In 2026, credit accuracy is more critical than ever. With the U.S. financial system fully transitioned to FICO 10T and VantageScore 4.0, lenders are using "trended data" to evaluate your behavior over a 24-month period. A single error—like a "settled" status on a fully paid loan—can now have a compounding negative effect on your score.

Under the Fair Credit Reporting Act (FCRA), revised for 2026, you have the absolute right to an accurate report. Here is how to identify and resolve common inaccuracies.

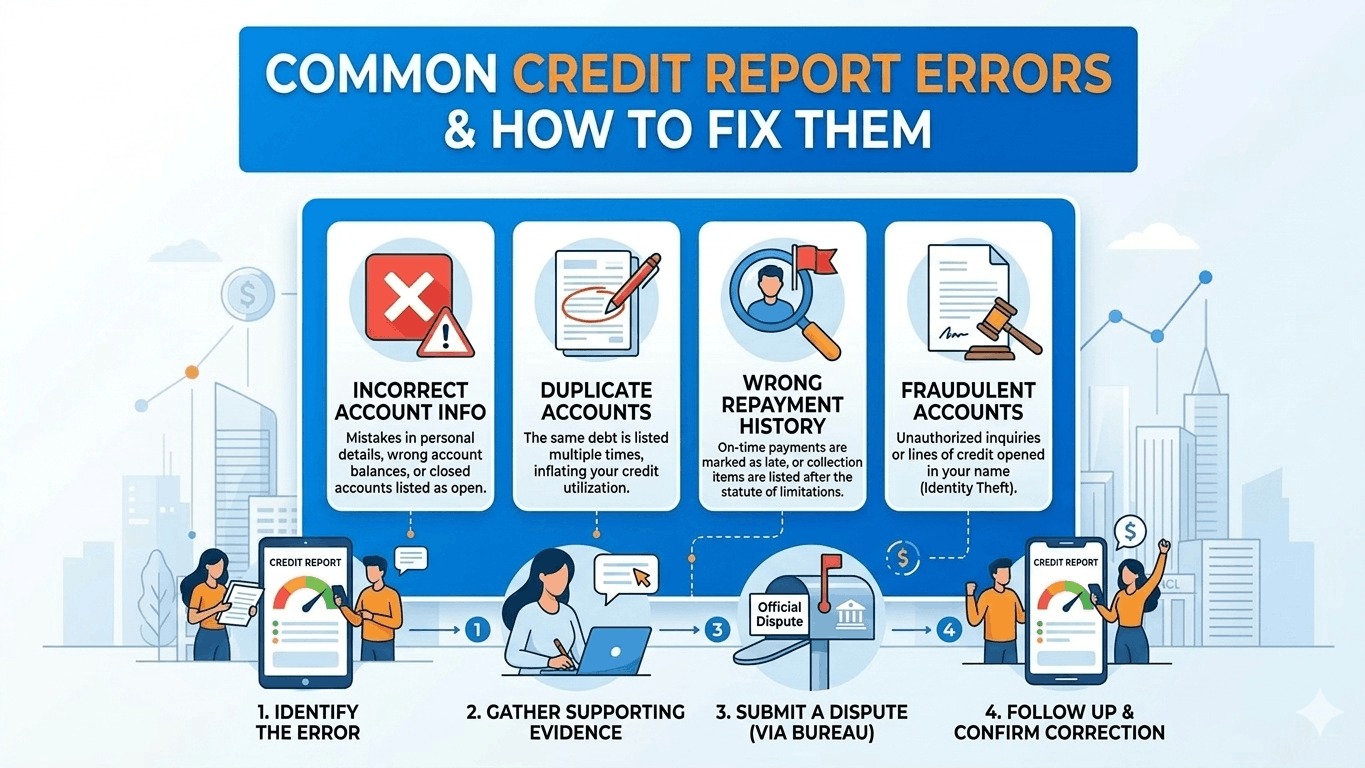

1. Common Errors to Spot in 2026

Errors generally fall into three categories: identity, account status, and data management.

Identity Errors

- Mixed Files: Information from another person with a similar name or SSN appears on your report.

- Incorrect Personal Details: Misspelled names, outdated addresses, or wrong phone numbers can lead to verification failures during loan applications.

- Identity Theft: Accounts you never opened or inquiries you didn't authorize.

Account Status Errors

- The "Settled" Trap: A loan you paid in full is marked as "Settled" or "Written-off," which signals high risk to 2026 AI underwriting models.

- Closed vs. Open: Accounts you closed still showing as "Active" (inflating your debt-to-income ratio) or open accounts mistakenly marked as “Closed.”

- Wrong DPD (Days Past Due): An on-time payment incorrectly coded as "030" (30 days late) or “060.”

Data Management Errors

- Duplicate Entries: The same debt listed multiple times, often by the original lender and a collection agency, which artificially doubles your reported debt.

- Inaccurate Limits: Your credit limit is reported lower than it actually is, which spikes your Credit Utilization Ratio.

2. The Step-by-Step Fix (2026 Protocol)

Step 1: Gather Your Evidence

Do not start a dispute without proof. Collect bank statements, "Paid in Full" letters, canceled checks, or a government-issued ID. If the error is identity theft, file a report at IdentityTheft.gov first.

Step 2: Contact the Credit Bureaus

You must dispute the error with each bureau reporting it (Equifax, Experian, and TransUnion).

- The Written Advantage: While online portals are faster, sending a Certified Letter with Return Receipt creates a legal paper trail. In 2026, this is still the most reliable way to ensure a thorough investigation.

- Timeline: Bureaus generally have 30 days to investigate and respond (unless they deem the dispute "frivolous").

Step 3: Contact the "Furnisher"

The "furnisher" is the bank or company that provided the wrong data. Send them a copy of your dispute and evidence. If they find an error, they are legally required to notify all three bureaus to fix it.

3. Contact Information for Major Bureaus (2026)

| Bureau | Online Dispute | Phone | Mailing Address |

|---|---|---|---|

| Experian | experian.com/disputes | (888) 397-3742 | P.O. Box 4500, Allen, TX 75013 |

| Equifax | equifax.com/personal/credit-report-services | (866) 349-5191 | P.O. Box 740256, Atlanta, GA 30348 |

| TransUnion | dispute.transunion.com | (800) 916-8800 | P.O. Box 2000, Chester, PA 19016 |

4. What If the Dispute is Denied?

If the bureau verifies the information as "accurate" but you know it’s wrong:

- Add a Consumer Statement: You have the right to add a 100-word statement to your file explaining your side of the dispute.

- Escalate to the CFPB: File a formal complaint with the Consumer Financial Protection Bureau.

- Seek a Fair Credit Attorney: If a lender's refusal to fix a clear error causes you financial harm (like a loan rejection), you may be entitled to damages under the FCRA.