the average American holds about four credit cards. While having multiple accounts can significantly boost your credit limit and rewards, it also increases the complexity of your financial life. With the introduction of FICO 10T—which tracks your balance trends over 24 months—managing multiple cards requires a shift from "monthly maintenance" to “strategic oversight.”

Here is how to master a multi-card wallet in 2026 without missing a beat.

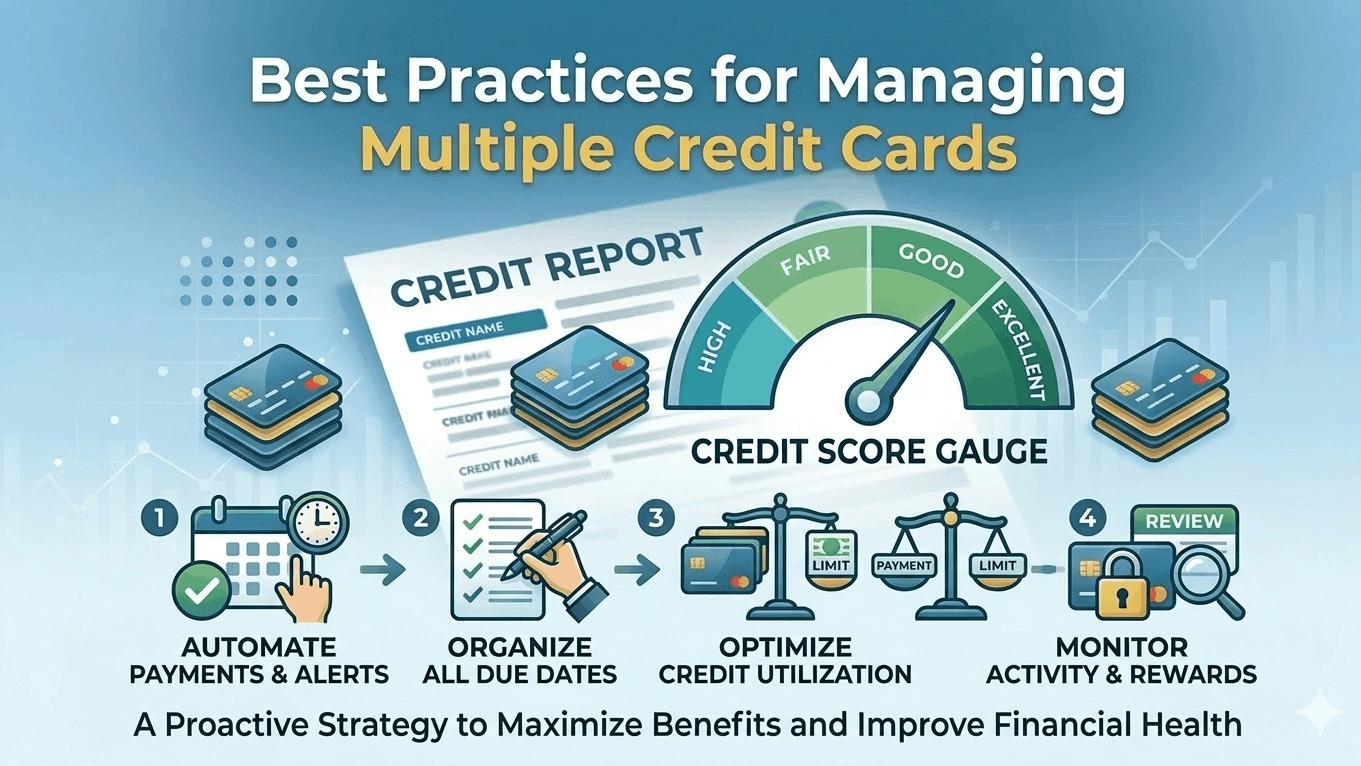

1. The "Single Due Date" Strategy

The biggest risk of multiple cards is the "staggered deadline" trap, where bills fall on different days throughout the month.

- The Fix: Log into your accounts or call your issuers to align your due dates. Many 2026 borrowers set all their cards to be due on the 3rd or 5th of the month.

- Why it works: This allows you to treat "Credit Card Day" like a single utility bill. You can sit down once a month, verify all statements, and ensure every balance is cleared.

2. Reward Mapping: Assigning a Purpose

Don't just pull out a random card at the register. In 2026, the most efficient users "tag" their cards for specific high-yield categories:

- The "Groceries & Gas" Card: Usually a card offering 3%–6% back on essentials.

- The "Dining & Travel" Card: For 3x points on restaurants and flights.

- The "Catch-All" Card: A flat 2% cash-back card for everything else (repairs, utilities, retail).

- The "Emergency" Anchor: A card with your highest limit and lowest APR, kept at home and used once every six months for a small purchase to keep the account active.

3. Leverage 2026 Management Tools

Manual spreadsheets are a thing of the past. Modern apps now integrate directly with your credit reports to give you a "command center" view.

- YNAB (You Need A Budget): Excellent for multi-card users because it "holds" money from your checking account the moment you swipe a credit card, ensuring you always have the cash to pay the bill in full.

- Monarch Money & Copilot: These 2026 leaders use AI to categorize spending across all your cards and send Real-Time Utilization Alerts if one card is getting too close to its limit.

- MaxRewards: This app tells you exactly which card to use at a specific store to get the highest reward percentage.

4. Managing the "Average Age" Risk

Every time you open a new card, your Average Age of Accounts (AAoA) drops. In the 2026 FICO 10T model, "credit depth" is a major trust signal.

- Space Your Applications: Wait at least 6 months between new card applications.

- The "Sock Drawer" Card: If you have an old card with no annual fee that you no longer use, do not close it. Put a small recurring subscription (like a $10 gym membership) on it and set it to autopay. This keeps your oldest account history "alive" and your total credit limit high.

5. Security: The "Freeze and Alert" Protocol

More cards mean more targets for fraud. In 2026, you should utilize these two features:

- The Digital Lock: If you have a card you rarely use, keep it "Locked" or "Frozen" via the bank's app. You can unlock it in seconds if you need to use it.

- Push Notifications for $1.00: Set every card to send a push notification for any transaction over $0.01. This allows you to catch fraudulent "test charges" instantly.