When it comes to financial security, retirement savings is one of the most important metrics to track. But a common question people ask is: “Am I saving enough compared to others?”

Looking at average retirement savings by age in the United States can provide helpful benchmarks. However, these numbers are most useful when you understand the context behind them—how savings grow over time, what influences them, and how you can improve your own trajectory.

What Counts as Retirement Savings?

Retirement savings include all the money you’ve set aside specifically for your future when you stop working. This typically includes:

- 401(k) plans

- Individual Retirement Accounts (IRAs)

- Roth IRAs

- Pension plans (if available)

- Other long-term investment accounts

These savings are designed to replace your income in retirement and support your lifestyle.

To understand how these accounts work:

Tax Benefits of Retirement Accounts – https://statush.com/finance-statistics/tax-benefits-of-retirement-accounts

Average vs Median Savings

Just like income and net worth, retirement savings can be measured in two ways: average and median.

| Measure | Explanation | Why It Matters |

|---|---|---|

| Average Savings | Total savings divided by number of people | Can be skewed by high savers |

| Median Savings | The middle value | More realistic for typical individuals |

The average is often higher because a small group of people have very large retirement accounts. The median gives a clearer picture of what most people have saved.

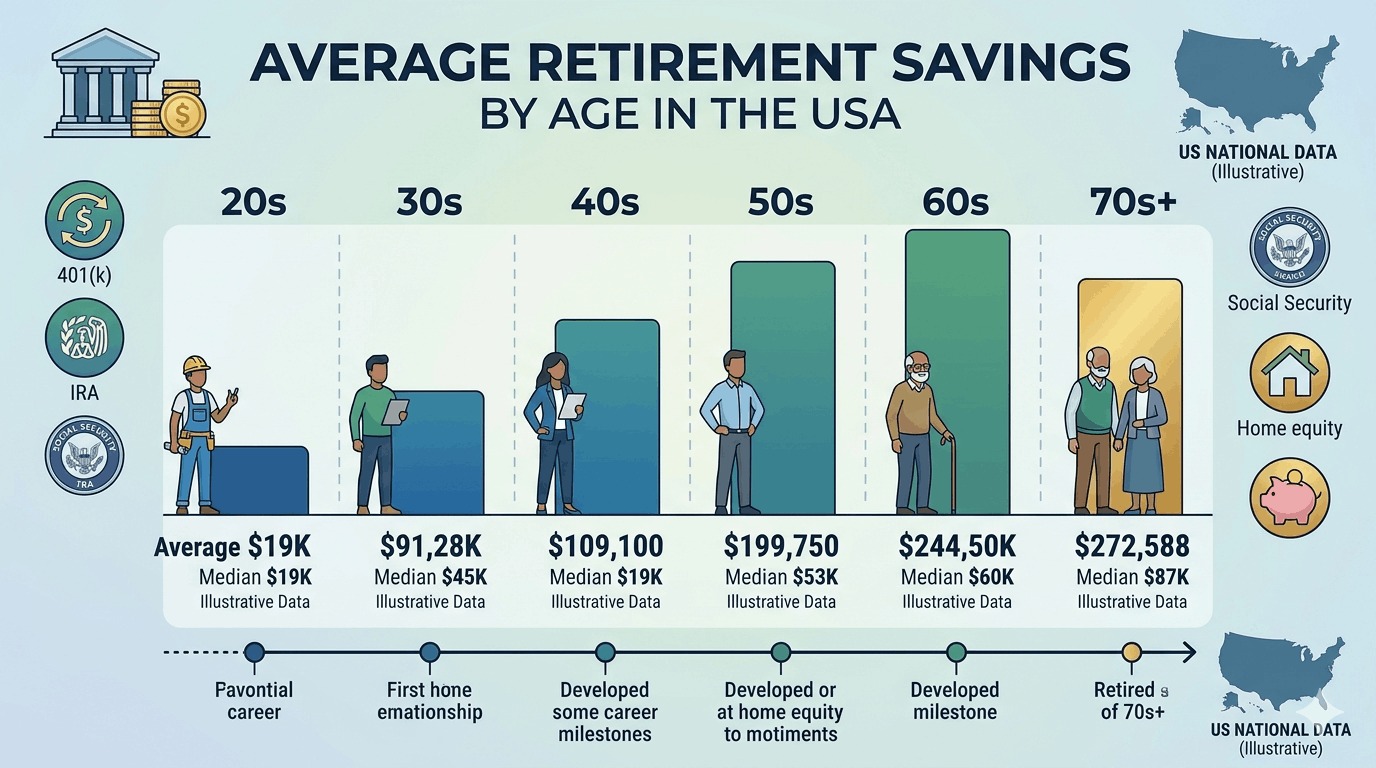

Retirement Savings by Age Group

Savings tend to grow gradually over time as income increases and investments compound.

| Age Group | Savings Pattern | Explanation |

|---|---|---|

| Under 35 | Low savings | Early career, lower income, starting to save |

| 35–44 | Moderate growth | Higher income, consistent contributions begin |

| 45–54 | Strong growth | Peak earning years, increased contributions |

| 55–64 | Highest accumulation | Final years before retirement, maximum savings |

| 65+ | Stabilization or drawdown | Retirement begins, withdrawals start |

Understanding Each Stage in Detail

Under 35: Getting Started

At this stage, many people are just beginning their careers. Income is often limited, and financial priorities may include paying off student loans or building an emergency fund.

Real Example

A 30-year-old might have:

- $15,000 in a 401(k)

- $5,000 in savings

While this may seem low, the key advantage at this stage is time. Even small contributions can grow significantly through compounding.

35–44: Building Momentum

During this phase, income typically increases, allowing for higher contributions to retirement accounts.

Many individuals begin to take retirement planning more seriously, contributing consistently and taking advantage of employer matching programs.

45–54: Acceleration Phase

This is when retirement savings often grow rapidly.

At this stage:

- Income is higher

- Contributions are larger

- Investment growth becomes more noticeable

People also start focusing more on long-term planning rather than short-term expenses.

55–64: Peak Savings Years

These are the final working years before retirement.

Individuals often:

- Max out retirement contributions

- Reduce debt

- Prepare for withdrawals

This stage is critical because it sets the foundation for retirement income.

65+: Transition to Retirement

Once retirement begins, savings are no longer just growing—they’re being used.

The focus shifts to:

- Managing withdrawals

- Minimizing taxes

- Ensuring savings last

To understand this transition:

Tax Planning for Retirement – https://statush.com/finance-statistics/tax-planning-for-retirement

Real-World Comparison

Let’s compare two individuals at age 50:

Person A

- Savings: $150,000

- Started investing late

- Contributes irregularly

Person B

- Savings: $300,000

- Started early

- Contributes consistently

Even if Person A earns more, Person B has a stronger financial position due to consistency and time in the market.

The Power of Compounding

Retirement savings benefit heavily from compounding—the process where your investments generate returns, and those returns generate additional returns.

Example

If you invest $5,000 annually:

- After 10 years, you may have around $70,000

- After 30 years, that amount could grow to several hundred thousand dollars

The earlier you start, the more powerful compounding becomes.

To explore this:

Compound Interest Calculator – https://statush.com/compound-interest-calculator

Factors That Influence Retirement Savings

Several factors determine how much people save over time.

Income Level

Higher income allows for larger contributions, but it doesn’t guarantee better savings habits.

Contribution Consistency

Regular contributions, even small ones, can lead to significant long-term growth.

Investment Strategy

Choosing the right mix of investments affects how quickly savings grow.

Taxes

Taxes can reduce investment returns and retirement income.

To understand this impact:

How Taxes Impact Wealth Building – https://statush.com/finance-statistics/how-taxes-impact-wealth-building

Common Mistakes to Avoid

Many people fall behind in retirement savings due to avoidable mistakes.

These often include:

- Delaying the start of saving

- Not contributing enough

- Ignoring employer matching

- Withdrawing funds early

Small mistakes early on can have large consequences later.

Using Tools to Plan Retirement Savings

Planning becomes easier when you use the right tools.

- Retirement Calculator – https://statush.com/retirement-calculator

- 401k Calculator – https://statush.com/401k-calculator

- Savings Goal Calculator – https://statush.com/savings-goal-calculator

These tools help you estimate how much you need and track your progress.

A Practical Perspective

Instead of comparing yourself strictly to averages, focus on your own progress.

Ask yourself:

- Am I saving consistently?

- Are my contributions increasing over time?

- Am I planning for long-term financial security?

These questions matter more than how you compare to others.

Final Thoughts

Average retirement savings by age provides a useful benchmark, but it’s not a fixed rule. Everyone’s journey is different, shaped by income, habits, and financial decisions.

The key takeaway is simple:

- Start early

- Stay consistent

- Let compounding work over time

When you focus on steady progress rather than perfection, you build a strong foundation for a secure and comfortable retirement.