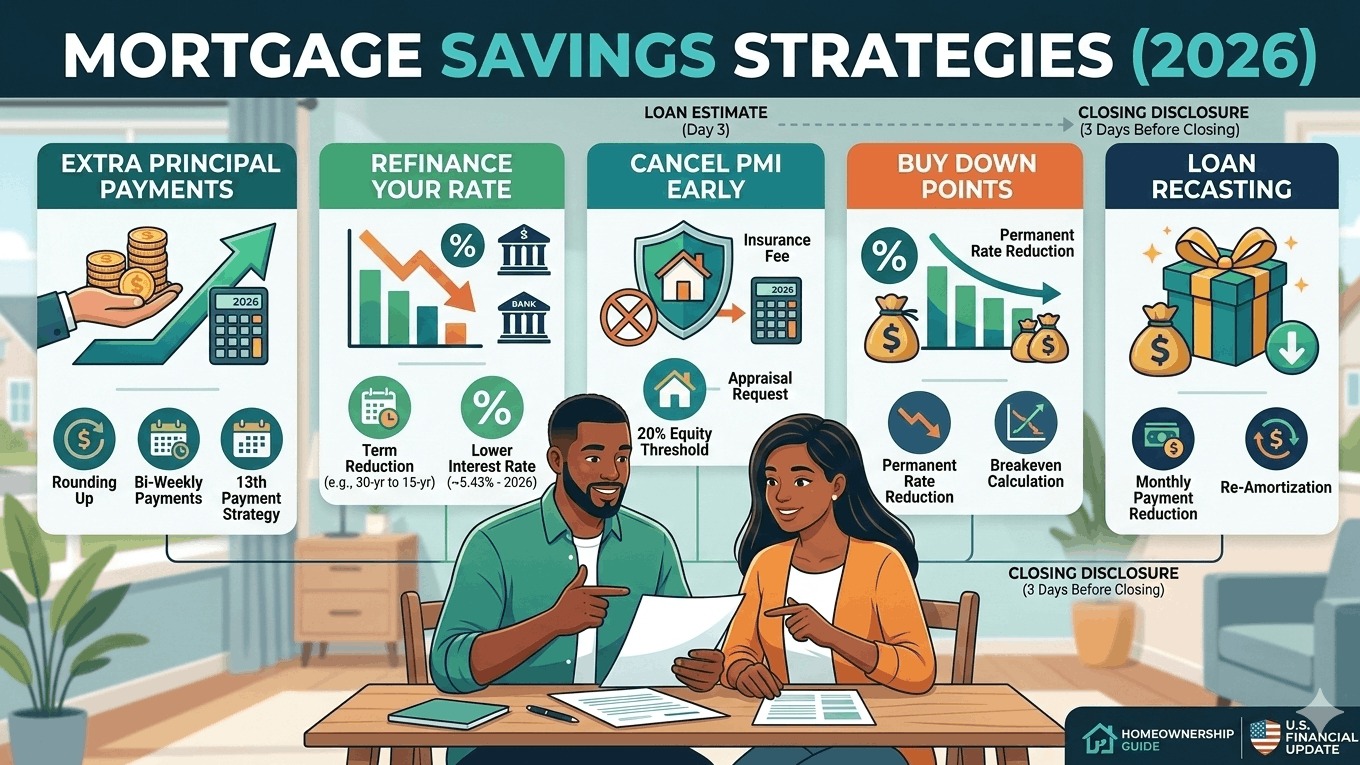

In 2026, the mortgage landscape has shifted. With 30-year fixed rates stabilizing around 6.00% and 15-year rates near 5.43%, homeowners are moving away from "survival mode" and back into strategic wealth-building. Whether you are about to sign a new loan or have been paying one for years, saving money on your mortgage is about reducing the total interest you pay over the life of the loan.

Here are the most effective, battle-tested strategies to save thousands on your mortgage this year.

1. The "Extra Payment" Mastery

The simplest way to save money doesn't require a bank's permission: pay more than the minimum. Because interest is calculated on your remaining principal, every extra dollar you pay today reduces the interest you are charged every month for the next 20+ years.

- The 13th Payment Strategy: By making one extra full mortgage payment each year, you can shave roughly 5 to 7 years off a 30-year mortgage.

- Bi-Weekly Payments: Switch from monthly payments to half-payments every two weeks. Because there are 52 weeks in a year, you’ll end up making 26 half-payments—equivalent to 13 full payments a year—without ever feeling the "extra" hit to your budget.

- Rounding Up: If your payment is $1,920, pay $2,000. That extra $80 a month is a "silent" principal killer.

2. Strategic Refinancing in 2026

Early 2026 has seen a slight dip in rates compared to the 2024–2025 peaks. If your current rate is 7.0% or higher, a refinance could save you significant cash.

- The 1% Rule: Traditionally, if you can drop your rate by 1%, a refinance is a "must-consider." In 2026, even a 0.75% drop can be worth it if you plan to stay in the home for more than five years.

- Term Reduction: Refinancing from a 30-year to a 15-year mortgage will increase your monthly payment, but it can save you $250,000+ in total interest.

- No-Cost Refi: Ask about "lender-paid closing costs." You’ll accept a slightly higher interest rate in exchange for the lender covering the thousands in fees upfront.

3. Eliminating "Dead Money" (PMI and Fees)

"Dead money" refers to costs that provide you with no equity or benefit.

- Cancel PMI Early: If you put down less than 20%, you are likely paying Private Mortgage Insurance (PMI). In 2026, home values in many states have risen. If your equity has reached 20%, call your lender to request an appraisal and cancel your PMI. This can save you $100–$300 per month instantly.

- Tax Assessment Appeals: If home prices in your specific neighborhood have dipped, your property tax assessment might be too high. Challenging your assessment at the local county office can lower your "T" in your PITI payment.

4. Buying "Points" Upfront

If you are buying a home or refinancing in 2026 and plan to stay for 10+ years, consider buying down the rate.

- How it works: You pay an upfront fee (1 "point" equals 1% of the loan amount) to permanently lower your interest rate by roughly 0.25%.

- The Math: If a point costs you $4,000 but saves you $60 a month, your "break-even" point is 66 months. If you stay in the home longer than that, every month after is pure profit.

5. Loan Recasting: The Hidden Alternative

If you come into a windfall (a bonus, inheritance, or tax refund), don't just pay it toward the principal—ask for a recast.

- The Difference: Unlike a refinance, a recast doesn't change your interest rate. Instead, the lender takes your new, lower principal balance and "re-amortizes" it over your remaining years.

- The Benefit: Your monthly payment drops significantly, providing better cash flow without the high fees of a refinance.