Becoming mortgage-free is the ultimate financial milestone. In 2026, with interest rates for existing loans ranging from pandemic-era lows of 3% to recent peaks near 7%, the strategy for paying off your home early depends on your specific "math."

Whether you want to shave off five years or fifteen, here is the blueprint for accelerating your path to full homeownership.

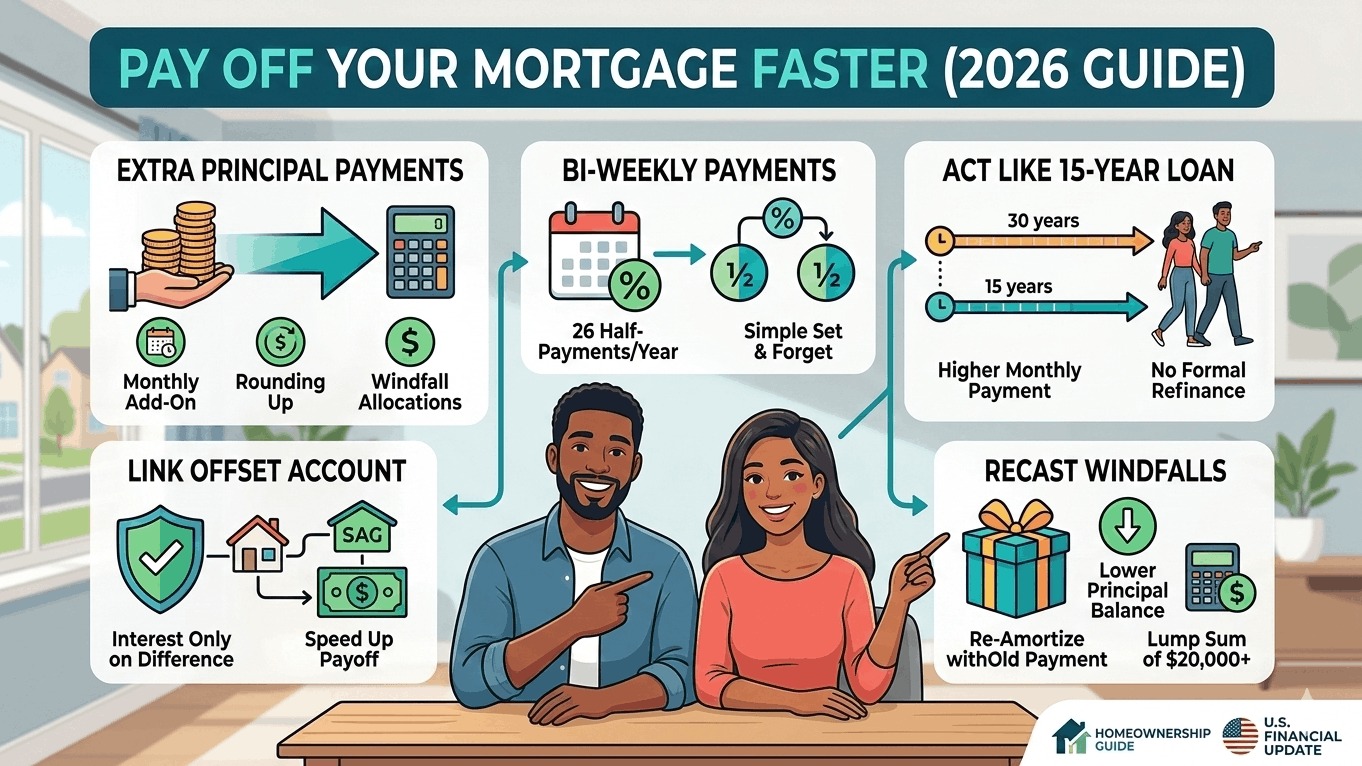

1. The "Extra Principal" Multiplier

The most effective way to shorten your loan is to ensure every extra dollar goes directly to the principal balance, not toward future interest.

- The Monthly Add-On: Adding just $100 extra to your monthly payment on a $300,000 loan at 6% can shave over 4 years off your mortgage and save you roughly $50,000 in interest.

- The 1/12th Rule: If a full extra payment feels daunting, divide your monthly principal and interest payment by 12. Add that amount to each monthly check. By the end of the year, you’ll have made a full 13th payment without a "lump sum" shock to your budget.

- Windfall Allocations: Commit to putting 50% of "surprise money"—tax refunds, work bonuses, or cash gifts—directly toward the mortgage principal.

2. Switch to Bi-Weekly Payments

This is a "set it and forget it" strategy that aligns with most 2026 payroll cycles.

- The Mechanism: Instead of one monthly payment, you pay half of your mortgage every two weeks.

- The Result: Because there are 52 weeks in a year, you make 26 half-payments. This equals 13 full payments a year.

- The Impact: On a 30-year loan, this simple switch typically shaves 4 to 6 years off the term, depending on your interest rate.

- Note: Always verify with your lender that they apply bi-weekly payments immediately to the principal.

3. The "Pseudo-Refinance" Strategy

If you have a 30-year mortgage but your income has grown, you can "act" like you have a 15-year mortgage without the high fees of a formal refinance.

Calculate what a 15-year payment would be for your current balance (using a 2026 mortgage calculator) and pay that amount instead.

- The Flexibility Benefit: Unlike a formal 15-year loan, if you have a tight month or an emergency, you can legally drop back down to your required 30-year minimum payment without penalty.

4. Leverage "Offset" Accounts (If Available)

Popular in international markets and gaining traction in some U.S. "all-in-one" loan products for 2026, an Offset Account links your savings to your mortgage.

- How it Works: If you owe $400,000 but have $50,000 in a linked offset savings account, the bank only charges you interest on $350,000.

- The Speed: Your monthly payment stays the same, but because you're being charged less interest, a much larger portion of your payment automatically goes toward the principal, accelerating your payoff date.

5. Recast After Large Lump Sums

If you receive a significant windfall (e.g., $20,000+), don't just pay it toward the principal—request a recast.

- For a small fee (usually ~$250), the lender will keep your current interest rate but "re-calculate" your monthly payments based on the new, lower balance.

- The Pro Move: Keep making your old (higher) payment amount even after the recast. Since your new required minimum is lower, almost the entire difference will go toward the principal, causing your balance to plummet.