In the 2026 American credit market, data transparency is at an all-time high. Every time your credit file is accessed, a "footprint" is left behind. These footprints are categorized as either Hard Inquiries or Soft Inquiries.

While both involve a peek into your financial history, they have vastly different impacts on your FICO® score and your ability to secure debt. Understanding the distinction is vital for maintaining a "lending-ready" profile.

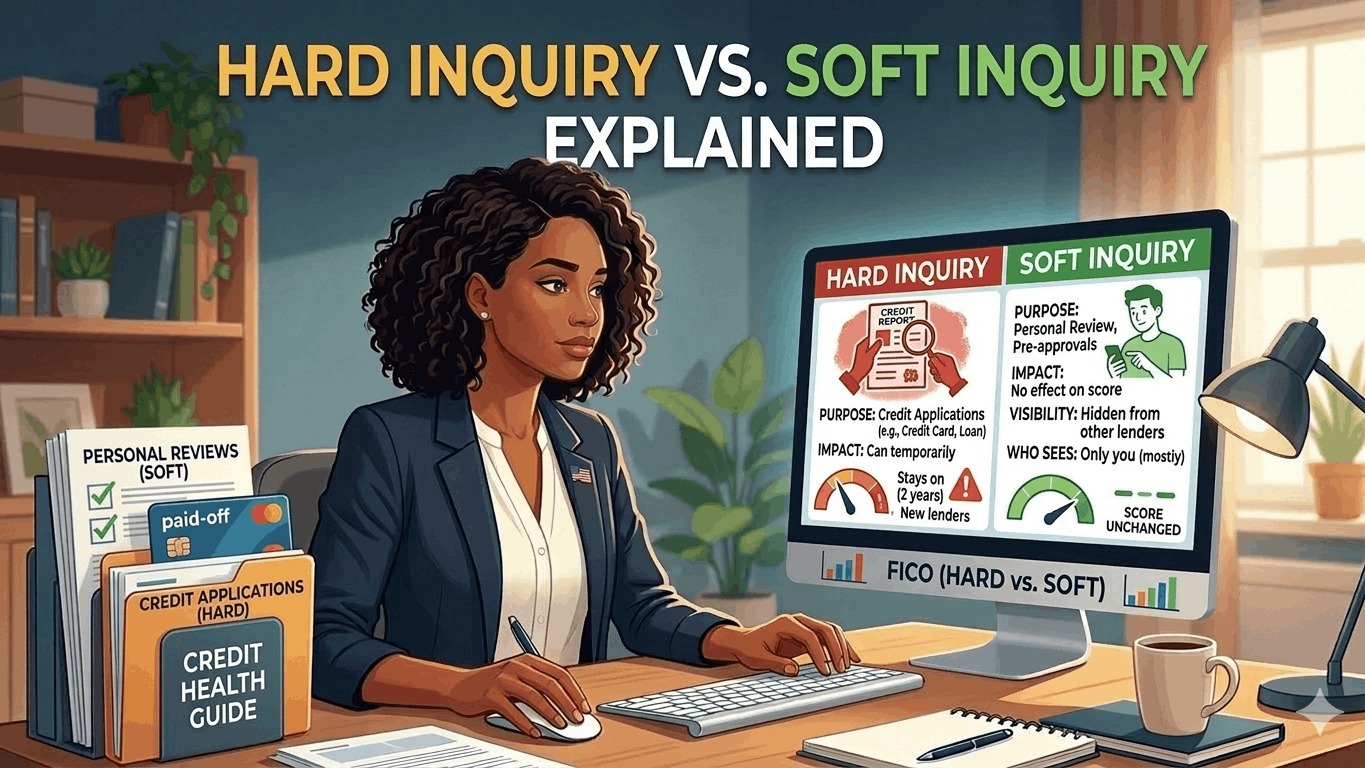

1. What is a Hard Inquiry?

A hard inquiry (or "hard pull") occurs when you officially apply for credit and a lender reviews your credit report to make a lending decision.

Key Characteristics:

- User Permission: These require your explicit legal consent (usually a checkbox or signature).

- Credit Impact: They typically lower your score by 5–10 points temporarily.

- Visibility: They are visible to other lenders who check your report.

- Duration: They stay on your report for 24 months, though FICO only considers them in your score for the first 12 months.

Common Examples:

- Mortgage applications.

- Auto loan applications.

- Credit card applications.

- Personal loan or student loan requests.

- In some cases, apartment rental applications or cell phone contracts.

2. What is a Soft Inquiry?

A soft inquiry (or "soft pull") happens when your credit file is checked for reasons not related to an official application for new debt.

Key Characteristics:

- User Permission: These can happen without your direct action (e.g., a bank checking if you’re eligible for a "pre-approved" offer).

- Credit Impact: They have zero impact on your credit score.

- Visibility: Only you can see them when you pull your own report; lenders cannot see your soft inquiries.

- Duration: They are recorded but do not affect your lending power.

Common Examples:

- Checking your own credit score (Experian, Credit Karma, etc.).

- "Pre-approved" credit card or insurance offers in the mail.

- Employer background checks.

- Existing lenders doing "account maintenance" checks to see if they should raise or lower your limit.

3. Comparing the Impact

In the 2026 credit scoring models, the "weight" of a hard inquiry depends on your overall credit health.

| Feature | Hard Inquiry | Soft Inquiry |

|---|---|---|

| Score Impact | Typically -5 to -10 points | No Impact |

| Visible to Lenders? | Yes | No |

| Affects Interest Rates? | Yes (indirectly via score) | No |

| Common Trigger | You applying for a loan | Checking your own score |

4. The 2026 "Rate Shopping" Rule

A common fear is that comparing multiple lenders for a single purchase (like a mortgage) will destroy your score with multiple hard pulls. In 2026, U.S. credit models have a built-in "deduplication" window.

- The Window: If you have multiple hard inquiries for the same type of loan (Mortgage or Auto) within a 14-to-45-day window, they are treated as a single inquiry for scoring purposes.

- The Strategy: Do all your "rate shopping" within a two-week period to ensure your score only takes one small hit instead of several.