Inflation is one of the most important forces shaping the economy—and your personal finances. It affects everything from grocery bills to housing costs, and even how your investments grow over time.

Understanding inflation trends in the United States helps you make better financial decisions, plan for the future, and protect your purchasing power. While inflation may seem like a complex economic concept, its real-world impact is something everyone experiences.

What Is Inflation?

Inflation refers to the rate at which prices for goods and services increase over time. As inflation rises, the purchasing power of money decreases.

In simple terms:

- You need more money to buy the same things

For example, if inflation is 5%, something that costs $100 today may cost $105 next year.

How Inflation Is Measured

Inflation in the U.S. is commonly measured using the Consumer Price Index (CPI), which tracks changes in prices across a basket of goods and services.

These include:

- Food and groceries

- Housing and rent

- Transportation

- Healthcare

The CPI provides a snapshot of how everyday costs change over time.

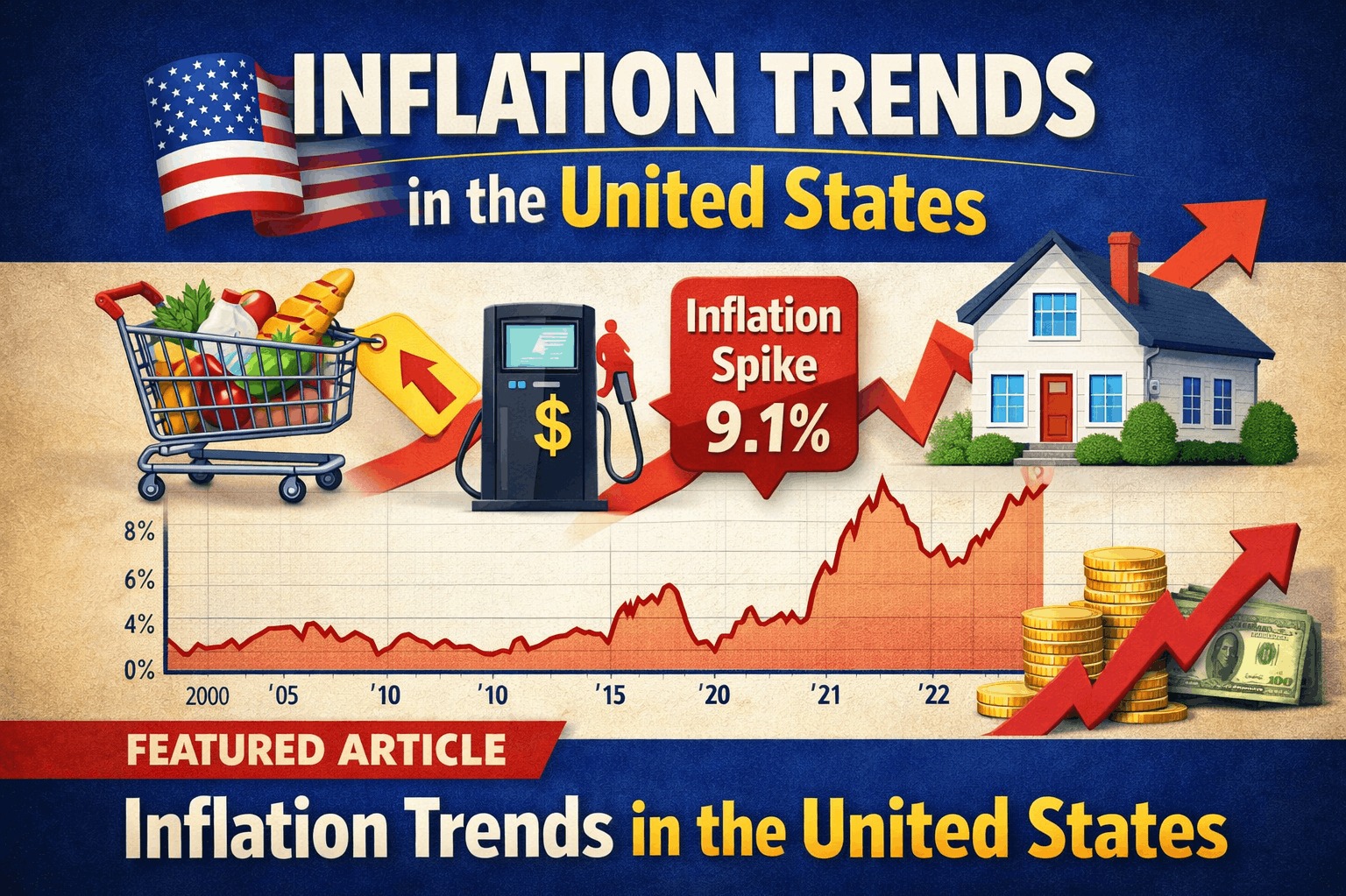

Historical Inflation Trends

Inflation in the United States has fluctuated over decades, influenced by economic conditions, government policies, and global events.

| Period | Inflation Trend | Key Drivers |

|---|---|---|

| 1970s–1980s | High inflation | Oil crises, economic instability |

| 1990s–2010s | Stable, moderate inflation | Economic growth, controlled policies |

| 2020–2022 | Sharp increase | Pandemic, supply chain disruptions |

| 2023–Present | Cooling but elevated | Interest rate adjustments |

This pattern shows that inflation is cyclical and responds to broader economic conditions.

Recent Inflation Trends (2020–2026)

In recent years, inflation has become a major economic concern.

- 2020: Low inflation due to reduced demand

- 2021–2022: Rapid increase (peaking around 8%–9%)

- 2023–2024: Gradual decline

- 2025–2026: Stabilizing but still above historical averages

These changes have affected everything from housing to food prices.

Real-World Example

Let’s look at how inflation affects everyday life:

- Grocery bill in 2020: $200

- Same groceries in 2024: ~$250

That’s a noticeable increase without any change in quantity or quality.

This is why inflation feels impactful—even if your income stays the same.

Major Drivers of Inflation

Inflation doesn’t happen randomly—it is driven by specific factors.

Demand-Pull Inflation

When demand for goods and services exceeds supply, prices rise.

Cost-Push Inflation

When production costs increase (e.g., wages or raw materials), businesses raise prices.

Monetary Policy

Actions by the Federal Reserve, such as adjusting interest rates, influence inflation levels.

Supply Chain Disruptions

Global events can affect production and delivery, leading to price increases.

Inflation and Cost of Living

Inflation directly impacts the cost of living.

| Category | Impact of Inflation |

|---|---|

| Housing | Higher rent and home prices |

| Food | Increased grocery bills |

| Transportation | Rising fuel and vehicle costs |

| Healthcare | Higher medical expenses |

These increases can reduce your financial flexibility over time.

To understand this further:

Average Cost of Living by State – https://statush.com/finance-statistics/average-cost-of-living-by-state

Inflation vs Income Growth

One of the biggest challenges is when inflation rises faster than income.

Example

- Income increase: 3%

- Inflation rate: 6%

Even though you earn more, your purchasing power decreases.

This is why inflation can feel like a “hidden cost” in your finances.

To explore income trends:

Average Household Income in the USA – https://statush.com/finance-statistics/average-household-income-in-the-usa

Impact on Savings and Investments

Inflation affects how your money grows over time.

- Savings lose value if interest rates are lower than inflation

- Investments may need to outperform inflation to create real gains

Example

If your savings earn 2% interest and inflation is 5%:

- You are effectively losing purchasing power

This is why investing is often necessary to stay ahead of inflation.

Inflation and Interest Rates

Interest rates and inflation are closely linked.

When inflation rises:

- The Federal Reserve may increase interest rates

This leads to:

- Higher loan costs

- Reduced borrowing

- Slower economic activity

These actions help control inflation but also impact consumers.

Long-Term Effects of Inflation

Over time, inflation can significantly change the value of money.

| Time Period | Impact on Purchasing Power |

|---|---|

| 10 years | Moderate decline |

| 20 years | Significant reduction |

| 30+ years | Major change in value |

This is why long-term financial planning must account for inflation.

How to Protect Against Inflation

While inflation is unavoidable, there are ways to reduce its impact.

Increase Income Over Time

Career growth and skill development help keep up with rising costs.

Invest in Growth Assets

Stocks and real estate often grow faster than inflation over the long term.

Manage Expenses Carefully

Tracking spending helps maintain financial stability during inflationary periods.

Use Financial Tools

- Savings Goal Calculator – https://statush.com/savings-goal-calculator

- Net Worth Calculator – https://statush.com/net-worth-calculator

- Retirement Calculator – https://statush.com/retirement-calculator

These tools help you adjust your strategy as prices change.

A Practical Perspective

Instead of worrying about inflation itself, focus on how you respond to it.

Ask yourself:

- Is my income growing over time?

- Am I investing to outpace inflation?

- Am I managing expenses effectively?

These actions matter more than short-term inflation changes.

Final Thoughts

Inflation trends in the United States show that while prices rise over time, the impact varies depending on economic conditions and personal financial strategies.

The key takeaway is simple:

- Inflation reduces purchasing power

- It affects everyday expenses and long-term planning

- Smart financial decisions can help you stay ahead

When you understand inflation and plan accordingly, you can protect your finances and continue building wealth—even in a changing economic environment.