You bought a stock, held it for a while, sold it for a profit — congratulations. But before you celebrate, the IRS wants a share. That's capital gains tax in a nutshell.

Whether you're an active investor, a homeowner thinking about selling, or just starting to build wealth, understanding capital gains tax is essential to keeping more of what you earn. This guide covers everything you need to know, updated with the latest 2025 and 2026 IRS numbers.

What Is Capital Gains Tax?

Capital gains tax is the tax you pay on the profit you make when you sell a capital asset for more than you paid for it.

A capital asset includes:

- Stocks and bonds

- Mutual funds and ETFs

- Real estate (investment properties, vacation homes, land)

- Cryptocurrency

- Collectibles (art, coins, antiques)

- A business you own

The profit — the difference between what you paid (your cost basis) and what you sold it for — is your capital gain. The IRS treats this gain as taxable income.

Important: You only owe capital gains tax when you sell the asset. As long as you hold it, the gain is "unrealized" and completely tax-free, no matter how much your investment has grown.

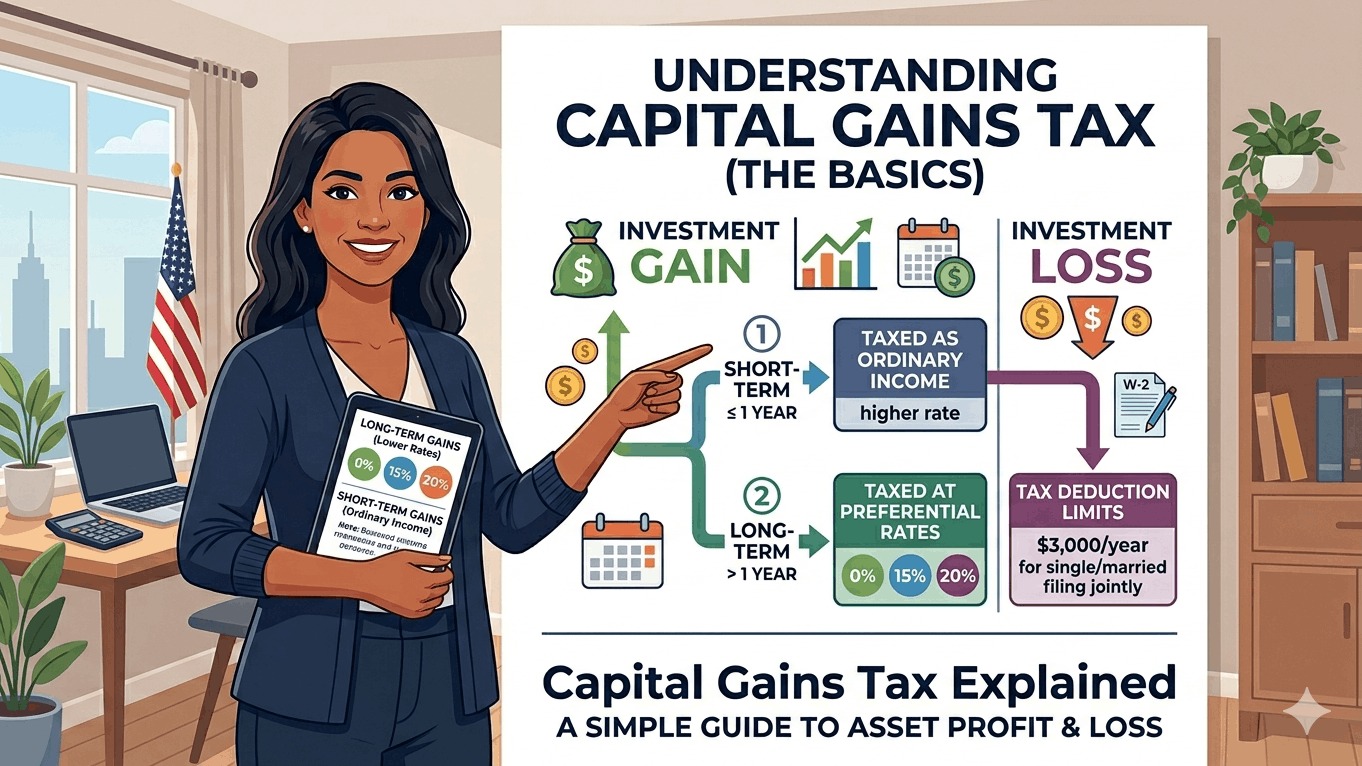

Short-Term vs. Long-Term Capital Gains: The Most Important Distinction

The single most impactful factor in how much capital gains tax you pay is how long you held the asset before selling.

| Type | Holding Period | Tax Rate |

|---|---|---|

| Short-Term Capital Gain | 1 year or less | Taxed as ordinary income (10%–37%) |

| Long-Term Capital Gain | More than 1 year | Preferential rates: 0%, 15%, or 20% |

This distinction can mean the difference between paying 37% and paying 0% on the same profit. It is one of the most powerful and legal tax strategies available to everyday investors: simply wait one year and one day before selling.

For example, if you're in the 22% income tax bracket and sell a stock after 11 months for a $10,000 profit, you owe $2,200 in tax. Hold that same stock one more month — past the one-year mark — and your tax bill could drop to $1,500 (at the 15% long-term rate) or even $0 if your income qualifies.

To understand how ordinary income tax brackets work and how short-term gains interact with them, read our guide: How Tax Brackets Work.

2025 Long-Term Capital Gains Tax Rates

(Applies to assets sold in 2025 — reported on returns filed in early 2026)

Single Filers:

| Rate | Taxable Income Range |

|---|---|

| 0% | $0 – $48,350 |

| 15% | $48,351 – $533,400 |

| 20% | Over $533,400 |

Married Filing Jointly:

| Rate | Taxable Income Range |

|---|---|

| 0% | $0 – $96,700 |

| 15% | $96,701 – $600,050 |

| 20% | Over $600,050 |

Head of Household:

| Rate | Taxable Income Range |

|---|---|

| 0% | $0 – $64,750 |

| 15% | $64,751 – $566,700 |

| 20% | Over $566,700 |

Key takeaway for 2025: The IRS confirmed that the tax rate on most long-term capital gains is no higher than 15% for the vast majority of Americans. Many lower-income earners pay 0%.

2026 Long-Term Capital Gains Tax Rates

(Applies to assets sold in 2026 — reported on returns filed in early 2027)

Single Filers:

| Rate | Taxable Income Range |

|---|---|

| 0% | $0 – $49,450 |

| 15% | $49,451 – $543,350* |

| 20% | Over $543,350* |

Married Filing Jointly:

| Rate | Taxable Income Range |

|---|---|

| 0% | $0 – $98,900 |

| 15% | $98,901 – $613,700* |

| 20% | Over $613,700* |

*Based on IRS Revenue Procedure 2025-32 and Kiplinger/CNBC reporting. Final full tables apply per IRS official publication.

The 2026 thresholds reflect modest inflation adjustments of roughly 2.3–2.7% from 2025 levels. The good news: more income now falls under the 0% and 15% bands, meaning more investors qualify for lower rates compared to 2025.

2025 Short-Term Capital Gains Tax Rates

Short-term capital gains are taxed at the same rates as ordinary income — your regular tax brackets. There is no preferential rate.

| Tax Rate | Taxable Income (Single Filers, 2025) |

|---|---|

| 10% | $0 – $11,925 |

| 12% | $11,926 – $48,475 |

| 22% | $48,476 – $103,350 |

| 24% | $103,351 – $197,300 |

| 32% | $197,301 – $250,525 |

| 35% | $250,526 – $626,350 |

| 37% | Over $626,350 |

Unlike long-term rates, there is no 0% rate and no 20% ceiling for short-term gains. A trader who flips stocks in days or weeks is taxed exactly like a salaried employee — at whatever ordinary income bracket they fall into.

Real-World Example: Short-Term vs. Long-Term

Meet David, a single filer with $80,000 in taxable income who sold $20,000 worth of stock for a $5,000 profit.

Scenario A — Sold after 9 months (Short-Term): David's total income (with the $5,000 gain added) pushes him into the 22% bracket.

- Tax on the $5,000 gain: $1,100 (22%)

Scenario B — Sold after 13 months (Long-Term): David's taxable income of $80,000 places him in the 15% long-term capital gains bracket.

- Tax on the $5,000 gain: $750 (15%)

David saves $350 simply by waiting four more months. For larger gains, the savings are proportionally much greater.

The Net Investment Income Tax (NIIT): The Hidden 3.8% Surcharge

High-income earners face an additional 3.8% Net Investment Income Tax (NIIT) on top of the regular capital gains rate. This applies to:

- Single filers with modified adjusted gross income (MAGI) above $200,000

- Married filing jointly with MAGI above $250,000

The NIIT applies to the lesser of your net investment income or the amount by which your MAGI exceeds the threshold.

Example: A married couple has $280,000 in MAGI, including $30,000 in long-term capital gains. Their MAGI exceeds the $250,000 threshold by $30,000. The NIIT applies to the lesser of net investment income ($30,000) or the excess ($30,000) — so they owe 3.8% × $30,000 = $1,140 extra.

This can effectively push the top capital gains rate to 23.8% (20% + 3.8%) for top earners.

Special Capital Gains Rates: The Exceptions

Not all long-term capital gains are taxed at 0%/15%/20%. A few asset types face higher maximum rates:

| Asset Type | Special Rate |

|---|---|

| Collectibles (art, coins, antiques) | Max 28% |

| Qualified Small Business Stock (Section 1202) | Max 28% on taxable portion |

| Unrecaptured Section 1250 Gain (real estate depreciation) | Max 25% |

| Short-term gains | Ordinary income rates (up to 37%) |

These exceptions are less common but important to know if you're selling real estate, a business, or collectibles.

Capital Gains on Your Home: The Big Exclusion

Selling your primary residence is one of the most tax-favored events in the U.S. tax code. Under the Section 121 exclusion, you can exclude a significant amount of profit from capital gains tax entirely:

- Single filers: Exclude up to $250,000 in profit

- Married filing jointly: Exclude up to $500,000 in profit

Requirements to qualify:

- You owned the home for at least 2 of the last 5 years

- You lived in it as your primary residence for at least 2 of the last 5 years

- You have not used this exclusion in the last 2 years

Any profit above the exclusion limit is taxed as a long-term capital gain (assuming you've owned the home for over a year). Investment properties, vacation homes, and rental properties do not qualify for this exclusion.

Capital Gains on Cryptocurrency in 2025–2026

The IRS treats cryptocurrency as property, not currency. This means every crypto sale, trade, or exchange is a taxable event subject to capital gains rules:

- Held over one year → Long-term capital gains rates (0%, 15%, or 20%)

- Held one year or less → Short-term rates (ordinary income, up to 37%)

Important 2026 update: Starting in 2026, the IRS is implementing stricter reporting through Form 1099-DA. Crypto brokers and exchanges will now report your transactions directly to the IRS, making accurate record-keeping more critical than ever. If you trade crypto, maintaining detailed records of every purchase price (cost basis) and sale date is no longer optional.

Capital Losses: How They Work in Your Favor

What if you sell an asset at a loss? Capital losses can actually help reduce your tax bill through tax-loss harvesting.

Here's how it works:

- Capital losses first offset capital gains of the same type (short-term losses against short-term gains, long-term losses against long-term gains)

- Net losses can then offset gains of the other type

- If losses still exceed gains, you can deduct up to $3,000 of net losses against ordinary income per year

- Any remaining losses carry forward to future tax years indefinitely

Example: You have $8,000 in long-term capital gains and $5,000 in capital losses.

- Net taxable gain: $3,000 (taxed at long-term rates)

- You've reduced your taxable gain by $5,000

If losses exceed gains by more than $3,000, the excess carries forward — it doesn't disappear.

Watch the Wash-Sale Rule: You cannot claim a loss on a security if you buy a "substantially identical" security within 30 days before or after the sale. As of 2026, this rule primarily applies to stocks and securities. Watch for any IRS updates that could extend it to cryptocurrency.

Capital Gains in Tax-Advantaged Accounts: Zero Tax

One of the best capital gains strategies requires no timing, no tax-loss harvesting, and no complex planning: invest inside tax-advantaged accounts.

Inside these accounts, your investments grow without triggering capital gains tax:

- 401(k) and Traditional IRA — Gains grow tax-deferred; you pay ordinary income tax only on withdrawals in retirement

- Roth IRA and Roth 401(k) — Gains grow completely tax-free; qualified withdrawals owe zero tax

- 529 College Savings Plans — Gains are tax-free when used for qualified education expenses

- HSA (Health Savings Account) — Triple tax advantage: deductible contributions, tax-free growth, tax-free withdrawals for medical expenses

By moving your highest-growth investments into these accounts, you can legally avoid capital gains tax entirely on those assets.

7 Strategies to Minimize Capital Gains Tax in 2025–2026

1. Hold for over one year The single most effective strategy. Switching from short-term to long-term rates can reduce your tax rate by up to 20+ percentage points.

2. Use tax-loss harvesting Sell underperforming investments to generate losses that offset your gains. Unused losses carry forward to future years.

3. Max out your Roth IRA For 2025, contribute up to $7,000 ($8,000 if 50+). Qualifying withdrawals — including all gains — are completely tax-free.

4. Stay below the 0% threshold In 2025, single filers with taxable income under $48,350 (or $96,700 for married couples) pay zero long-term capital gains tax. Strategic income management (deferring income, increasing deductions) can keep you in this bracket.

5. Gift appreciated assets Instead of selling investments and owing tax, gift shares directly to charity or family members in lower tax brackets. The charity pays no tax; the recipient takes on your cost basis.

6. Rebalance inside tax-advantaged accounts Rather than selling appreciated investments in a taxable account to rebalance your portfolio, rebalance within your 401(k) or IRA where no gains are triggered.

7. Use the home sale exclusion wisely Plan your home sale to meet the 2-out-of-5-year rule and exclude up to $500,000 in profit (married filing jointly) from tax entirely.

How Capital Gains Tax Interacts With Your Income Tax Bracket

Capital gains do not exist in isolation — they interact with your overall taxable income and affect which bracket your other income falls into. This is a nuanced but important point.

Long-term capital gains are added to your ordinary income when determining where you land on the capital gains rate table. However, they are not added to your ordinary income for the purpose of pushing your wages into a higher income tax bracket.

For the full picture of how all your income sources — wages, investment income, business income — stack together and affect your overall tax bill, see our complete guide: How Tax Brackets Work.

Common Capital Gains Tax Myths — Busted

| Myth | Reality |

|---|---|

| "I owe taxes as soon as my investment grows in value" | False — gains are only taxed when you sell (realized gains) |

| "All capital gains are taxed at the same rate" | False — short-term and long-term rates differ drastically |

| "I have to pay capital gains on my 401(k)" | False — gains inside retirement accounts are tax-deferred or tax-free |

| "Crypto is too hard to track for taxes" | Risky — the IRS requires reporting, and Form 1099-DA now makes crypto brokers report directly to the IRS in 2026 |

| "Selling my house always triggers capital gains" | Not necessarily — the $250K/$500K exclusion shields most homeowners completely |

Final Thoughts

Capital gains tax is one of the most manageable taxes in the U.S. system — if you understand the rules. The combination of preferential long-term rates, the home sale exclusion, tax-advantaged accounts, and tax-loss harvesting gives everyday investors powerful tools to legally minimize what they owe.

The most important move is also the simplest: hold your investments for more than one year before selling. That single decision can cut your tax rate significantly — or even to zero.

For a deeper understanding of how your overall income, brackets, and tax rate come together, read our full breakdown: How Tax Brackets Work.