Before you start touring open houses, you need to know exactly how much "house" you can afford. While online calculators are convenient, understanding the manual math behind your mortgage payment is the only way to truly master your budget.

In 2026, with 30-year fixed rates averaging around 6.00%, even a small change in your interest rate or down payment can shift your monthly obligation by hundreds of dollars. This guide breaks down the "PITI" formula and shows you how to calculate your payment like a pro.

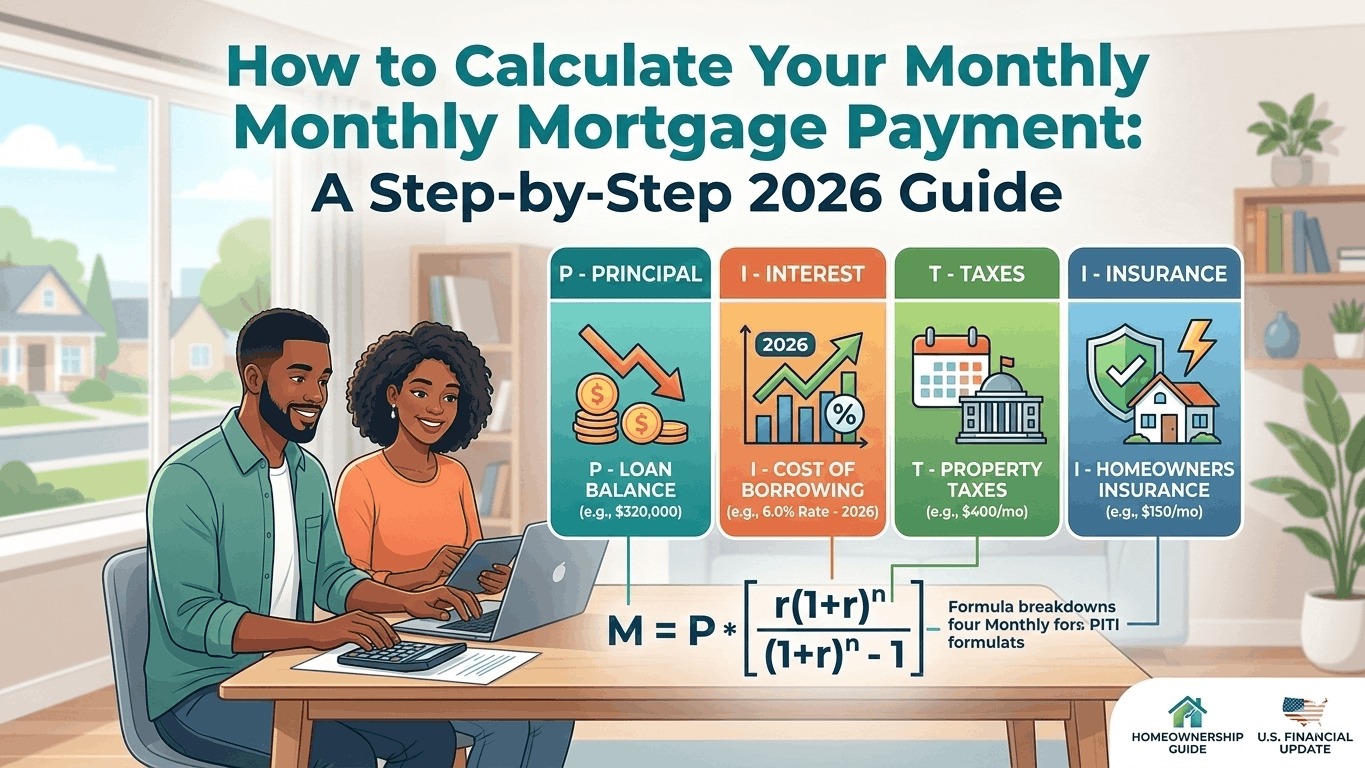

1. The PITI Formula: The Four Pillars of Your Payment

Most beginners think a mortgage payment is just the loan and interest. In reality, your monthly check to the bank usually covers four distinct costs, known as PITI:

- Principal: The amount that goes toward paying off the original balance of your loan.

- Interest: The fee the lender charges for the privilege of borrowing the money.

- Taxes: Your local property taxes, usually divided into 12 monthly installments.

- Insurance: This includes homeowners insurance and, if applicable, Private Mortgage Insurance (PMI).

2. Calculating Principal and Interest (The Math)

The "PI" part of the equation is the most complex. To calculate this manually, lenders use the standard amortization formula:

M = P r(1+r)n / (1+r)n - 1

Where:

- M: Your total monthly principal and interest payment.

- P: The principal loan amount (the home price minus your down payment).

- r: Your monthly interest rate (your annual rate divided by 12 months).

- n: The total number of months in your loan term (e.g., 360 months for a 30-year loan).

2026 Example Calculation:

If you buy a $400,000 home with a 20% down payment ($80,000), your loan amount (P) is $320,000.

At a 6.0% annual interest rate, your monthly interest (r) is 0.005.

Over 30 years, your total months (n) is 360.

Using the formula, your monthly Principal and Interest payment would be: $1,918.56.

3. Estimating Taxes and Insurance

To get your final PITI total, you must add the "T" and "I."

- Property Taxes: Look up the local tax rate (e.g., 1.2% of the home's value). For a $400,000 home, that’s $4,800/year, or $400/month.

- Homeowners Insurance: The national average in 2026 is roughly $150/month, though this is higher in coastal or high-risk states.

- PMI (If applicable): If you put down less than 20%, add roughly 0.5% to 1.5% of the loan amount annually. On a $320,000 loan, this adds about $133–$400/month.

Total 2026 Monthly Payment (PITI): $1,918.56 + $400 + $150 = $2,468.56

4. Factors That Will Change Your Result

- The Down Payment: Every extra $10,000 you put down reduces your monthly payment by roughly $60 (at 6% interest).

- The Loan Term: A 15-year mortgage will have a significantly higher monthly payment because you are paying off the principal twice as fast, even though the interest rate is lower.

- Escrow Account Changes: Lenders often manage your taxes and insurance through an Escrow Account. If your local tax rate goes up, your monthly mortgage payment will increase, even if you have a fixed-rate loan.