Your credit score is one of the most important numbers in your financial life. It affects your ability to borrow money, the interest rates you receive, and even opportunities like renting a home or getting approved for certain services.

Understanding the average credit score in the United States gives you a useful benchmark. But more importantly, it helps you understand how credit works, what influences your score, and how you can improve it over time.

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness—essentially, how reliable you are as a borrower.

It is calculated based on your credit history, including:

- Payment behavior

- Debt levels

- Length of credit history

- Types of credit used

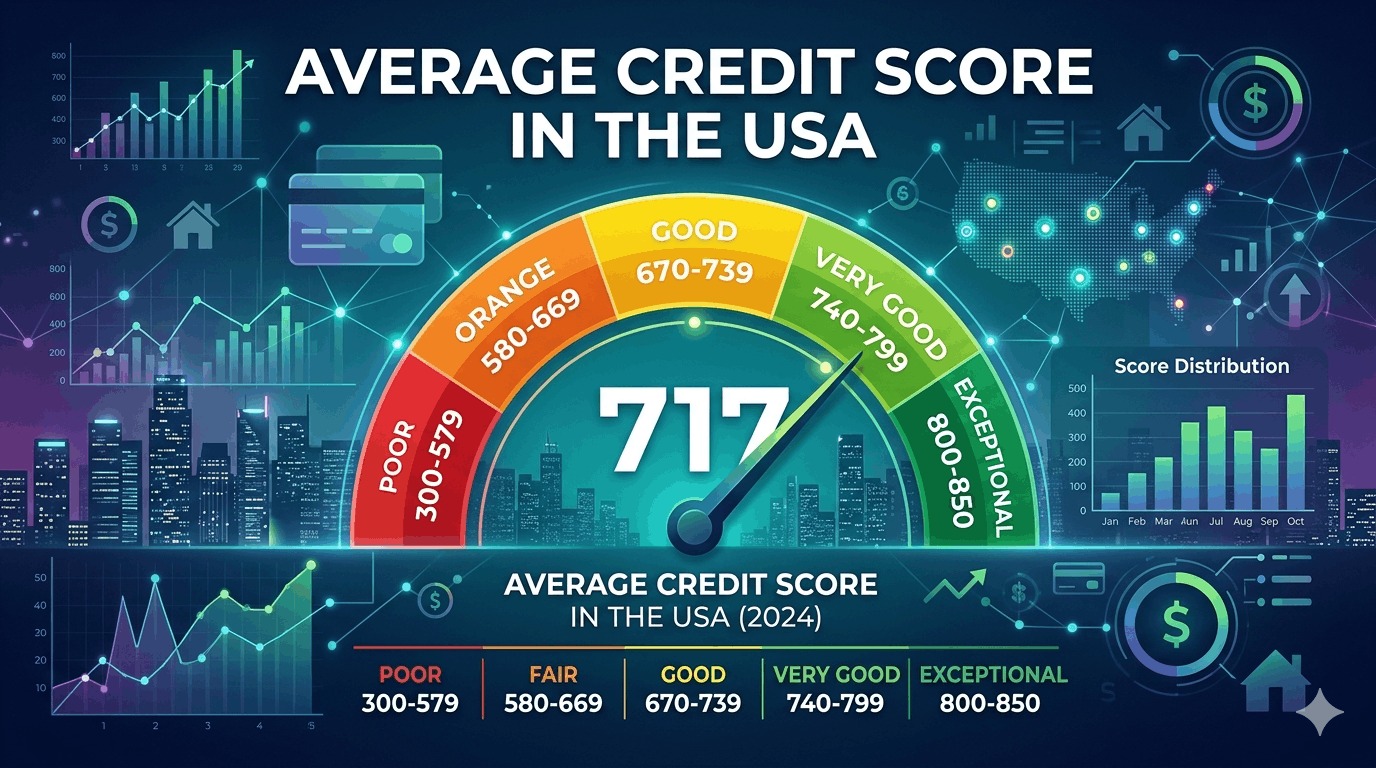

Most credit scores in the U.S. range from 300 to 850, with higher scores indicating better credit health.

Average Credit Score in the USA

In recent years, the average credit score in the United States has generally been in the mid-to-high 600s to low 700s range, depending on the scoring model and data source.

This suggests that most Americans fall into the “good” credit category—but there is still a wide variation depending on age, income, and financial habits.

Credit Score Ranges Explained

To understand where you stand, it helps to see how credit scores are categorized.

| Credit Score Range | Rating | What It Means |

|---|---|---|

| 300–579 | Poor | High risk, limited access to credit |

| 580–669 | Fair | Moderate risk, higher interest rates |

| 670–739 | Good | Average borrower, reasonable terms |

| 740–799 | Very Good | Lower risk, better loan conditions |

| 800–850 | Excellent | Top-tier borrower, best rates available |

Credit Score by Age Group

Credit scores tend to improve with age as individuals build longer credit histories and develop better financial habits.

| Age Group | Score Trend | Explanation |

|---|---|---|

| 18–29 | Lower scores | Limited credit history, new borrowers |

| 30–44 | Improving scores | More experience managing credit |

| 45–59 | Strong scores | Stable income and longer history |

| 60+ | Highest scores | Established credit patterns and lower debt |

Real-World Example

Let’s compare two individuals:

Person A

- Credit score: 620

- Applies for a loan

- Receives higher interest rate

Person B

- Credit score: 760

- Applies for the same loan

- Receives lower interest rate

Over time, Person B saves thousands of dollars in interest simply because of a higher credit score.

What Impacts Your Credit Score?

Your credit score is influenced by several key factors, each carrying a different weight.

Payment History

This is the most important factor. Consistently paying bills on time builds a strong credit profile.

Credit Utilization

This refers to how much of your available credit you’re using.

For example:

- If your credit limit is $10,000 and you use $3,000, your utilization is 30%

Lower utilization generally leads to better scores.

Length of Credit History

The longer your credit history, the more data lenders have to evaluate your behavior.

Types of Credit

Having a mix of credit types—such as credit cards, loans, and mortgages—can positively impact your score.

New Credit Inquiries

Applying for multiple credit accounts in a short period can temporarily lower your score.

Why Credit Scores Matter

Your credit score affects more than just loan approvals.

It influences:

- Interest rates on loans

- Credit card approvals

- Rental applications

- Insurance premiums in some cases

A higher score can save you money and provide more financial flexibility.

Credit Score and Debt

Debt levels play a significant role in your credit score.

High levels of debt, especially credit card balances, can lower your score and make borrowing more expensive.

To understand how debt affects finances:

Credit Card Debt Statistics in the USA – https://statush.com/finance-statistics/credit-card-debt-statistics-in-the-usa

Improving Your Credit Score Over Time

Improving your credit score doesn’t happen overnight, but consistent habits can make a big difference.

Real Example

If you:

- Pay all bills on time

- Reduce credit card balances

- Avoid unnecessary new credit

Your score can gradually improve over months or years.

Common Mistakes That Lower Credit Scores

Many people unintentionally damage their credit through avoidable mistakes.

These include:

- Missing payments

- Using too much of available credit

- Closing old credit accounts

- Applying for too many loans at once

Even small mistakes can have a noticeable impact.

Tools to Track and Improve Credit Health

Monitoring your financial situation helps you stay on track.

- Net Worth Calculator – https://statush.com/net-worth-calculator

- Debt Payoff Calculator – https://statush.com/debt-payoff-calculator

- Savings Goal Calculator – https://statush.com/savings-goal-calculator

These tools help you manage the factors that influence your credit score.

A Practical Perspective

Instead of focusing only on the national average, it’s more useful to evaluate your own progress.

Ask yourself:

- Is my score improving over time?

- Am I managing debt responsibly?

- Am I building a strong credit history?

These questions matter more than how you compare to others.

Final Thoughts

The average credit score in the USA provides a helpful benchmark, but your personal score is what truly matters.

The key takeaway is simple:

- Credit scores reflect financial behavior over time

- Small, consistent habits make a big difference

- A higher score leads to better financial opportunities

By understanding how credit works and managing it carefully, you can improve your score and create stronger financial opportunities for the future.