tax on withdrawal | No | Yes |

| RMDs | No | Yes |

| Best for | Future higher taxes | Current tax savings |

When Should You Use a Roth IRA?

A Roth IRA is a great choice if:

- You expect higher future income

- You want tax-free retirement income

- You value flexibility in withdrawals

- You want long-term tax-free growth

Final Thoughts

A Roth IRA is one of the most tax-efficient investment tools available in the U.S. If used correctly, it can provide completely tax-free income in retirement, which is incredibly valuable.

In my opinion, the biggest advantages are:

- Tax-free withdrawals

- No required distributions

- Long-term compounding without tax

Simple strategy:

- Start early

- Contribute consistently

- Combine with other retirement accounts

Continue learning:

- Tax Planning for Retirement

https://statush.com/finance-statistics/tax-planning-for-retirement - How to Reduce Your Taxable Income

https://statush.com/finance-statistics/how-to-reduce-your-taxable-income - Long-Term Tax Planning Guide

https://statush.com/finance-statistics/long-term-tax-planning-guide