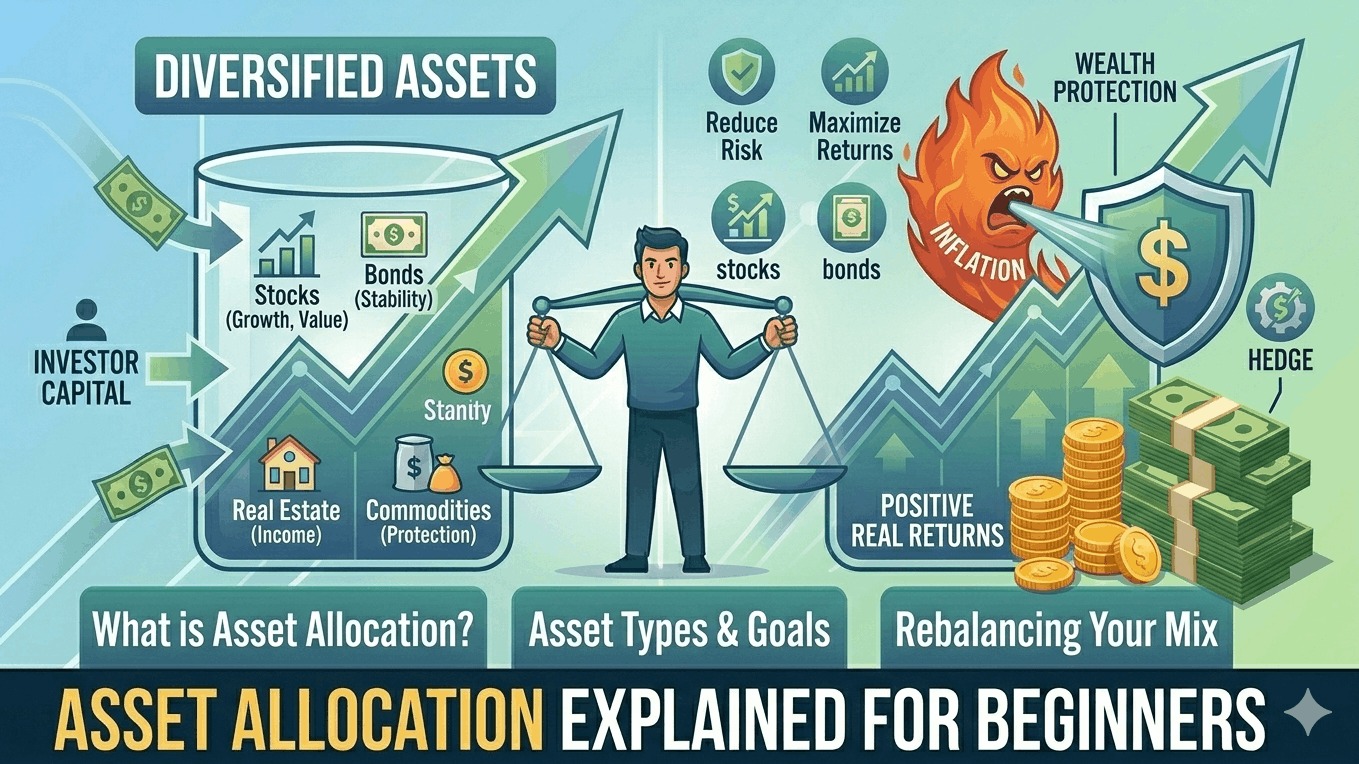

In the investing world of 2026, asset allocation is the single most important decision you will make. While picking the "next big stock" gets all the headlines, academic research consistently shows that over 90% of your portfolio's long-term returns are determined by your asset allocation—not individual stock picking.

Asset allocation is the process of dividing your investment portfolio among different asset categories, such as stocks, bonds, cash, and "alternatives" (like gold or real estate). Think of it as the "recipe" for your wealth: the right mix of ingredients ensures your portfolio doesn't "burn" during a market crash or "stay raw" (fail to grow) during a bull market.

1. The Three Main Pillars of Allocation

To build a balanced portfolio in 2026, you must understand the "job" of each asset class:

- Stocks (Equities) – The Engine: Their job is growth. Stocks represent ownership in companies. They are volatile (they go up and down fast), but historically, they provide the highest long-term returns to help you beat inflation.

- Bonds (Fixed Income) – The Shock Absorber: Their job is stability. When you buy a bond, you are lending money to a government or corporation in exchange for interest. Bonds usually move in the opposite direction of stocks, cushioning the blow when the market drops.

- Cash / Equivalents – The Safety Net: Their job is liquidity. This includes high-yield savings accounts or money market funds. In 2026, with interest rates stabilizing around 3.5%, cash is no longer "trash"—it provides a safe place to park money you might need in the next 1–2 years.

2. Real-World Example: The "Age-Based" Rule

A classic beginner strategy is the "Rule of 100" (or 110/120 for more aggressive 2026 investors). You subtract your age from 100 to find your stock percentage.

Example: Meet Sarah (Age 30)

- The Calculation: 100 - 30 = 70%.

- The Allocation: Sarah puts 70% of her money into a Total Stock Market ETF and 30% into a Bond Fund.

- The Result: Because she is young, she has time to weather the ups and downs of that 70% stock portion. If the market crashes 20% tomorrow, her 30% bond cushion helps keep her total account from falling as far.

3. Common 2026 Portfolio Models

Depending on your "sleep-at-night" factor (risk tolerance), you might choose one of these pre-set models:

| Portfolio Style | Asset Mix (Stocks / Bonds / Alts) | Who is it for? |

|---|---|---|

| Aggressive | 80% / 10% / 10% | People in their 20s or 30s with 20+ years to invest. |

| Moderate | 60% / 30% / 10% | The "Classic 60/40" for mid-career professionals. |

| Conservative | 30% / 60% / 10% | Retirees or those needing their money in 3–5 years. |

Note: In 2026, many investors add a 5–10% "Alternative" slice for assets like Gold or REITs to further diversify.

4. Why You Must "Rebalance"

Asset allocation is not a "set it and forget it" task. Over time, your winners will grow and take over your portfolio.

The Scenario: You start with a 50/50 mix of Stocks and Bonds. After a massive year for AI stocks in 2025, your stocks have grown so much that they now make up 70% of your account.

The Problem: You are now much riskier than you intended to be. If a crash happens, you will lose more money than you planned.

The Fix: You sell a portion of your stocks (selling high) and buy more bonds (buying low) to get back to your 50/50 target. This disciplined "Rebalancing" is the secret to long-term success.