When people talk about wealth, income usually gets all the attention. But income only tells part of the story. Net worth—the total value of what you own minus what you owe—is a much better measure of financial health.

Looking at median net worth by age in the United States gives you a realistic benchmark of where people stand financially at different stages of life. More importantly, it helps you understand what’s typical, what’s possible, and how your own financial journey compares.

What Is Net Worth?

Net worth is a simple but powerful concept. It represents the difference between your assets and liabilities.

- Assets include things like cash, investments, property, and retirement accounts

- Liabilities include debts such as loans, credit cards, and mortgages

If your assets are greater than your debts, you have a positive net worth. If not, your net worth is negative.

This number reflects your true financial position far better than income alone.

To calculate your own position:

Net Worth Calculator – https://statush.com/net-worth-calculator

Why Median Net Worth Matters

When analyzing wealth, median net worth is more useful than average net worth.

| Measure | Explanation | Why It Matters |

|---|---|---|

| Average Net Worth | Total wealth divided by number of households | Skewed by extremely wealthy individuals |

| Median Net Worth | The middle value in the dataset | Represents the typical household |

The median shows what a “normal” household looks like financially, making it a better benchmark for comparison.

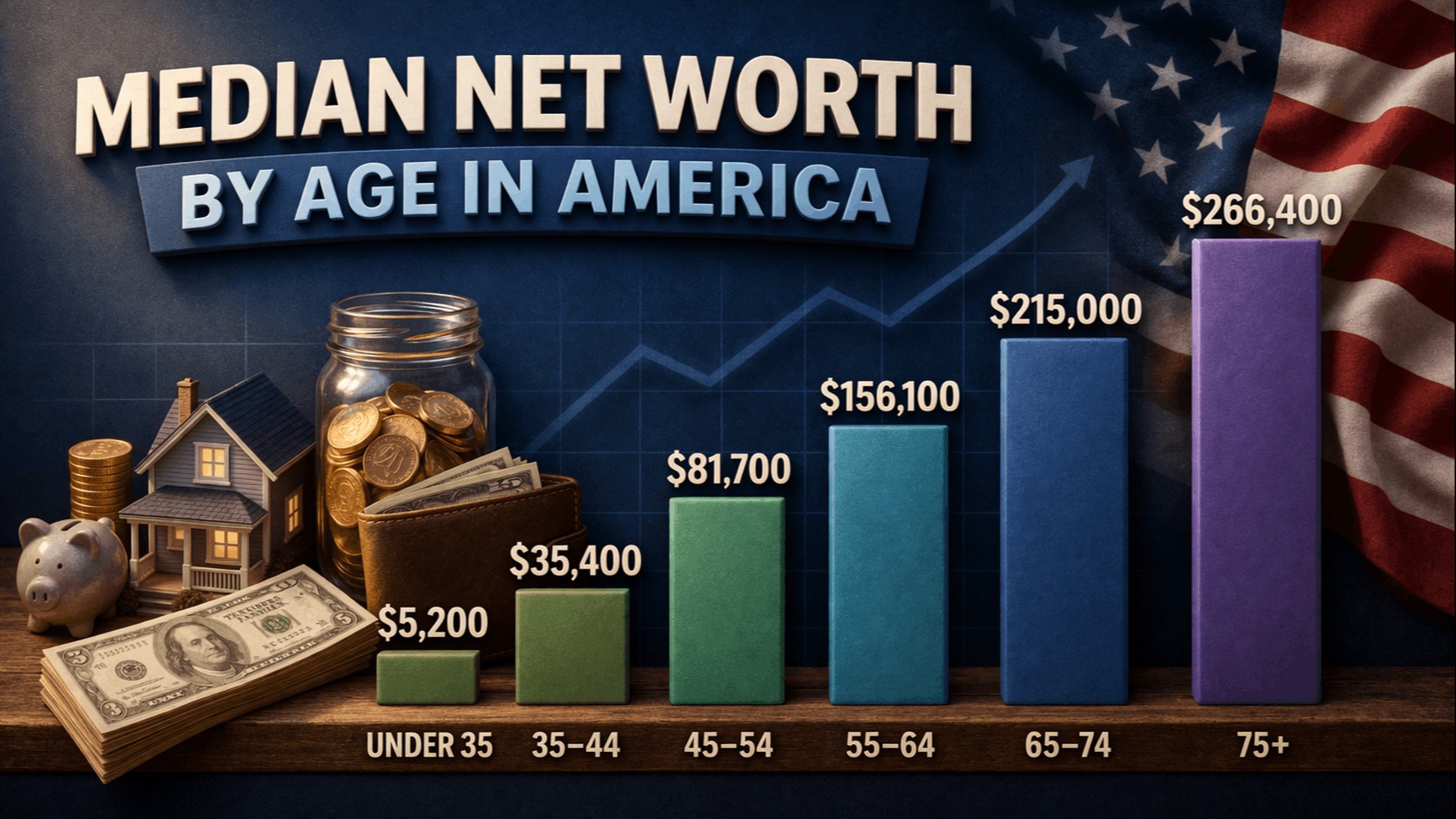

Median Net Worth by Age Group

Net worth tends to follow a predictable pattern as people move through different life stages.

| Age Group | Median Net Worth Trend | Explanation |

|---|---|---|

| Under 35 | Lower or near zero | Early career, student loans, limited assets |

| 35–44 | Growing steadily | Increasing income, homeownership begins |

| 45–54 | Strong growth | Peak earning years, higher investments |

| 55–64 | Highest accumulation phase | Retirement savings peak |

| 65+ | Stabilizes or declines slightly | Withdrawals begin during retirement |

Understanding Each Life Stage

Under 35: Building the Foundation

In the early years, net worth is often low or even negative. This is usually due to student loans, car loans, or limited savings.

At this stage, the focus is less on wealth accumulation and more on:

- Building income

- Reducing debt

- Starting to save

Real Example

A 28-year-old might have:

- $10,000 in savings

- $20,000 in student loans

Net worth: –$10,000

This is common and not necessarily a problem—it’s part of the early financial journey.

35–44: Growth Begins

As careers progress, income increases and debt starts to decrease. Many people buy homes and begin investing more seriously.

This stage often marks the transition from negative or low net worth to meaningful growth.

45–54: Acceleration Phase

This is where wealth building accelerates.

Higher income, combined with years of investing, leads to significant increases in net worth. Retirement accounts and home equity play a major role here.

55–64: Peak Wealth Years

By this stage, most people have reached their highest net worth.

They typically have:

- Substantial retirement savings

- Reduced debt

- Valuable assets

This is also the period where financial planning becomes more focused on preservation rather than growth.

65+: Wealth Utilization

In retirement, net worth may stabilize or decline slightly as people begin using their savings.

The focus shifts to:

- Managing withdrawals

- Minimizing taxes

- Maintaining financial stability

To understand this phase better:

Tax Planning for Retirement – https://statush.com/finance-statistics/tax-planning-for-retirement

Real-World Comparison

Let’s compare two individuals at age 40:

Person A

- Income: $120,000

- Savings: Minimal

- Debt: High

Person B

- Income: $80,000

- Savings: Consistent

- Debt: Managed

Even though Person A earns more, Person B may have a higher net worth due to better financial habits.

This highlights an important truth: net worth is built through consistency, not just income.

Factors That Influence Net Worth

Several key factors shape how net worth grows over time.

Income Growth

Higher income provides more opportunity to save and invest, but it must be managed effectively.

Saving and Investing Habits

Regular investing, even in small amounts, can lead to significant growth over time.

Debt Management

High-interest debt can slow down wealth building, especially in early years.

Taxes

Taxes reduce both income and investment returns, impacting long-term wealth.

To understand this impact:

How Taxes Impact Wealth Building – https://statush.com/finance-statistics/how-taxes-impact-wealth-building

How Net Worth Builds Over Time

Net worth growth is not linear—it accelerates over time due to compounding.

| Stage | Key Focus | Long-Term Effect |

|---|---|---|

| Early Years | Saving and reducing debt | Foundation building |

| Mid Career | Investing consistently | Rapid growth |

| Late Career | Maximizing assets | Peak wealth |

| Retirement | Managing withdrawals | Wealth preservation |

This progression shows why starting early is so important.

Common Mistakes That Slow Net Worth Growth

Many people delay wealth building due to avoidable mistakes.

These often include:

- Waiting too long to start investing

- Carrying high-interest debt

- Increasing lifestyle expenses too quickly

- Ignoring long-term planning

Even small changes can have a big impact over time.

Tools to Track Your Progress

Tracking your net worth regularly helps you stay on course.

- Net Worth Calculator – https://statush.com/net-worth-calculator

- Savings Goal Calculator – https://statush.com/savings-goal-calculator

- Retirement Calculator – https://statush.com/retirement-calculator

These tools help you turn financial awareness into action.

A Practical Perspective

Instead of comparing yourself strictly to averages, it’s more useful to focus on your trajectory.

Ask yourself:

- Is my net worth increasing each year?

- Am I reducing debt and building assets?

- Am I planning for long-term financial stability?

Progress matters more than comparison.

Final Thoughts

Median net worth by age in America provides a helpful benchmark, but it’s not a strict rulebook. Everyone’s financial journey is different, shaped by choices, opportunities, and timing.

The key takeaway is simple:

- Net worth is a better measure than income

- Growth takes time and consistency

- Smart financial habits matter more than starting point

When you focus on building assets, managing debt, and staying consistent, your net worth will grow—regardless of where you start.